This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

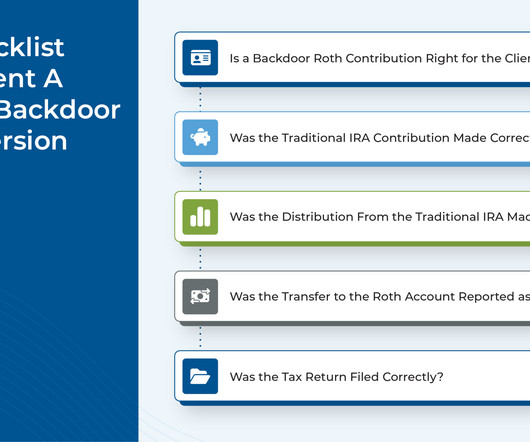

Proactive year-end taxplanning can lead to significant savings and set you up for financial success in the new year. Checklist: Year-end TaxPlanning Strategies Review the following tax strategies with your tax advisor and/or financial advisor before the end of the year.

For example, if taxes were expected to rise in the future, it would be better to contribute to a Roth retirement account (which is taxed on the contribution, but not upon withdrawal) than to a traditional pre-taxaccount (which is tax-deductible today but is taxable on withdrawal).

Misusing Retirement Accounts. Retirement accounts are a crucial piece of your retirement puzzle. It’s important to know how each retirement account is structured so you don’t end up paying penalty fees and missing out on any tax-advantaged perks of these accounts.

taps.substack.com) Advisers Wade Pfau on why taxplanning in retirement is so challenging. blog.xyplanningnetwork.com) What it takes to set up a Charitable Gift Annuity account. (kitces.com) How to send a follow-up e-mail. thinkadvisor.com) There is no one-size-fits-all for managing a couple's finances.

While this will help seniors keep pace with rising prices, it also creates taxplanning opportunities for advisors and raises the possibility that the Social Security Trust Fund could be depleted sooner than expected. Why accounting firms have become hot acquisition targets for RIAs.

Also in industry news this week: A probe by the Government Accountability Office found that the conflict-of-interest disclosures offered by many firms offering financial advice are often inadequate or confusing, making it hard for consumers to understand whether and when a financial professional is operating in their best interest A recent study has (..)

There are many taxplanning strategies that allow financial advisors to demonstrate the ongoing value they provide to clients in exchange for the fees they charge. Advisors also can support the backdoor Roth process by communicating with clients' tax preparers about the strategy and why they are recommending it for their mutual client.

Taxplanning might not top everyone’s list of leisure activities, but in the middle of tax season, theres a hidden opportunity. In this episode, we talk about five strategies you can use during tax season to create opportunities to help you reach your financial goals.

Which means that by taking into account a client's net worth, realistic liability risks, and level of sophistication, advisors can help assess what types of strategies may be appropriate for the client to explore. For instance, qualified plan assets (e.g., tenancy by the entireties and community property).

Also in industry news this week: A recent survey indicates that financial advisors continue to move towards ETFs and away from mutual funds when it comes to client portfolio recommendations, though a majority of advisors continue to see a role for active management in the investment management process A former employee has filed a lawsuit alleging (..)

Also in industry news this week: A coalition of organizations representing financial advisors is pressing Congress to include tax breaks for financial advisory fees amidst expected negotiations to address the pending expiration of several provisions of the Tax Cuts and Jobs Act A recent survey indicates that client referrals remain the chief source (..)

And while the near-constant drumbeat of proposed legislative actions that would further alter the estate planning landscape has led some planners to try to 'get ahead' of those changes by suggesting action in anticipation of those bills becoming laws, doing so can come with risks… especially when those proposals never come to fruition.

Also in industry news this week: Why industry groups representing investment advisers and others have blasted an SEC proposal that would significantly expand its Custody Rule A new study suggests that organic client growth and profit margins are the key factors driving RIA valuations, with the firm’s affiliation model having little to no impact (..)

The IRA and Roth IRA contribution limits are unchanged but income eligibility for tax-deductible IRA contributions and Roth IRA contributions have changed. Also updated: health savings accounts, flexible spending accounts, estate and gifting limits, qualified charitable distributions and other cost-of-living adjustments.

Also in industry news this week: 2 House committees this week advanced legislation that would halt implementation of the Department of Labor's new Retirement Security Rule, which, combined with ongoing lawsuits, threaten to derail the regulation either before or soon after it becomes effective in late September A Federal judge has put the future of (..)

This month's edition kicks off with the news that digital estate planning platform Wealth.com has raised a whopping $30 million in Series A funding, following on the heels of Vanilla's follow-on $20M capital round just a few months ago – which on the one hand reflects the anticipated enthusiasm for solutions that can help advisors efficiently (..)

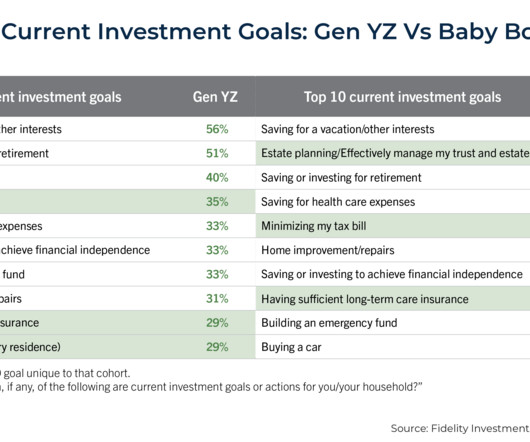

For example, most Millennial and Gen Z clients can open their own investing account and buy index funds online with only minimal guidance from their advisor, so full-service investing might not offer enough value to a next-generation client to justify an ongoing planning fee.

As we begin our countdown to 2024, it is a great time to ensure your year-end taxplan is in place. Taxplanning is a vital component of meeting your overall financial goals. Our team of professionals is here to assist with your financial and taxplanning needs. You can access the webinar recording here.

Holistic Financial Management Beyond investment advice, financial advisors offer comprehensive services such as taxplanning, estate planning, and risk management. This support can be important in maintaining discipline and making rational decisions amidst market fluctuations.

As Gio Bartolotta, Partner at GoJo Accountants , explains “ordinary” means the expense must be common and accepted within your trade or business, while “necessary” indicates it should help or be appropriate for running operationsnot necessarily indispensable.

In this episode, we talk in-depth about how, after years of working in an environment where she saw first-hand how ultra-high-net-worth clients keep and grow their wealth (and the lack of diversity among those clients), Kamila decided to build a practice that focused on providing holistic financial planning to communities of color with emerging wealth, (..)

For example, advisors who use a Customer Relationship Management (CRM) tool may be able to use that tool to narrow down the list of clients to those who are good tax-loss-harvesting candidates, such as those in higher tax brackets (who are likelier to realize more value from deducting capital losses). With these three tools (i.e.,

If you've heard of a DAF and are curious about incorporating it into your giving and taxplanning strategy, this article is for you. Key Takeaways: Contributions to a donor-advised fund reduce your tax bill in the year your contribution is made. What is a Donor Advised Fund? What are the costs of a DAF?

Also in industry news this week: Backers announced the new Texas Stock Exchange, which seeks to provide companies with a lower-cost alternative to the NYSE and Nasdaq, which, if successful, could create a more competitive landscape and potentially better execution and reduced trading costs for financial advisors and their clients The American College (..)

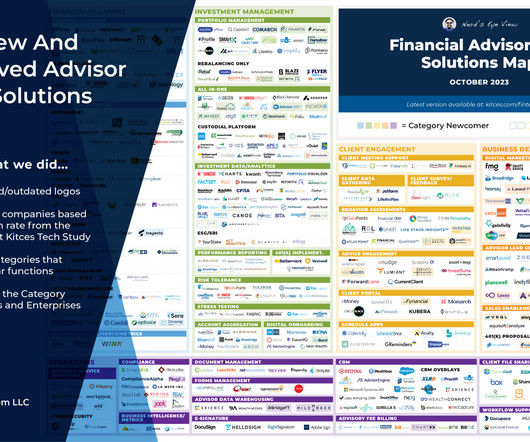

Welcome to the October 2023 issue of the Latest News in Financial #AdvisorTech – where we look at the big news, announcements, and underlying trends and developments that are emerging in the world of technology solutions for financial advisors!

We start with several articles on retirement planning: Data showing where American retirees currently stand, from their average net worth to how they spend each hour of the day How, according to a recent study, delaying Social Security benefits typically leads to greater lifetime wealth than claiming benefits early in order to reduce portfolio withdrawals (..)

While these can be avoided, there is another cash outflow that can considerably lower your savings and returns and is also hard to avoid – tax. Taxplanning is essential. Tax is charged on every penny you earn. It also includes your 401k and Individual Retirement Account (IRA) withdrawals from traditional accounts.

These contributions not only provide immediate tax relief but help secure longer-term financial stability during retirement. 401(k) Plans: Contribute the maximum allowable amount for 2024 : $23,000 if youre under 50, or $30,500 if youre 50 or older. Available to taxpayers aged 70.5

While a Roth conversion may never make sense for some individuals, for others, early retirement years may be the best time to convert pre-taxaccounts to tax-free Roth. Your current and projected future tax rate is often a main component of the decision, but there are other considerations and benefits as well.

Taxplanning serves as the cornerstone of the entire acquisition deal, extending far beyond a simple checkbox. Every element, from structure to price negotiations, hinges on understanding tax implications for all parties involved. To qualify for tax-free treatment under IRC Section 368 , attention to detail is essential.

Let us face ittech startups encounter a unique set of tax challenges that can make or break their financial future. The complex interplay between traditional tax regulations and the innovative nature of tech businesses demands smart planning from day one.

Donor-advised funds (DAFs) have emerged as powerful tools that deliver this exact combination, providing immediate tax advantages while offering flexibility to recommend grants to qualified organizations over time. At their core, donor-advised funds are specialized 501(c)(3) charitable accounts housed within public charities.

Within the accounting profession, Client Accounting Services (CAS) has emerged as a pivotal offering for entrepreneurial CPAs wishing to help their clients with more than just annual tax filings. Table of Contents What are Client Accounting Services (CAS)? What are Client Accounting Services (CAS)?

It would be difficult to create a holistic financial plan for any client without a full picture of their financial lives. Account aggregation gives financial professionals—and their clients—a complete and centralized view of the client’s financial information.

If their income is over $44,000, up to 85% could be taxed! This is why having a smart, well-rounded retirement plan that includes income planning and taxplanning is so important! Planning ahead helps make the transition to retirement smoother and keeps finances on track!

If you’re looking for ways to invest after your 401(k) or 403(b) at work, you likely have three options: a brokerage account, IRA, or Roth IRA. Investing after maxing out a 401(k) is smart, especially since your retirement accounts may not be enough to fully fund the lifestyle you want.

Cost-saving taxplanning can be much more difficult to implement after your company is well-established and has reached the stage where an IPO, merger, or acquisition becomes a likely event. ISOs can only be issued to employees, and the company issuing the ISO cannot take a tax deduction.

Consider spreading investments across different types of accounts, like tax-deferred accounts, to minimize the chance of incurring this additional tax. Charitable Giving and TaxPlanning The tax rules continue to encourage generosity.

Among the most notable changes include a significant step towards ‘Rothification’ through expanded use, new requirements, and even a way to move money from college savings accounts to a Roth IRA. 5 new changes to Roth accounts in Secure Act 2.0. 529 plan to Roth IRA rollovers. Prior to the passing of Secure Act 2.0,

Councilor, Buchanan & Mitchell is a full-service accounting and advisory firm in the Mid-Atlantic region in the Harness Wealth Advisor network. Below are some insights from Richard Morris, Executive Vice President and Director of Tax Services, and Alex Seleznev, Senior Investment Advisor and Chief Operating Officer of MBI, LLC.

By Mike Valenti, CPA, CFP ® , Director, TaxPlanning Corporate executives often receive the brunt of the U.S. tax system. Typically, most or all of their income is W-2 income and subject to the higher ordinary tax rates as well as FICA taxes.

Acts, what that means to you and your TaxPlanning in Retirement. Lastly, Larry will take your questions on TaxPlanning in Retirement so you can avoid unintended tax consequences in retirement. Mr. Pon is a Certified Public Accountant, Personal Financial Specialist, Certified. Guest commentator: Larry Pon.

Traditional IPO: Valuation, Lockup Period, and Employee Equity Founders have more options for reducing the tax consequences of an acquisition Founders are generally in the best position to engage in taxplanning and limit the taxable consequences associated with an acquisition.

While most taxpayers dont need to worry about estate and gift taxes, having significant assets can make them a challenge. Also, like most UHNW individuals, you may have income from several sources like investments, real estate, and business interests that may require special taxplanning. Donate to qualified charities.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content