This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

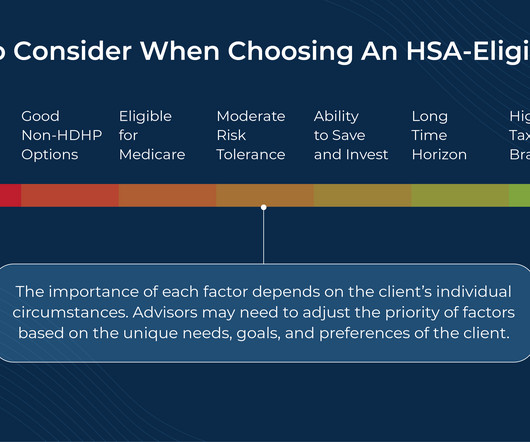

Health Savings Accounts (HSAs) have become an increasingly popular tool for financial advisors and their clients due in part to the 'triple tax savings' they offer: tax-deductible contributions, tax-free growth, and non-taxable distributions for qualifying expenses.

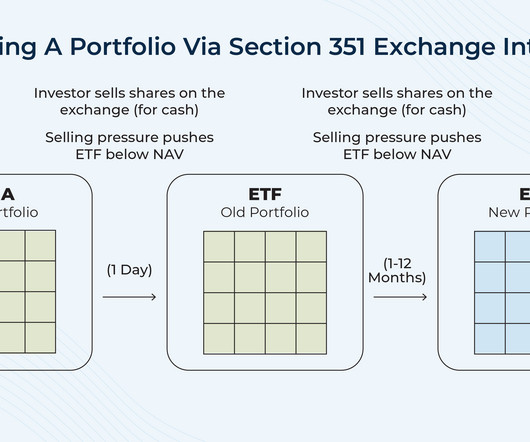

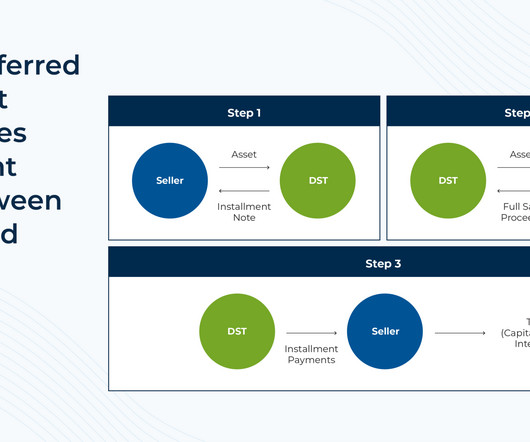

Following the long run-up in the US equity markets since the bottom of the 2008–2009 financial crisis, many investors with taxable investment accounts have likely found themselves with high embedded gains in their portfolios. If the exchange meets the requirements of Section 351, it is tax-deferred for investors.

Health Savings Accounts (HSAs) are one of the most popular savings vehicles because of their triple-tax advantage: account owners can take an above-the-line tax deduction for eligible contributions, growth in the account is tax-deferred, and withdrawals are tax-free if they are used for qualified healthcare expenses.

Speaker: Rita Keller - President of Keller Advisors, LLC

You've worked diligently and have built a glowing reputation grounded in your excellent skills in tax, accounting, and auditing. You're known as the “go-to” person when a client is faced with tax and financial decisions. You have a very successful firm -- but that’s not enough.

Would you like to diversify but also defer paying big capital gains taxes? I’m Barry Ritholtz and on today’s edition of at the money we’re going to discuss how to manage concentrated equity positions with an eye towards diversification and managing big capital gains taxes. None of these solutions are optimal.

The IRA and Roth IRA contribution limits are unchanged but income eligibility for tax-deductible IRA contributions and Roth IRA contributions have changed. Also updated: health savings accounts, flexible spending accounts, estate and gifting limits, qualified charitable distributions and other cost-of-living adjustments.

Over the last 60 years, the top Federal marginal tax bracket has steadily decreased from over 90% in the 1950s and 60s to 'just' 37% today. While it's true that the top marginal tax rate has decreased dramatically since the mid-20th century, the difference in the actual tax paid by most Americans has been far more modest.

Health savings accounts (HSA) provide another vehicle to save for retirement. Many of you have the option to enroll in high-deductible insurance plans that allow the use of a health savings account via your employer. HSA accounts can only be used in conjunction with a high-deductible health insurance plan. How the HSA works .

The robo advisor failed to tell some clients its tax-loss harvesting service only checked accounts on alternating days and not daily, as some materials claimed, according to the commission.

that incentivizes saving for these goals for American citizens – namely with tax-advantaged accounts such as 401(k) plans, IRAs, 529 college savings plans, and Health Savings Accounts (HSAs) – can impose hurdles on foreign nationals who rely on them for their own savings needs. However, the system in the U.S.

The combination with Harrison Berkman Claypool & Guard and its RIA enhances Coldstreams existing tax and consulting practice and brings its total AUA to $11.1

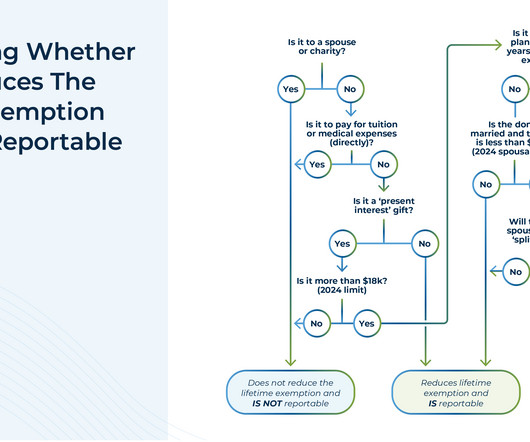

While all gifts could technically be considered taxable to the donor, the annual gift tax exclusion (currently at $18,000) provides for a practical allowance that makes it unnecessary to track and report every small gift (because no one wants to spend time accounting for the value of birthday gifts like bikes, books, or cash!).

Roth conversions are, in essence, a way to pay income taxes on pre-tax retirement funds in exchange for future tax-free growth and withdrawals. Conversely, if the opposite is true and the converted funds would be taxed at a lower rate upon withdrawal in the future, then it makes more sense not to convert.

At the Money: How to Pay Less Capital Gains Taxes (January 24, 2024) We’re coming up on tax season, after a banner year for stocks. Successful investors could be looking at a big tax bill from the US government. On this episode of At the Money, we look at direct indexing as a way to manage capital gains taxes.

Each of these account types has its pros and cons, which I have outlined below. Once you open this account, it functions the same way as every other bank account does for deposits and withdrawals, and you can order a debit card for your child once they get older for spending purposes.

Tax-loss harvesting – i.e., selling investments at a loss to capture a tax deduction while re-investing the proceeds to maintain market exposure – is a popular strategy for financial advisors to increase their clients’ after-tax investment returns. With these three tools (i.e.,

And for many business sales that create capital gains of more than $500,000, the one-time spike in taxable income created by selling a business can bump the seller into a higher income tax bracket, requiring them to forfeit a significant chunk of their funds needed for retirement to pay their own tax bill on the sale. Under IRC Sec.

investmentnews.com) Retirement savings Capitalize is helping people transfer old 401(k) accounts. (riabiz.com) Going solo Not every financial adviser wants to build a lasting franchise. investmentnews.com) The pros and cons of going solo. riabiz.com) State auto-IRA programs seem to drive companies to start their own plans.

Strategic charitable giving not only benefits the recipient but can also create significant tax advantages for the giver. You can deposit money into the account now, receive the tax benefit, and then make the donation in your own time. Theres no time limit on when you need to make the donation.

Tax season can be overwhelming, but understanding how to leverage deductions and credits can significantly impact your bottom line. While both mechanisms help reduce what you owe, they operate in fundamentally different ways that affect your final tax bill. And tax law is not static. of your AGI. of your AGI.

This weeks Tax Advisor Weekly covers key updates for financial professionals. We begin with guidance on navigating property tax considerations during business mergers and expansions. In this blog post, well cover key business events that impact property tax and business licenses, along with what you need to consider for each.

Tax deductions can save you thousands annually by reducing your taxable income through legitimate business expenses. Understanding these deductions is more critical than ever as tax laws evolve, presenting new opportunities for savings. Understanding this distinction is crucial for maximizing your tax benefits effectively.

To achieve this, financial support may start at a very young age, allowing for a longer growth horizon and, in many cases, serving tax and estate planning purposes. Parents often want to ensure their children have the resources to pursue their potential and lead fulfilling lives.

This edition of the Tax Advisor Weekly covers key updates for financial professionals. To round things out, we provide a refresher on the most common tax return mistakes to watch for this season. Citizens, Businesses ( Martha Waggoner , The Tax Adviser) U.S. citizens or businesses, a significant shift in regulatory enforcement.

mrmoneymustache.com) Why you need to account for your Treasury income on your state taxes. fastcompany.com) What to consider when rolling over a 401(k) account to an IRA. (tonyisola.com) Age is just one factor when it comes to your asset allocation. ofdollarsanddata.com) Invest time in your life, not in managing your portfolio.

Tax planning might not top everyone’s list of leisure activities, but in the middle of tax season, theres a hidden opportunity. In this episode, we talk about five strategies you can use during tax season to create opportunities to help you reach your financial goals.

Every year brings changes in tax rules, and 2025 is no exception. Staying informed about these tax updates isn’t just about being prepared for tax seasonit’s about making smart money moves all year long. More Money Protected from Taxes Good news for your walletyou can shield more of your income from taxes in 2025.

April 15 marks the IRS tax return filing deadline for 2025. Although this is the traditional tax filing deadline, given the spate of recent natural disasters (such as the California wildfires and Hurricane Milton), the IRS is granting certain filing and payment extensions beyond this date.

Tax-loss harvesting is a powerful strategy that investors can use to reduce their taxable income. As effective as tax-loss harvesting can be, there are a number of important details that investors need to be aware of in order to implement the strategy successfully while following regulations. How does tax-loss harvesting work?

Donor-advised funds (DAFs) have emerged as powerful tools that deliver this exact combination, providing immediate tax advantages while offering flexibility to recommend grants to qualified organizations over time. At their core, donor-advised funds are specialized 501(c)(3) charitable accounts housed within public charities.

morningstar.com) Americans are increasingly tapping their 401(k) accounts early. investopedia.com) On the tax benefits of 529 accounts. (readthejointaccount.com) Retirement savings Stopping and starting your 401(k) contributions is akin to market timing. sherwood.news) Meet the Roth IRA evangelists. wsj.com)

ft.com) Taxes Your chances of getting audited are low and getting lower. nytimes.com) Just because the IRS is defanged doesn't mean you should skimp on your taxes. thecollegefinanciallady.com) Do you know what's in your 529 account? humbledollar.com) What is the best way to manage a concentrated, low tax basis position?

As the year comes to a close, now is the time to review potential financial moves to help minimize your tax burden heading into 2025. Proactive year-end tax planning can lead to significant savings and set you up for financial success in the new year. Find your next tax advisor at Harness today. Starting at $2,500.

We also get you up to speed on the tax benefits of using a DAF. If you've heard of a DAF and are curious about incorporating it into your giving and tax planning strategy, this article is for you. Key Takeaways: Contributions to a donor-advised fund reduce your tax bill in the year your contribution is made.

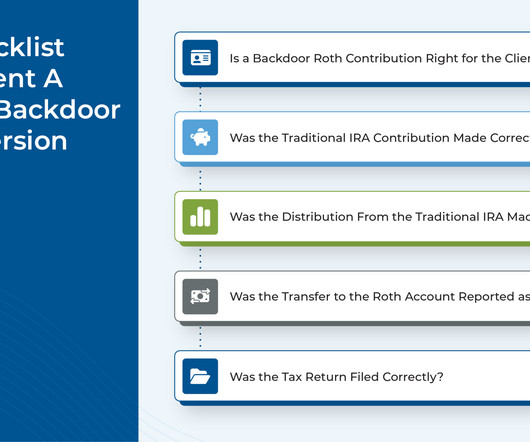

There are many tax planning strategies that allow financial advisors to demonstrate the ongoing value they provide to clients in exchange for the fees they charge. Advisors also can support the backdoor Roth process by communicating with clients' tax preparers about the strategy and why they are recommending it for their mutual client.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content