This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

And as 2024 draws to a close, we wanted to highlight 24 of the most popular and insightful articles that were featured throughout the year (that you might have missed!).

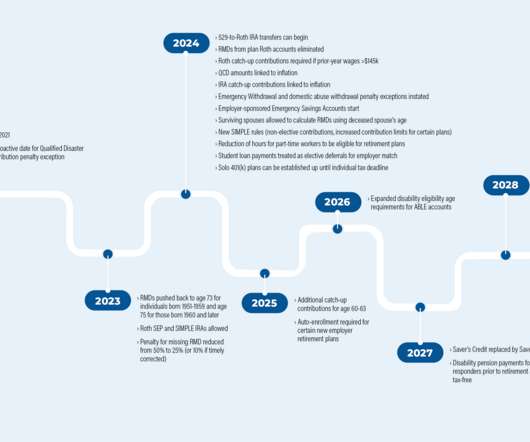

The Setting Every Community Up for Retirement Enhancement (SECURE) Act, passed in December 2019, brought a wide range of changes to the retirementplanning landscape, from the death of the ‘stretch’ IRA to raising the age for Required Minimum Distributions (RMDs) to 72. In addition, SECURE 2.0

The Setting Every Community Up for Retirement Enhancement (SECURE) Act, passed in December 2019, brought a wide range of changes to the retirementplanning landscape, from the death of the ‘stretch’ IRA to raising the age for Required Minimum Distributions (RMDs) to 72. In addition, SECURE 2.0

Like gardening or working out, taxplanning is one of those activities where you get out what you put in. Taxplanning is similar in the sense that you can put work in on the front end that youll reap benefits from later. Many of us just do tax preparation, dropping off a shoebox of documents with a CPA for the weekend.

Retirementplanning is a critical part of financial security that many women still overlook. However, remember that as a woman, you have a longer life expectancy than a man, which means retirementplanning is even more important. Consider early retirementtaxplanning.

In late 2019, Congress passed the Setting Every Community Up for Retirement Enhancement (SECURE) Act, introducing several significant changes to retirementplanning. This shift has led financial advisors to explore new strategies for mitigating the resulting tax-planning challenges.

Within this framework, the concept of the five pillars of retirementplanning emerges as a valuable strategy. These pillars provide a comprehensive framework for building a resilient and sustainable plan. In addition to traditional health insurance, you can also explore the Health Savings Account (HSA).

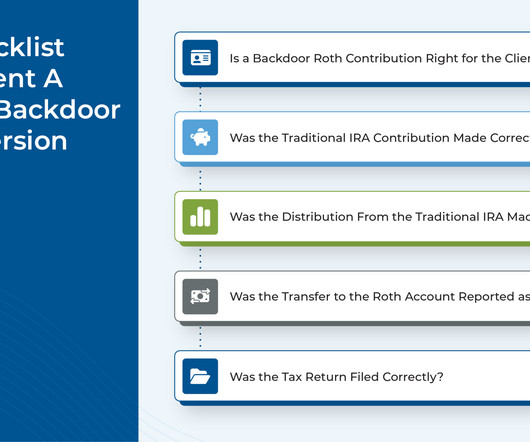

There are many taxplanning strategies that allow financial advisors to demonstrate the ongoing value they provide to clients in exchange for the fees they charge. Advisors also can support the backdoor Roth process by communicating with clients' tax preparers about the strategy and why they are recommending it for their mutual client.

Although any investor with earned income can make a non-deductible contribution to an IRA (up to $7,000 in 2024-2025 if under age 50) and still take advantage of tax-deferred growth, it still may not be advisable. Many people end up paying taxes twice. To calculate the tax-free percentage: Your Total Basis (e.g. Yes and no.

This month's edition kicks off with the news that digital estate planning platform Wealth.com has raised a whopping $30 million in Series A funding, following on the heels of Vanilla's follow-on $20M capital round just a few months ago – which on the one hand reflects the anticipated enthusiasm for solutions that can help advisors efficiently (..)

And as 2023 draws to a close, we wanted to highlight 25 of the most popular and insightful articles that were featured throughout the year (that you might have missed!).

Here’s how it breaks down for 2023-2024: If a couple’s total retirement income is between $32,000 and $44,000, up to 50% of Social Security benefits could be taxable. If their income is over $44,000, up to 85% could be taxed! Planning ahead helps make the transition to retirement smoother and keeps finances on track!

If you’ve just inherited a retirementaccount like an IRA or 401(k) from a parent, sibling, or relative, you may be unsure about what your options are and what to do next. Most non-spouse beneficiaries inheriting an IRA, 401(k), or retirementaccount from the original account owner must take the money in 10 years.

Once upon a time, people would put money in their 401(k) or IRA accounts and know that – should their retirement savings outlive them – their loved ones would inherit the rest and all would essentially be well. . How Did the SECURE Act Affect Inherited RetirementAccounts? Convert the Accounts to a Roth IRA.

When you are presented with the option to distribute your assets, you will have the choice to roll them into an IRA or place the stock into a taxable account and then roll the remaining assets into an IRA or 401(k). In addition, shares of employer securities for the NUA must be moved in-kind to a taxable brokerage account.

For example, they could make most of their charitable contributions and medical expenditures in a year they plan to itemize. Optimize retirementplan contributions The maximum allowable 401(k) contribution for 2023 is $22,500, with a $7,500 additional contribution, if the plan allows, for taxpayers who are 50 and over.

One of those options might be to set up a defined contribution plan such as a 401(k). [1] 1] A 401(k) will allow you to set aside some of your assets into a tax-advantaged account that can have market exposure and the potential to grow over time. [2] 4] This is a tax-advantaged account, much like a 401(k). [5]

just upended retirementplanning…again. The age when retirees must begin drawing from non-Roth retirementaccounts increases to 73 in 2023, then 75 in 2033. Raising the age when withdrawals must begin is great as it gives investors more planning opportunities. The Secure Act 2.0

Your retirement income plan may be sending up bubbles, too, whether around Social Security, retirementaccount distributions, taxes or somewhere else – and these holes need to be patched up right away. So, to help your retirementplan be more airtight, let’s look at a few of the common leaks.

As such, one of the most important retirement income resources is Social Security, which provides retirees inflation-adjusted income for life. Making the right decisions around claiming Social Security — based on your spending needs, longevity and taxplanning — could mean the difference between meeting your retirement goals or not.

These contributions not only provide immediate tax relief but help secure longer-term financial stability during retirement. 401(k) Plans: Contribute the maximum allowable amount for 2024 : $23,000 if youre under 50, or $30,500 if youre 50 or older. Available to taxpayers aged 70.5

Last year’s considerable losses and market fluctuations underscore the need for clients to assess their retirementplans to ensure it aligns with their objectives, financial situations, timelines, and attitudes toward market volatility. You can help them start the year right by conducting a retirement checkup.

The 4% Rule is a general rule of thumb that is meant to guide your decisions on how much you can and should withdraw from your retirement savings each year. The purpose of adopting the rule is to keep a steady income stream while maintaining an adequate overall account balance for future years. The post Does the 4% Rule Really Work?

If you’re looking for ways to invest after your 401(k) or 403(b) at work, you likely have three options: a brokerage account, IRA, or Roth IRA. Investing after maxing out a 401(k) is smart, especially since your retirementaccounts may not be enough to fully fund the lifestyle you want.

Retirementplan savers looking to mitigate the risk of higher taxes in the future may benefit from making after-tax contributions to employer plans, which may be transferred to Roth accounts. Our Bill Cass details a “mega backdoor” Roth strategy.

Backdoor strategies are retirement contribution methods that allow individuals to bypass income limits and contribute to tax-advantaged retirementaccounts. The strategies typically involve making after-tax contributions to a traditional IRA or 401(k), then converting those funds into a Roth IRA or Roth 401(k).

How you handle taxes and when you are taxed are two of the most important factors when it comes to retirementplanning. There are also Roth 401(k)s that have a similar tax treatment but are subject to some different rules.

In the new bill, the age when retirees must begin drawing from non-Roth tax-deferred retirementaccounts would increase to 73 in 2023 and 75 in 2033. would permit employers to make matching contributions to an employee’s 401(k) and 403(b) retirementplan, even if the worker isn’t saving themselves.

Among the most notable changes include a significant step towards ‘Rothification’ through expanded use, new requirements, and even a way to move money from college savings accounts to a Roth IRA. Here are the top five Roth-related retirement changes following the passing of Secure Act 2.0. 529 plan to Roth IRA rollovers.

What are appropriate checklists for year-end taxplanning? Tax planners often develop checklists to guide taxpayers toward year-end strategies that might help reduce taxes. Certain tax benefits may be available if you can claim an individual as a dependent. Family taxplanning. Employee matters.

The simple examples above only illustrate the state tax impact, but federal tax implications will also apply. Further, both examples ignore other sources of income, such as wages, pre-taxretirementaccount distributions, dividends, etc., that could increase the tax due from the surtax.

This advanced language processing technology has also greatly impacted the financial advisory sector, prompting a critical question: Can ChatGPT replace human financial advisors in retirementplanning? Personalized guidance, empathy, and a deep contextual understanding are integral to effective retirementplanning.

This tax benefit is scheduled to sunset at the end of 2026. Taxplanning for 2026 Depending on your situation, income, and goals, your planning options will vary. As with anything in taxplanning, it’s important not to let the tax-tail wag the dog.

The post Part 1: The Tools of the Tax-Planning Trade appeared first on Yardley Wealth Management, LLC. Part 1: The Tools of the Tax-Planning Trade Whether you’re saving, investing, spending, bequeathing, or receiving wealth, there’s scarcely a move you can make without considering how taxes might influence the outcome.

The post Part 1: The Tools of the Tax-Planning Trade appeared first on Yardley Wealth Management, LLC. Part 1: The Tools of the Tax-Planning Trade. Whether you’re saving, investing, spending, bequeathing, or receiving wealth, there’s scarcely a move you can make without considering how taxes might influence the outcome.

Retirementplanning: Calculate retirement needs and contribute regularly to retirementaccounts. TaxPlanning: Optimize tax efficiency through strategies such as retirement contributions, tax-deferred accounts, and deductions and credits.

The reality for those with various employers is that untracked retirement savings might lead to missed financial growth opportunities and instability. Diligent oversight and management of these retirementaccounts is essential for anyone aiming to build a solid financial foundation for a comfortable and secure retirement.

With our deep expertise and qualifications in NUA strategies, our experts are adept at navigating the complexities of tax-efficient retirementplanning. Explore the Fortune Financial advantage in transforming how you manage your retirement assets and bringing you closer to achieving your financial dreams.

Here are a few examples of how they can help with your financial planning: Create a Comprehensive Financial Plan: A fiduciary and fee-only advisor can work with you to create a comprehensive financial plan that takes into account your goals, assets, and risk tolerance.

If you think retirementplanning moves stop at retirement, think again. Although it won’t make sense in every situation, retirement can be a unique opportunity for Roth conversions for some investors. But there are other ways to go about taxplanning. This can be done through Roth conversions.

Assessing the tax structure of your state and constructing your retirementplan and financial strategy around your state’s tax system can help you stay a step ahead in retirement. Utilize a Smart RetirementAccount Withdrawal Strategy Choose a withdrawal strategy that works for you. [2]

Part 3: Tax-Wise Financial Planning In our last two pieces, we covered some tools of the tax-planning trade, as well as how to deploy them for tax-efficient investing. But taxplanning isn’t just for your investments. But we can weave each event into the tax-planning fabric of your financial life.

Part 3: Tax-Wise Financial Planning. In our last two pieces, we covered some tools of the tax-planning trade, as well as how to deploy them for tax-efficient investing. . But taxplanning isn’t just for your investments. Each can translate into tax-planning challenges and opportunities: .

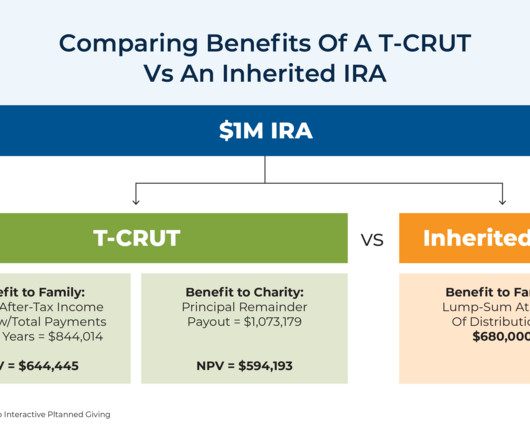

How it works There are numerous instruments someone can choose from, for example: A Donor-Advised Fund (DAF) – A separately identified fund or account is maintained and operated by a “sponsoring organization.” The accounts are composed of contributions made by individual donors. A CRT may be partially tax-deductible right away.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content