This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

We start with several articles on retirement planning: Why considering a client's retirement time horizon and spending flexibility could lead to more accurate (and often higher) safe withdrawal rates than the simpler "4% rule" Four unique risks retirees face when drawing down their assets, from sequence of returns risk to tax risk, and how financial (..)

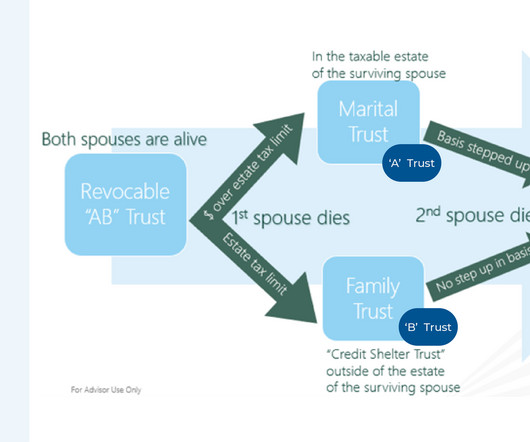

In recent years, the Internal Revenue Code (IRC) has endured some drastic changes resulting from legislative action that have altered the strategies estateplanning professionals have recommended to clients. For instance, prior to the 2017 Tax Cuts and Jobs Act (TCJA), "A/B trusts" had become ubiquitous for spousal estatetaxplanning.

Proactive year-end taxplanning can lead to significant savings and set you up for financial success in the new year. Checklist: Year-end TaxPlanning Strategies Review the following tax strategies with your tax advisor and/or financial advisor before the end of the year.

As a Christian, your estateplan should represent your dedication to financial stewardship according to Scripture. W hat important factors should Christians consider when estateplanning? W hat important factors should Christians consider when estateplanning?

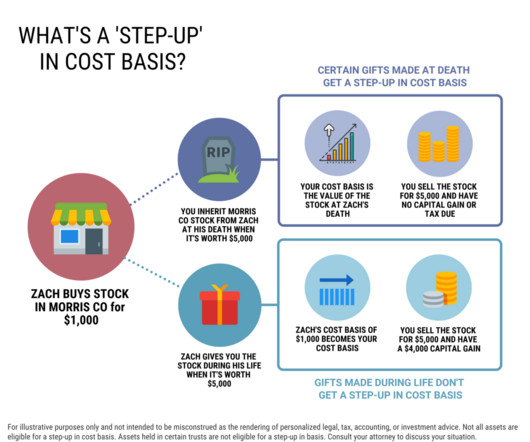

This means that if the beneficiary taxpayer sells the stock for $650, they’d only pay long-term capital gains tax on a $150 gain, rather than $550. Conversely, if the original account owner gifted the stock while living, the recipient retains purchaser’s carryover basis and holding period ($100 in this example). Yes and no.

Also in industry news this week: With a potential SEC regulation requiring RIAs to engage in enhanced "know your customer" practices under consideration, the Investment Adviser Association is arguing for a more tailored approach to identifying risky clients and a longer implementation period to relieve the potential burden on RIAs The SEC is investigating (..)

Under the new law, non-spouse beneficiaries (with few exceptions) must now withdraw the entirety of an inherited IRA within 10 years of the account owner's passing rather than over their own lifetimes. This shift has led financial advisors to explore new strategies for mitigating the resulting tax-planning challenges.

Which means that by taking into account a client's net worth, realistic liability risks, and level of sophistication, advisors can help assess what types of strategies may be appropriate for the client to explore. For instance, qualified plan assets (e.g., tenancy by the entireties and community property).

Welcome to the October 2024 issue of the Latest News in Financial #AdvisorTech – where we look at the big news, announcements, and underlying trends and developments that are emerging in the world of technology solutions for financial advisors!

million in assets to both retire and pass on a legacy interest (though many have yet to establish an estateplan), according to a recent survey. Enjoy the current installment of "Weekend Reading For Financial Planners" – this week's edition kicks off with the news that affluent Americans believe they need an average of $5.5

Also in industry news this week: Backers announced the new Texas Stock Exchange, which seeks to provide companies with a lower-cost alternative to the NYSE and Nasdaq, which, if successful, could create a more competitive landscape and potentially better execution and reduced trading costs for financial advisors and their clients The American College (..)

Holistic Financial Management Beyond investment advice, financial advisors offer comprehensive services such as taxplanning, estateplanning, and risk management. This support can be important in maintaining discipline and making rational decisions amidst market fluctuations.

In this guest post, Harness Tax Advisory Council member, Griffin Bridgers, J.D., covers some of the top estateplanning trends that tax advisors should be tracking during the second half of 2024. contained a number of changes relevant to estateplanning. citizens and residents. The SECURE Act 2.0

They could also consider contributions to an individual retirement account (IRA) and a health savings account (HSA) , too. Make sure they take their required minimum distributions Clients who are age 73 or over must take required minimum distributions (RMDs) from their qualified plans and IRAs.

Common types of assets that will pass via beneficiary designation include retirement accounts, life insurance, and some pensions and annuities. The most common examples of joint assets are real estate, bank and brokerage accounts. The US has 50 states – each with their own tax laws and estateplanning opportunities.

Not only was the stock market fairly volatile, but there were also atypical tax regulation changes. The combination of those means that there is going to be a lot of complexity to account for as you look back on the year. Tax-loss harvesting. The current lifetime gift tax exclusion is $12.06M (or $24.12 Estateplanning.

Investment planning also plays a crucial role in tax optimization, enabling you to minimize tax liabilities and maximize after-tax returns. In addition to traditional health insurance, you can also explore the Health Savings Account (HSA). Asset diversification is an essential component of effective taxplanning.

While there are certainly ways to do estateplanning without a lawyer, for most people hiring an estateplanning attorney makes the most sense. Estateplans can get complex fast, and even fairly straightforward estates can feel overwhelming if you’re not trained in the area. Do your research.

Choosing whether to fund a trust with your assets is an important decision in the estateplanning process. A will and a trust are two different estateplanning tools. This can include a bank account, brokerage account, home, car, art, and even equity in a privately held business.

Creating wealth that can provide financial security for generations to come is an incredible feat, and it requires careful planning, consideration, and communication among family members. Let’s take a look at the tax impact and other considerations of each. . 200/share (today’s fair market value) – $188.44/share

A financial advisor can help with maximizing your retirement income through taxplanning After retirement, your income sources may become limited to pensions, Social Security benefits, and investment income. A financial advisor can craft tax-efficient withdrawal strategies to minimize the tax burden on your retirement income.

Here are some examples of one-time and ongoing services you can offer clients under the fee-for-service model: One-Time Services Ongoing Services Comprehensive Financial Plan Ongoing Financial Planning Second Opinion Engagement Advising on Held-Away Accounts Student Loan Analysis TaxPlanning Portfolio Tax Efficiency Review EstatePlanning Housing (..)

Navigating the complexities of estateplanning can often feel like charting through uncharted waters, especially when it comes to handling assets, taxes, and ensuring one’s legacy is preserved according to their wishes.

The post Part 1: The Tools of the Tax-Planning Trade appeared first on Yardley Wealth Management, LLC. Part 1: The Tools of the Tax-Planning Trade Whether you’re saving, investing, spending, bequeathing, or receiving wealth, there’s scarcely a move you can make without considering how taxes might influence the outcome.

The post Part 1: The Tools of the Tax-Planning Trade appeared first on Yardley Wealth Management, LLC. Part 1: The Tools of the Tax-Planning Trade. Whether you’re saving, investing, spending, bequeathing, or receiving wealth, there’s scarcely a move you can make without considering how taxes might influence the outcome.

This tax benefit is scheduled to sunset at the end of 2026. Taxplanning for 2026 Depending on your situation, income, and goals, your planning options will vary. As with anything in taxplanning, it’s important not to let the tax-tail wag the dog.

Key Takeaways: Accounting advisory services extend beyond traditional tax preparation to offer strategic financial guidance. Specialized areas can include estateplanning and tax-efficient investment strategies. Table of Contents What Are Accounting Advisory Services?

Depending on a firms tech strategy, she wrote, advisors may have to log in to the CRM, custodian, portfolio accounting, planning software, taxplanning software, estateplanning software, social security maximizer software, etc.,

When you are presented with the option to distribute your assets, you will have the choice to roll them into an IRA or place the stock into a taxable account and then roll the remaining assets into an IRA or 401(k). In addition, shares of employer securities for the NUA must be moved in-kind to a taxable brokerage account.

Part 3: Tax-Wise Financial Planning In our last two pieces, we covered some tools of the tax-planning trade, as well as how to deploy them for tax-efficient investing. But taxplanning isn’t just for your investments. But we can weave each event into the tax-planning fabric of your financial life.

Part 3: Tax-Wise Financial Planning. In our last two pieces, we covered some tools of the tax-planning trade, as well as how to deploy them for tax-efficient investing. . But taxplanning isn’t just for your investments. Each can translate into tax-planning challenges and opportunities: .

Retirement planning: Calculate retirement needs and contribute regularly to retirement accounts. TaxPlanning: Optimize tax efficiency through strategies such as retirement contributions, tax-deferred accounts, and deductions and credits.

Part 2: Tax-Wise Investment Techniques In our last piece, we introduced some of the tools of the tax-planning trade. In other words, your tax-planning techniques matter at least as much as the tools. Tax breaks come and go, and are beyond our control. It’s another to make best use of them.

Part 2: Tax-Wise Investment Techniques. In our last piece, we introduced some of the tools of the tax-planning trade. These include tax-sheltered accounts for saving toward retirement, healthcare, and education, as well as tax-efficient tools for charitable giving, emergency spending, and estateplanning. .

Unrelated Business Taxable Income (UBTI): Investors holding hedge funds in tax-advantaged accounts (IRAs, 401(k)s) may face unexpected UBTI taxes. Net Investment Income Tax (NIIT): Investors earning passive income from hedge funds may be subject to an additional 3.8% Net Investment Income Tax (NIIT): A 3.8%

Only 26% of Americans have an estateplan. If you’re thinking, “But my clients are high-net-worth…many more have an estateplan.” These numbers show an opportunity for tax practices to build deeper, meaningful relationships with their clients, helping them to navigate some of life’s most challenging financial decisions.

Gift Tax Exemptions Each year, you can give up to $17,000 to any number of people tax-free. This means that if you have two children, you can give each of them $17,000 without a tax penalty in 2023. [1] 1] This can be something you do as part of your estateplan.

Your business advisory team may consist of: a business broker or M&A advisor, accounting and tax advisors, and transaction/M&A attorney. On the personal side, your financial advisor , estateplanning attorney, and CPA/tax advisor should be involved throughout the process.

To help you achieve your goals, knowledgeable advisors take multiple aspects of financial planning into account. The following areas are among the most vital to discuss with high-net-worth clients: EstatePlanning. Estateplanning for high-net-worth individuals is also significant because recent developments in U.S.

Long-term goals typically encompass retirement planning, wealth preservation and estateplanning. They are well-versed in various aspects of financial planning, including investments, retirement planning, estateplanning and tax management. Scan the QR code below to connect with us.

Look at those discretionary expenses that might not be necessary (cable TV, that Hulu account you never watch, the Pandora music you don’t listen to, etc). Nothing will nuke your financial plan like high credit card debts and other high rate liabilities. Nuke those I-Bond and “high yield savings” accounts.

Depending on your situation, you may need the help of a financial advisor or an accountant. Dear Zoe Experts, I’ve been looking for taxplanning guidance and am deciding whether to hire a financial advisor or an accountant. Depending on your situation, you may need the help of a financial advisor or an accountant.

Together, both types of insurance plans provide a safety net for unexpected medical expenses and serve as an alternative strategy to shield your retirement nest egg from potential financial shocks. With improved healthcare accessibility and a vibrant lifestyle, the urgency to plan for the future may seem less pressing.

When selecting a tax professional, there are four main types to consider: Certified Public Accountant (CPA) Enrolled Agent (EA) Tax Attorney Non-credential Tax Professional Each type requires its own education and training, allowing them to provide specific services, which we’ll explore below.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content