This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

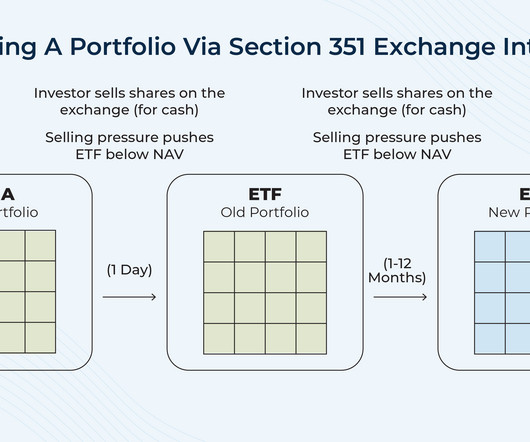

Following the long run-up in the US equity markets since the bottom of the 2008–2009 financial crisis, many investors with taxable investment accounts have likely found themselves with high embedded gains in their portfolios. If the exchange meets the requirements of Section 351, it is tax-deferred for investors.

tonyisola.com) Age is just one factor when it comes to your assetallocation. mrmoneymustache.com) Why you need to account for your Treasury income on your state taxes. fastcompany.com) What to consider when rolling over a 401(k) account to an IRA. readthejointaccount.com) When a second home makes financial sense.

standarddeviationspod.com) Christine Benz and Amy Arnott talk assetallocation and more with Matt Krantz. riabiz.com) Retirement accounts On the downside of holding non-traditional assets in an IRA. investmentnews.com) Why funds in pre-tax retirement accounts need to be adjusted for taxes.

This includes a broad AssetAllocation including full Diversification of asset classes, geographies, etc. via the site (and Etsy shop and Instagram account) Mindfulenough. Asset Economy. AssetAllocation. You must Save enough money relative to your income by living within your means. Inflation.

peterlazaroff.com) Investing There's no magic rule for assetallocation. crr.bc.edu) Saving for college How much should you save in 529 accounts? theconversation.com) Taxes Earned income? flowfp.com) Billionaires pay their taxes differently. awealthofcommonsense.com) Four ways to reduce sequence-of-returns risk.

Tax-loss harvesting is a powerful strategy that investors can use to reduce their taxable income. As effective as tax-loss harvesting can be, there are a number of important details that investors need to be aware of in order to implement the strategy successfully while following regulations. How does tax-loss harvesting work?

Reevaluate Your AssetAllocation If watching your investment portfolio fluctuate causes anxiety, your current allocation might be too aggressive. You can reduce your stock exposure and increase investments in fixed income options, such as cash or bonds, within tax-advantaged accounts (like a 401(k), IRA, or Roth IRA).

So historically, every $1 million invested would yield annual dividend income of $19,800 on average… before tax. If you own 10,000 shares, you receive $40,000 in dividend income (before taxes) and have a portfolio currently worth $2M. Over the last 30 years, the S&P 500’s average dividend yield was 1.98%.

As the year comes to a close, now is the time to review potential financial moves to help minimize your tax burden heading into 2025. Proactive year-end tax planning can lead to significant savings and set you up for financial success in the new year. Find your next tax advisor at Harness today. Starting at $2,500.

Most individuals choose to have a certain amount of money transferred from each paycheck directly into their investment accounts so they don’t even have the option to spend it. Set Up Another Retirement Account Individual Retirement Accounts (IRAs) may offer tax advantaged savings as well.

However, what is equally critical when it comes to creating a portfolio is assetallocation and selection. Assetallocation aims to balance risk and reward through a portfolio composition of different kinds of assets. If not allocated efficiently, you may become subject to a slew of taxes and other charges.

What to Do Instead: Stick to fundamentals: Learn about assetallocation, risk management, and diversification before investing. Keep it separate: Use a high-interest savings account or liquid mutual fundsbut not your main spending account. Use it only for real emergencies: If you have to ask, Is this an emergency? ,

One of the pre-market Bloomberg emails gave a positive mention to the Cambria Global AssetAllocation ETF (GAA) because it is up in what of course has been a tough tape for equities this year. It is an interesting assetallocation that targets 40% in equities, 40% in fixed income and 20% in alternatives.

As the tax year draws to a close, many high-income investors will look to reposition their portfolios to intentionally generate losses as a way to offset gains — an investment strategy known as tax loss harvesting. A net neutral tax position. What Is Tax Loss Harvesting? How Tax Loss Harvesting Works.

🔊 Play Audio Have you heard of the Income Tax Saving Festival in India? Well, usually it starts in the last quarter of the financial year (Jan-Mar) when many employees scurry to provide investment proof to save tax outgo. If not already, why not from today?

Review risk tolerance and current assetallocation strategy It’s important to ensure your clients’ portfolios align with their risk tolerance because taking too much risk can negatively impact their ability to navigate market fluctuations. You can help them start the year right by conducting a retirement checkup.

A financial advisor can help navigate the complexities of wealth management, from tax considerations to estate planning and retirement strategies. Their role extends beyond investment managementthey can help with: Retirement Planning : Structuring your assets to support your desired lifestyle. Ready to Grow Your Wealth?

The age when retirees must begin drawing from non-Roth retirement accounts increases to 73 in 2023, then 75 in 2033. Those born between 1951 – 1959 can delay taking money from retirement accounts in their own name until 73. Here are some tax planning strategies to consider when you should start drawing from your IRA.

CIO Perspectives Webinar, 2022 AssetAllocation Outlook mhannan Fri, 03/18/2022 - 06:42 Markets have been unsteady at the start of 2022, driven by geopolitical tensions, inflation, and concerns about equity valuations. Brown Advisory does not render legal or tax advice. The war in Ukraine is causing even more uncertainty.

CIO Perspectives Webinar, 2022 AssetAllocation Outlook. CIO Perspectives Webinar, 2022 AssetAllocation Outlook . The themes and topics discussed include: The performance of various markets and asset classes over recent years and since the onset of the Ukraine conflict. Fri, 03/18/2022 - 06:42. Watch the Video.

Your assetallocation is the percentage of your portfolio that you distribute between different asset classes, like stocks and bonds. To rebalance your portfolio, you’ll buy and sell certain investments to realign to your accounts with your desired assetallocation.

Early on in my savings journey I prioritized tax-deferred retirement accounts over all else. I like the ease and simplicity of 401k contributions coming out of my paycheck before it ever even touches my checking account. It’s easy to automate.

Depending on your financial situation and the type of asset you inherit, your options may differ. Inherited cash, stocks, or a brokerage account. Inheriting money or taxable investment accounts has some big benefits. Further, many beneficiaries are eligible for a step-up in basis on eligible assets. Inheriting a home.

A Contributory IRA, otherwise known as a traditional IRA , is a retirement savings account that allows individuals to make contributions from their earned income. Contributory IRA accounts are held by custodians, such as banks, brokerage firms, and mutual fund companies.

Consider early retirement tax planning. Retirement accounts like 401(k)s and IRAs provide the advantage of tax-deferred growth, saving you significant amounts of money in taxes over the long term. Research different retirement accounts and investments to determine which is best for your individual needs.

You just needed a brokerage account. But today, you know, a lot of brokers, you know, whether they’re with the big full service brokerage firms now have advisory accounts that they flog to clients where they can buy ETFs. 00:10:57 [Speaker Changed] So let me push back a little bit on that.

Investment strategy: Determine assetallocation and investment vehicles aligned with risk tolerance and financial goals. Retirement planning: Calculate retirement needs and contribute regularly to retirement accounts. This blog is not intended to provide specific legal, tax, or other professional advice.

And my dad had always said, as many young kids get this advice, doctor, lawyer, accountant, engineer. SALISBURY: And accountant seemed like a reasonable option. And I kind of stumbled my way into accounting. That background of being an accountant was just great bedrock training. RITHOLTZ: Sure. Very different fields.

I created this list of financial advisors for small accounts (less than $300,000 in assets) because there are alot of schmucks out there hawking crap products to people with portfolio of this size, and I don’t think it’s fair. Transform Retirement www.transformretirement.com Avg account size: Approx.

Of course, one of the most important aspects of retirement planning is managing retirement taxes. Taxes can significantly impact the amount of money you’ll have for retirement. As such, you must be aware of any tax implications arising from your investments during your working years.

Of course, one of the most important aspects of retirement planning is managing retirement taxes. Taxes can significantly impact the amount of money you’ll have for retirement. As such, you must be aware of any tax implications arising from your investments during your working years.

Many people invest in their company-sponsored 401(k)s but only sometimes take the time to review the investments within the account. Rebalancing involves adjusting the mix of assets in your 401(k) portfolio to maintain a desired level of risk and return. We make it easy by matching you to vetted advisors that meet your unique needs.

Calculate your 2023 after tax income and expected after tax 2024 income. Look at those discretionary expenses that might not be necessary (cable TV, that Hulu account you never watch, the Pandora music you don’t listen to, etc). AssetAllocation and Goals. We are big advocates of time based assetallocation.

Minimize Risk Implement an investment strategy that takes market risk, inflation risk and time horizon into account. As you get closer to retirement your assetallocation should change. Additionally, be sure to account for the tax confusions of different investments in taxable brokerage accounts and retirement accounts.

A lot of this depends on which market you look at and what time horizon, but the global stock market has generated nowhere near 10% when you account for real factors like inflation, taxes and fees. We live in the real world where we pay for inflation, taxes and fees over time. 3) This is Not an Era of Fiscal Dominance.

which accounts for about half of it's total outperformance since inception. Circling back to model ETF portfolio mentioned at the top of this post, the assetallocation was as follows. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation.

One thing that I have craved for investors is a tool that allows you to sync all your financial accounts – your investment portfolio, checking and savings accounts, credit cards and other loan accounts – in one place, and then provides an investment-related analysis of your entire portfolio.

Beef up your emergency fund – A good rule of thumb is to have between 3-6 months’ worth of expenses set aside in a high-yield savings account. The catch-up contribution (available for anyone over age 50) remains the same at $7500 for elective deferral account and $1k/year for Traditional and Roth IRAs.

Most investors pay close attention to their assetallocation. And that makes sense since research has shown that the asset classes a portfolio is allocated to drive the majority of its return over time. But assetallocation isn’t the whole story.

Overindulgence in information can lead to poor decisions, and excessive monitoring of your retirement account balance can result in stress. Checking your retirement account balance too often can have a psychological impact on you. Therefore, exploring the optimal frequency for checking your retirement account is essential.

Several talked about tax issues, it is important to keep tabs on how taxes might change going forward and then when they actually do change. Yes on the taxes but without earned income and living on long term capital gains from an investment portfolio, there might be no income tax. Always read the comments.

For the last couple of years, I think a lot of people gravitated to just using market cap weighted in their accounts, that seems like it has been the conversation and for 2023 and 2024 the returns for MCW have been great. MCW also did great in 2021, 2020 and 2019. Occasionally of course, MCW gets pasted.

Make funding tax-advantaged accounts a priority Tax-advantaged accounts are specifically designed to help savers build their retirement nest egg. Some common tax-advantaged retirement savings solutions include your 401(k), 403(b), and SIMPLE 401(k) plan. Once in the account, your contributions will grow tax-free.

Tax Loss Harvesting: Upside To A Down Market ajackson Thu, 03/26/2020 - 14:08 The market's path forward is extremely uncertain right now, but there are still planning steps that investors can implement today to generate positive results down the line. TAX LOSS HARVESTING: WHAT IS IT? Assets should not be sold solely for tax reasons.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content