This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

While many people approach their financialplanning with careful strategy, its easy to overlook the same level of intention when it comes to charitable giving. Lets explore several potentially effective financialplanning tools that may help you maximize your impact and meet your philanthropic goals.

One of the best tax deductions for a small business owner is funding a retirementplan. Beyond any tax deduction you are saving for your own retirement. You deserve a comfortable retirement. If you don’t plan for your own retirement who will? For the Solo 401(k) you will generally use a prototype plan.

30 years ago, when financialplans relied mainly on constant investment return projections derived from straight-line appreciation and time-value of money calculations, financial advisors began acknowledging and accounting for the variable and uncertain nature of investment returns.

30 years ago, when financialplans relied mainly on constant investment return projections derived from straight-line appreciation and time-value of money calculations, financial advisors began acknowledging and accounting for the variable and uncertain nature of investment returns.

Freelancing is liberating, but without a solid financialplan, it can also be unpredictable. As a freelancer, you juggle not only your craft but also your finances, taxes, and retirementplanning. That’s where financialplanning for freelancers comes in. Plan for taxes ahead of time 4.

(riabiz.com) Why women are still struggling to make progress in the world of financial advice. thinkadvisor.com) Vanguard is entering the cash management space with the Cash Plus Account. thinkadvisor.com) Retirement Baby Boomers were supposed to retire in penury. riabiz.com) Avise is a cooperative platform for advisers.

Historically, advisors haven't had many avenues to manage clients' 401(k) planaccounts, since unlike traditional custodial investment accounts, advisors generally lack discretionary trading authority in employer-sponsored retirementplans.

Historically, advisors haven't had many avenues to manage clients' 401(k) planaccounts, since unlike traditional custodial investment accounts, advisors generally lack discretionary trading authority in employer-sponsored retirementplans.

We’ve covered a lot of ground with regard to how various tax laws impact your retirementplans: pensions, IRAs, 403(b) and 401(k) plans. But we’ve primarily focused on the US income tax laws (the IRS) affect your plans – and there are many nuances that you need to take into account with regard to state tax laws.

Because when it comes to financialplanning, you’re ready to write it downand studies show that writing down your goals makes you 42% more likely to achieve them. Heres your top 10 financialplanning checklist for the new year. Three to six months worth of expenses tucked away in a high-yield savings account.

There are many important birthdays when it comes to retirementplanning. So, as you approach your retirement, it’s crucial to have a few of these in mind as key milestones. 1] IRA holders can contribute $7,500 a year to their accounts. [1] 1] But you can begin to claim at 62 if that fits into your financialplan.

Enjoy the current installment of "Weekend Reading For Financial Planners" - this week's edition kicks off with the news that the Department of Labor released the final version of its Retirement Security Rule (a.k.a.

There are many financialplanning considerations before, during, and after a divorce. A key part of the process from a financial standpoint is dividing the assets. Here are some key considerations when financialplanning for a divorce. Generally, couples split the value of their assets 50-50 (though not always).

Also in industry news this week: While the number of RIA M&A deals has not surged in 2024, the average size of deals has increased, demonstrating interest from (often private-equity-backed) firms in pursuing larger targets Off-channel communication tops the list of concerns amongst RIA compliance professionals, with advertising and marketing coming (..)

Know these 3 ages that can help you get the most out of your retirementaccounts. At age 50, workers with certain qualified retirementplans can make annual “catch-up” contributions in addition to their normal contributions. 3 Now, many retirees have more time to let their retirement savings grow tax-free.

Over the course of your life, you have probably acquired several different retirementaccounts, and you have likely considered many kinds of retirement strategies. 401(k) This is the most common kind of retirementaccount. 1] Traditional IRA IRA stands for Individual RetirementAccount.

One powerful but often overlooked tool is the Health Savings Account (HSA). Whether you’re new to HSAs or looking to optimize your existing one, this guide will break down everything you need to know about these tax-advantaged accounts. What is an HSA? It’s ideal for those who want to actively grow their HSA funds.

No one cares about your financial well-being more than you, so it's important to have a financialplan for yourself. Knowing how to make a financialplan will allow you to save money, afford the things you really want, and achieve long-term goals like saving for college and retirement. Retirement savings.

often fail to consider sequence of return, housing, longevity, health or family risks faced in retirement. Focus on Your RetirementPlan Rather Than a Magic Number. would be “How do I plan for retirement?“ Social Security is a federal retirementplan originally created under the Social Security Act of 1935.

No one cares more about your financial well-being than you, so having a personal financialplan is important. Knowing how to make a financialplan will allow you to save money, afford the things you want, and achieve long-term goals like saving for college and retirement. What is a full financialplan?

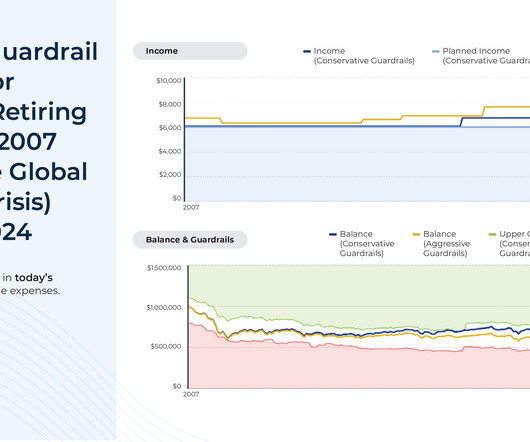

Monte Carlo simulations have become a central method of conducting financialplanning analyses for clients and are a feature of most comprehensive financialplanning software programs. However, the results of these simulations generally don't account for potential adjustments that could be made along the way (e.g.,

For these reasons and several others, it is essential to follow specific financialplanning tips for dual-income families. If you wish to learn about financial strategies that can help dual-income families plan their finances better, consider seeking the services of a professional financial advisor for the same.

In most cases, you can’t actually keep your money in your retirementaccounts forever. Even if you don’t need the money from your retirementaccounts, many of them will require you to begin withdrawing from them when you are 73 years old. [1] 4] So why can’t you just leave your money in your account?

You may be able to do everything online, otherwise contact the plan administrator at your company. There are a number of retirementplan options to consider. If you don’t have a retirementplan in place for yourself, do this today. You work way too hard not to be putting something away for retirement.

In retirementplanning, the concept of vesting is more than a contractual formality; it serves as a retention tool that incentivizes employees to remain with their employer for a certain period. To grasp how vested balance works and impacts your financial future, it’s essential to understand the notion of vesting.

2] With higher prices in consumer goods, retirees may have had to reevaluate their withdrawals and spending on retirementaccounts as their income became strained. In that case, it may be essential to review your financial position as these changes possibly affected how you cater to your short and longer-term retirement needs.

There are a few specialized financial tools for individuals with disabilities. ABLE (Achieving a Better Life Experience) accounts are one of those options. ABLE accounts are specialized savings accounts designed to help individuals with disabilities and their families save and invest money for disability-related expenses.

Of an estimated 104 million households seeking some level of financial advice, 88 million of those households want that advice from a financial professional. In this overview, we will explore the demographics of each stage, the financialplanning needs of people in each stage, and strategies for serving them.

You can also get to that number by asking yourself some fundamental questions: What age do you plan to retire? How many years do you have until you hit retirement? Where do your retirementaccounts stand now? How do you plan to spend your retirement? Moving, traveling, hobbies, etc.)

If you have student, personal or car loans, credit card debt or a mortgage, you need to have a plan on how to pay them off – and which ones to tackle first. While from a behavioral standpoint some suggest you should tackle low balance accounts first, a financialplanning approach suggests you tackle high interest rate debt first.

Petersen, CPA, CFP ® , CP, Affluent Wealth Planning The holidays are upon us! That must mean it’s time to roll up my sleeves and get to work on year-end financialplanning – with an emphasis on 2023 income tax. The benefit: more interest income on cash and money market accounts.

At some point we are bound to see a stock market correction of some magnitude, hopefully not on the order of the 2008-09 financial crisis. As someone saving for retirement , what should you do now? During the financial crisis there were many stories about how our 401(k) accounts had become “201(k)s.”

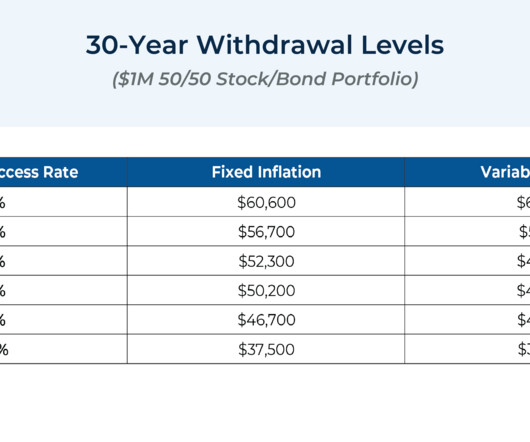

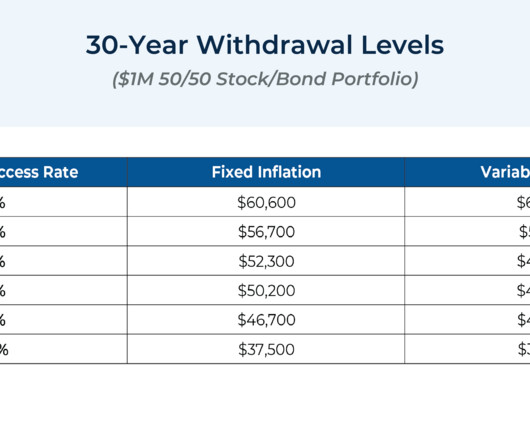

The 4% Rule is a general rule of thumb that is meant to guide your decisions on how much you can and should withdraw from your retirement savings each year. The purpose of adopting the rule is to keep a steady income stream while maintaining an adequate overall account balance for future years. The post Does the 4% Rule Really Work?

Rather I suggest an investment strategy that incorporates some basic blocking and tackling: A financialplan should be the basis of your strategy. View all accounts as part of a total portfolio. This means IRAs, your 401(k) , taxable accounts, mutual funds , individual stocks and bonds, etc. Photo credit: Flickr.

One of those options might be to set up a defined contribution plan such as a 401(k). [1] 1] A 401(k) will allow you to set aside some of your assets into a tax-advantaged account that can have market exposure and the potential to grow over time. [2] 4] This is a tax-advantaged account, much like a 401(k). [5]

Retirementplanning is an essential aspect of financial security, especially as one transitions from a phase of regular income to relying on savings and investments. With increased life expectancy, the modern retirementplan may need to account for not only a longer life but also for the increased expectations during this phase.

These types of plans commonly come in the form of pension plans. [1] 1] A pension plan guarantees a certain level of retirement benefit based on your salary and how many years you worked for the company. [2] 5] This is one reason why many employers have moved away from this kind of retirementplan.

The Five Phases of RetirementPlanning Published January 29, 2025 Reading Time: 2 minutes Written by: The Zoe Team Retirement is a journey with distinct phases, each requiring its own focus and preparation. Understanding these phases can help you approach your financial future with clarity and confidence.

For many people, the extent of their retirementplanning includes signing up for the plan at work – which is often more of a starting point than a comprehensive retirementplan. Here are some of the most common ones: 401(k) – A 401(k) is a retirementplan available through employers for employees.

We speak a secret language in financialplanning. Translating from the secret language of financialplanning, the sentence would read “Tammy specializes in insurance. She reviewed two types of annuity contracts often used for retirement and helped determine which one is the best fit for her client.” .

How you handle taxes and when you are taxed are two of the most important factors when it comes to retirementplanning. This type of account can be useful for some because when you withdraw under qualifying circumstances, you do not pay taxes.

How much should Gen X have in their retirementaccounts and when should they reach out to a financial advisor? The post RetirementPlanning for Generation X appeared first on Integrity FinancialPlanning, inc. Remember, you won’t be able to get to the money for a year. ” – Brian Bowen.

Whether you’re decades from retirement or quickly approaching it, some of these changes will likely impact you and your financialplan. Student Loan and Roth Account Matching Employers will be able to match employees’ student loan payments to a workplace retirementaccount beginning in 2024. Secure Act 2.0:

Roth IRA conversions present a significant challenge for retirement planners: pay taxes now or later? Moving funds from traditional IRAs to Roth accounts triggers immediate taxation but promises tax-free withdrawals in retirement. This flexibility becomes increasingly valuable as your retirement portfolio grows more complex.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content