This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Also in industry news this week: A study suggests that simplification is the top reason consumers combine their investmentaccounts, signaling that the onboarding process for new advisory client assets is a value-add in itself.

Among other measures, the proposal would amend the current 5-part test that determines fiduciary status for retirement accounts by defining as a fiduciary act a one-time recommendation to roll funds from a company retirement plan to an Individual Retirement Account (IRA), strengthen advice standards for independent insurance professionals, apply to (..)

There are many types of accounts for individuals to employ as part of their saving and investmentplan – IRAs, HSAs, FSAs, 529 plans, and more. However, there is one account that we haven’t covered before and doesn’t get a lot of attention when considering the alphabet soup of account types – an ABLE account.

Enjoy the current installment of "Weekend Reading For Financial Planners" - this week's edition kicks off with the news that RIA custodial platform Altruist announced that it is offering its portfolio accounting software for free to advisors who custody with the firm, offering the opportunity to advisory firms to reduce the costs of their tech stacks (..)

Also in industry news this week: While many pre-retirees feel unprepared for retirement, longitudinal survey data suggest most will end up living a comfortable retirement, suggesting a role for financial advisors to show them projections of what their retirement could actually look like According to a recent survey, high-net-worth individuals are largely (..)

Also in industry news this week: A bill that would allow funds in 529 plans to be used for postsecondary credentials, including the CFP certification, is gaining significant bipartisan support in Congress A recent survey identified key topics on which financial advisors and investors have mismatched views, from expected investment returns to how they (..)

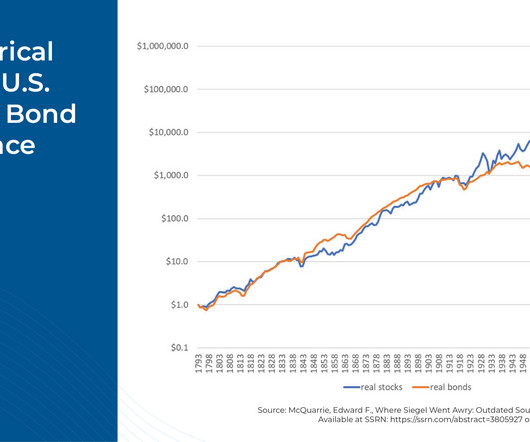

First is the fact that stocks (specifically because they carry a higher risk level) have not always outperformed bonds, and while stocks should carry a risk premium, advicers can turn to Monte Carlo simulations to consider a wider dispersion of outcomes, versus relying on 'expected' returns when developing investmentplans.

Also in industry news this week: Backers announced the new Texas Stock Exchange, which seeks to provide companies with a lower-cost alternative to the NYSE and Nasdaq, which, if successful, could create a more competitive landscape and potentially better execution and reduced trading costs for financial advisors and their clients The American College (..)

We start with several articles on retirement planning: Data showing where American retirees currently stand, from their average net worth to how they spend each hour of the day How, according to a recent study, delaying Social Security benefits typically leads to greater lifetime wealth than claiming benefits early in order to reduce portfolio withdrawals (..)

Three to six months worth of expenses tucked away in a high-yield savings account. We encourage you to reach out directly to us with your list of specific goals and not only will you find yourself more accountable but it helps us calendar reminders and check-ins to make sure we’re on track with you. A good rule of thumb?

InvestmentPlanning Options achen Mon, 10/16/2017 - 10:24 The decision to sell or hold a concentrated position may sound simple, but these situations are often more complex than they appear. They require the investor to reconcile investment dynamics, tax considerations and a variety of subjective, emotional factors.

InvestmentPlanning Options. They require the investor to reconcile investment dynamics, tax considerations and a variety of subjective, emotional factors. Mon, 10/16/2017 - 10:24. The decision to sell or hold a concentrated position may sound simple, but these situations are often more complex than they appear.

I created this list of financial advisors for small accounts (less than $300,000 in assets) because there are alot of schmucks out there hawking crap products to people with portfolio of this size, and I don’t think it’s fair. Transform Retirement www.transformretirement.com Avg account size: Approx. Three Creeks Capital – Ryan A.

This article will discuss the five pillars of retirement planning and why they are a critical component of your retirement plan. At its core, investmentplanning ensures that your financial resources are strategically allocated to various asset classes in accordance with your risk tolerance and investment objectives.

Inherited cash, stocks, or a brokerage account. Inheriting money or taxable investmentaccounts has some big benefits. Jump-starting (or catching up on) retirement savings by investing the money in a brokerage account. Inherited IRA or retirement account. Then, you can treat the account as your own.

Are you considering opening a certificate of deposit (CD) account? Our CEO, Marianela Collado , CPA/PFS, CFP®, CDS®, was recently quoted in MarketWatch sharing her insights on the process of opening a CD account. It’s always good to know why you are investing in a CD and whether that helps you reach your long-term goals.”

What's unique about Dann, though, is how he has channeled the anxiety of having imposter syndrome, which still causes him to be nervous before every client meeting (despite having 17 years of experience in the financial advisory business), as a means to hold himself accountable to always be doing the best he can for his clients, which has allowed Dann (..)

Even though the federal government has rescued SVB and guaranteed all deposits over the FDIC insurance limit of $250,000 per account, that doesn’t mean they will be doing it again for other banks. In the United States, any individual account with a balance of up to $250,000 at a bank is insured. and are not protected by SIPC.

That’s more than a whole percentage point higher than present inflation rates and a far cry above savings accounts. The average high-yield savings account is only paying 0.60% interest currently. So if you’re one of those people who has been complaining about how low the rate on your savings account is, then I-Bonds are for you.

Set Up Automatic Contributions and Max Them Out Once you’ve created a budget, you can set up automatic contributions to your retirement accounts. Many employers offer matching contributions for 401(k)s and other investmentplans. If your employer is one of them, take advantage by making the maximum contribution possible.

Overindulgence in information can lead to poor decisions, and excessive monitoring of your retirement account balance can result in stress. Checking your retirement account balance too often can have a psychological impact on you. Therefore, exploring the optimal frequency for checking your retirement account is essential.

When planning for retirement, one of the most important decisions you will likely make is which type of retirement account to use. The Roth Individual Retirement Account (IRA) and the pre-tax retirement account are two common options. What is a pre-tax retirement account? What is a Roth IRA?

If you have a million dollars to invest or anywhere close to that, the steps below can help you grow your money so it lasts a lifetime. Ad Robo-Advisors move with the market to ensure your investments. That plan that accounts for all your hopes, dreams, and wishes should then dictate the investments you choose.

As college costs rise, qualified tuition plans, or 529 college savings plans, can be an option for clients to save for their child or grandchild’s (or even their own!) These accounts can help your clients’ beneficiaries save for college and the funds can be used for various expenses relating to K-12 and higher education.

They can assess your financial situation, long-term goals, risk tolerance, and investment preferences to create personalized strategies. They can also help you optimize your savings and investmentplans, ensuring that you maximize your earning potential while minimizing risks. Tax planning is not solely about federal taxes.

To sweeten the deal, Robinhood didn’t require account minimums, so even investors with limited capital could start investing. Gone were the restrictions of many investing platforms with account minimums and hefty trading commissions. Margin accounts? ? million individual brokerage accounts. X X X X X X ?

So, when referencing an income generation investment strategy, oftentimes, they refer to this concept of scheduled cash returns as a key characteristic of the investment strategy. What is a Total Return Investment Strategy? The total return strategy takes a different approach to an investmentplan.

Without periodic rebalancing, your investment mix will change as the market fluctuates, falling out of alignment with your target investment mix. To rebalance your portfolio, you’ll buy and sell certain investments to realign to your accounts with your desired asset allocation.

1. Employer match on 401(k) plans. There’s not a lot of mystery surrounding the 401(k) retirement and savings investmentplan. 2. Health savings accounts. The health savings account, or HSA, can be a great tool to boost retirement savings. It’s been around for a long time.

The post Part 2: Tax-Wise Investment Techniques appeared first on Yardley Wealth Management, LLC. Part 2: Tax-Wise Investment Techniques In our last piece, we introduced some of the tools of the tax-planning trade. Building: Are you maxing out your contributions to appropriate tax-sheltered accounts?

The post Part 2: Tax-Wise Investment Techniques appeared first on Yardley Wealth Management, LLC. Part 2: Tax-Wise Investment Techniques. In our last piece, we introduced some of the tools of the tax-planning trade. As you manage your investmentaccounts …. It’s one thing to have the tools.

residents 18+ and subject to account approval. Ready to Start Investing? Whether you are hoping to start investing small amounts of money or you have a lump sum of cash to get started, you should know that investing isn’t necessarily a “set it and forget it” activity. Open an Account Today.

I sort of think of tax loss harvesting as the eharmony of investmentplanning. At its core, it’s about matchmaking and there are three core steps to making it all work: Step 1: You identify equities in your taxable accounts — stocks, mutual funds, bonds, as examples — that aren’t performing well.

Understanding Tax Liability in InvestmentPlanning To optimize your portfolios performance, it’s crucial to consider tax liability alongside investment gains. In my opinion, income taxes, capital gains taxes, and estate taxes are the most important categories for investmentplanning. What Is Tax Liability?

In addition, when you start to cut back, use effective money-saving tips, and use high-interest accounts, you may find that the cents start to turn into dollars fast and you find that you are able to save 50k. Figure out a payment plan that works for you—and your other investmentplans—and take things from there.

Women’s financial plans are unique, so their investing strategies should be, too. Find out more about women and investing, and discover ideas for creating your own investmentplan. It was also found that millennial women are investing outside of their retirement more often than previous generations.

A strategy for managing your investments is also key: understanding your risk capacity vs appetite, balancing a need for a current income stream and future growth, and ways to be more tax efficient in taxable accounts. Put the plan into action. A liquidity event is a great opportunity to develop a long-term investmentplan.

Most employer retirement plans allow you to save on a tax-deferred basis, meaning that contributions into these types of accounts are not considered in calculating your taxable income. . Retirement plans, such as 401(k) and 403(b) plans, allow employees to contribute a portion of their salary up to a federal limit ($20,500 in 2022).

But for those investors not blessed with the power of prediction, it’s better to take a long-term approach: devise a stable investingplan, invest in low-cost index funds that offer a stable array of stocks and bonds, and then do nothing.

What does my savings account look like? And do I have any money invested? Make a budget Budgeting is a key part of how to create a financial plan that works. Track your spending A master plan for your money should be an accurate representation of your finances, which means accounting for exactly where your money is going.

A market downturn at the start of retirement, hitting portfolio values when retirees begin to take account withdrawals, can be unsettling, even for seasoned investors. It’s not surprising to see many investors checking their retirement account balances more than three times per week (53% of women and 34% of men report doing this*).

A goal-based investing approach is one such strategy. It stands out as it focuses directly on your goals, determining the amount of money you need to achieve your financial goals, and then developing an investmentplan designed to achieve those goals within a specific timeframe. 5 steps involved in goal-based investing 1.

Are you good with numbers, accounting, and financial planning? If yes, then DIY financial planning might be a good option for you. On the other hand, if you tend to struggle with budgeting or find financial planning overwhelming, then professional money management could be a better solution.

Let’s demystify the lingo and break down some of the most common retirement plans, so you can determine the best retirement plan for you: Common Retirement Accounts Whether you work for a large company, a small business, or yourself, there are retirement savings accounts that will work best for your situation.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content