This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

And as 2024 draws to a close, we wanted to highlight 24 of the most popular and insightful articles that were featured throughout the year (that you might have missed!).

For example, if taxes were expected to rise in the future, it would be better to contribute to a Roth retirementaccount (which is taxed on the contribution, but not upon withdrawal) than to a traditional pre-taxaccount (which is tax-deductible today but is taxable on withdrawal). Read More.

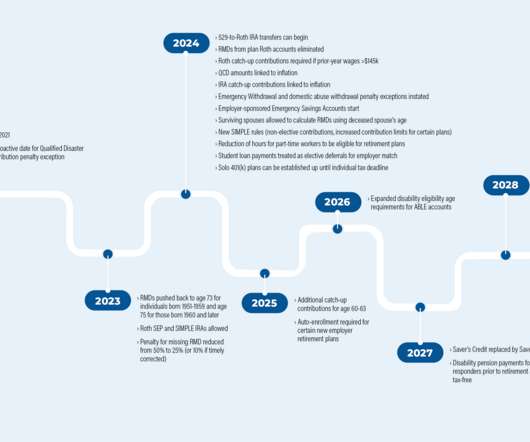

The Setting Every Community Up for Retirement Enhancement (SECURE) Act, passed in December 2019, brought a wide range of changes to the retirementplanning landscape, from the death of the ‘stretch’ IRA to raising the age for Required Minimum Distributions (RMDs) to 72. In addition, SECURE 2.0

The Setting Every Community Up for Retirement Enhancement (SECURE) Act, passed in December 2019, brought a wide range of changes to the retirementplanning landscape, from the death of the ‘stretch’ IRA to raising the age for Required Minimum Distributions (RMDs) to 72. In addition, SECURE 2.0

(podcasts.apple.com) Taxes The 0% capital gains bracket is an opportunity. whitecoatinvestor.com) Why it's important to do taxplanning before you start taking Social Security. nytimes.com) Retirement Six myths in retirement including 'You don't need a financial advisor.'

Proactive year-end taxplanning can lead to significant savings and set you up for financial success in the new year. Checklist: Year-end TaxPlanning Strategies Review the following tax strategies with your tax advisor and/or financial advisor before the end of the year. GET STARTED 1.

Like gardening or working out, taxplanning is one of those activities where you get out what you put in. Taxplanning is similar in the sense that you can put work in on the front end that youll reap benefits from later. Many of us just do tax preparation, dropping off a shoebox of documents with a CPA for the weekend.

taps.substack.com) Advisers Wade Pfau on why taxplanning in retirement is so challenging. blog.xyplanningnetwork.com) What it takes to set up a Charitable Gift Annuity account. (kitces.com) How to send a follow-up e-mail. thinkadvisor.com) There is no one-size-fits-all for managing a couple's finances.

Enjoy the current installment of "Weekend Reading For Financial Planners" – this week's edition kicks off with the news that a recent survey indicates that clients of financial advisors are more confident than others about their financial preparedness for retirement and are more likely to have a financial plan in place that can weather the ups (..)

In late 2019, Congress passed the Setting Every Community Up for Retirement Enhancement (SECURE) Act, introducing several significant changes to retirementplanning. This shift has led financial advisors to explore new strategies for mitigating the resulting tax-planning challenges.

Taxes are among the most common concern for people in retirement. You might be wondering how to start thinking about your tax strategy so you aren’t taxed more than you need to be. These three mistakes can help start the conversation about what a comprehensive tax strategy might look like for you.

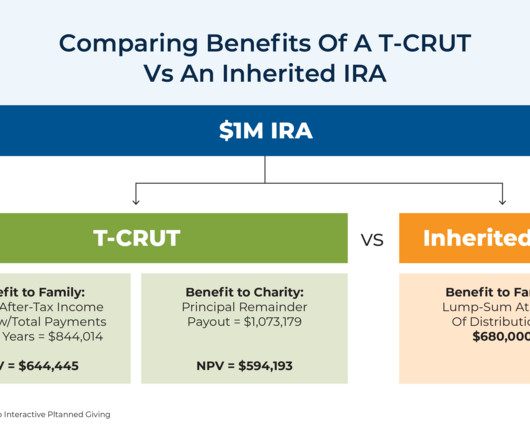

If you’ve just inherited a retirementaccount like an IRA or 401(k) from a parent, sibling, or relative, you may be unsure about what your options are and what to do next. Most non-spouse beneficiaries inheriting an IRA, 401(k), or retirementaccount from the original account owner must take the money in 10 years.

While this will help seniors keep pace with rising prices, it also creates taxplanning opportunities for advisors and raises the possibility that the Social Security Trust Fund could be depleted sooner than expected. Why accounting firms have become hot acquisition targets for RIAs.

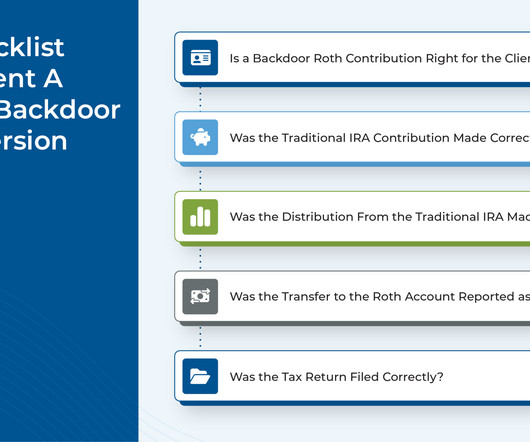

Although any investor with earned income can make a non-deductible contribution to an IRA (up to $7,000 in 2024-2025 if under age 50) and still take advantage of tax-deferred growth, it still may not be advisable. Many people end up paying taxes twice. To calculate the tax-free percentage: Your Total Basis (e.g. Yes and no.

Once upon a time, people would put money in their 401(k) or IRA accounts and know that – should their retirement savings outlive them – their loved ones would inherit the rest and all would essentially be well. . How Did the SECURE Act Affect Inherited RetirementAccounts? Convert the Accounts to a Roth IRA.

There are many taxplanning strategies that allow financial advisors to demonstrate the ongoing value they provide to clients in exchange for the fees they charge. Advisors also can support the backdoor Roth process by communicating with clients' tax preparers about the strategy and why they are recommending it for their mutual client.

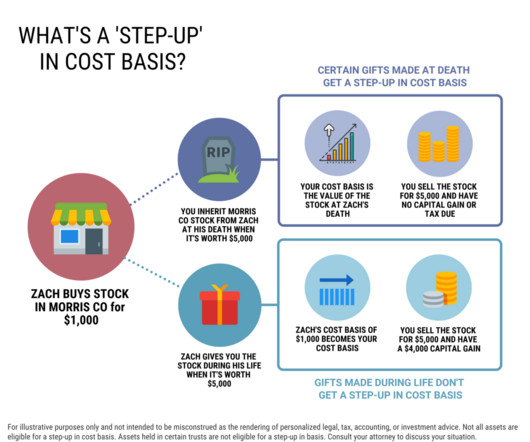

Conversely, if the original account owner gifted the stock while living, the recipient retains purchaser’s carryover basis and holding period ($100 in this example). The tax benefits of the step-up in basis provision cannot be understated. Retirementaccounts and IRAs do not receive a stepped up basis. Yes and no.

This month's edition kicks off with the news that digital estate planning platform Wealth.com has raised a whopping $30 million in Series A funding, following on the heels of Vanilla's follow-on $20M capital round just a few months ago – which on the one hand reflects the anticipated enthusiasm for solutions that can help advisors efficiently (..)

Which means that by taking into account a client's net worth, realistic liability risks, and level of sophistication, advisors can help assess what types of strategies may be appropriate for the client to explore. For instance, qualified plan assets (e.g., tenancy by the entireties and community property).

million in assets to both retire and pass on a legacy interest (though many have yet to establish an estate plan), according to a recent survey. Enjoy the current installment of "Weekend Reading For Financial Planners" – this week's edition kicks off with the news that affluent Americans believe they need an average of $5.5

Which suggests that while firms might be tempted to zero in on compensation when it comes to retaining advisors, focusing on these other factors (which do not necessarily involve hard dollar expenses) could pay off in the form of increased advisor (and client) retention over time.

Retirementplanning is a critical part of financial security that many women still overlook. However, remember that as a woman, you have a longer life expectancy than a man, which means retirementplanning is even more important. Suppose you significantly reduce your stock investments close to or after retirement.

These include the surviving spouse, minor children of the decedent, a disabled or chronically ill individual as assessed at the time of the decedent’s passing, and other individuals who are no more than ten years younger than the deceased account owner. 15:46] Timing distributions strategically can reduce tax liability.

At a high level, the challenge of serving next-generation clients is that, although they may not be able to afford higher fees, their financial needs are just as complex – if not more so – than those of retired clients. robo-managed portfolios) at a lower fee.

Retirement is different for folks who are running a small business. Your retirement is something that isn’t set up by an employer, and you often must manage it on your own. If you are running your own business and are interested in setting yourself up for retirement, contacting a financial advisor can be a great idea.

Achieving financial freedom in retirement requires meticulous planning, dedicated effort, and strategic management. Without a solid plan, you risk drifting without direction. Within this framework, the concept of the five pillars of retirementplanning emerges as a valuable strategy.

How you handle taxes and when you are taxed are two of the most important factors when it comes to retirementplanning. There are also Roth 401(k)s that have a similar tax treatment but are subject to some different rules.

Financial advisors play a crucial role in assisting you before your retire. They can also help you optimize your savings and investment plans, ensuring that you maximize your earning potential while minimizing risks. Here are 5 benefits of hiring a financial advisor after you retire: 1.

And as 2023 draws to a close, we wanted to highlight 25 of the most popular and insightful articles that were featured throughout the year (that you might have missed!).

As you move toward retirement, you can’t be content just to accumulate assets. You need to develop a retirement income plan that can help guide you when it comes time to turn savings into sustainable retirement income. of Social Security benefits are paid to retired workers and their dependents.

If you think retirementplanning moves stop at retirement, think again. Although it won’t make sense in every situation, retirement can be a unique opportunity for Roth conversions for some investors. For high earners, converting an IRA to a Roth IRA while you’re still working could be the worst time of all.

In this article, well examine the most effective end-of-year tax strategies to help maximize your deductions and reduce your taxable income. These contributions not only provide immediate tax relief but help secure longer-term financial stability during retirement. Available to taxpayers aged 70.5

Here’s how it breaks down for 2023-2024: If a couple’s total retirement income is between $32,000 and $44,000, up to 50% of Social Security benefits could be taxable. If their income is over $44,000, up to 85% could be taxed! Planning ahead helps make the transition to retirement smoother and keeps finances on track!

After you’ve spent your whole life working, you may find that in retirement, you want to give some money to charity. But if you are living off of income streams from sources like your retirementaccounts and Social Security, you may be worried about finding a way to make charity work for your financial picture.

Retirementplanning can be a bit complex. There are multiple factors to weigh in, right from healthcare and inflation to estate planning, business succession planning, taxplanning, and more. However, the main drawback to this can be the lack of foresight regarding what and how to plan.

If you’re looking for ways to invest after your 401(k) or 403(b) at work, you likely have three options: a brokerage account, IRA, or Roth IRA. Investing after maxing out a 401(k) is smart, especially since your retirementaccounts may not be enough to fully fund the lifestyle you want.

Congress is once again poised to make sweeping changes to the retirement and tax rules in the last two weeks of the year. retirement changes. retirement changes. In the new bill, the age when retirees must begin drawing from non-Roth tax-deferred retirementaccounts would increase to 73 in 2023 and 75 in 2033.

Every year brings changes in tax rules, and 2025 is no exception. Whether you are saving for retirement, running a business, or planning for your family’s future, these updates could affect your financial decisions throughout the year. Charitable Giving and TaxPlanning The tax rules continue to encourage generosity.

As you plan for retirement, it’s important to consider tax optimization strategies to minimize your tax liabilities. Here are three key ways to optimize taxes in retirement, based on information from sources published between 2022 and 2023.

As we begin our countdown to 2024, it is a great time to ensure your year-end taxplan is in place. Taxplanning is a vital component of meeting your overall financial goals. Our team of professionals is here to assist with your financial and taxplanning needs. You can access the webinar recording here.

just upended retirementplanning…again. The age when retirees must begin drawing from non-Roth retirementaccounts increases to 73 in 2023, then 75 in 2033. Raising the age when withdrawals must begin is great as it gives investors more planning opportunities. The Secure Act 2.0

For example, they could make most of their charitable contributions and medical expenditures in a year they plan to itemize. Optimize retirementplan contributions The maximum allowable 401(k) contribution for 2023 is $22,500, with a $7,500 additional contribution, if the plan allows, for taxpayers who are 50 and over.

While these can be avoided, there is another cash outflow that can considerably lower your savings and returns and is also hard to avoid – tax. Taxplanning is essential. Tax is charged on every penny you earn. Tax evasion is a crime, and missing tax payments can lead to legal hassles that can be hard to get out of.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content