This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

But wealthaccumulation might be something you haven't thought about. But how do you create wealth? Is wealthaccumulation only for the rich and famous? While some are born into it, many others spent a long time accumulating their wealth. What is wealthaccumulation? Not at all!

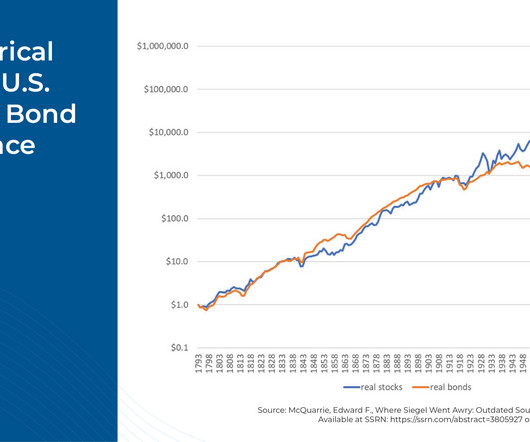

Accordingly, McQuarrie found that, while stocks did indeed far outperform bonds between 1942–1981, not only did stocks and bonds produce about the same wealthaccumulation during the 150-year period before 1942, but the same held true from 1982–2019 as well.

Tom Fridrich, Senior Wealth Planner . Once upon a time, people would put money in their 401(k) or IRA accounts and know that – should their retirement savings outlive them – their loved ones would inherit the rest and all would essentially be well. . How Did the SECURE Act Affect Inherited Retirement Accounts?

When you start to approach retirement, you’ll have to start thinking about transitioning from the wealthaccumulation stage to the income stage of your life. Misusing Retirement Accounts. Retirement accounts are a crucial piece of your retirement puzzle. Taking Too Much Income.

In your working years, you made sure to have a savings and wealthaccumulation plan. Your retirement goals were focused on building wealth, but now, your goal is to spend it efficiently. NO STATEMENTS MADE SHALL CONSTITUTE ANY FINANCIAL, TAX, LEGAL, OR ACCOUNTING ADVICE.

Backdoor strategies are retirement contribution methods that allow individuals to bypass income limits and contribute to tax-advantaged retirement accounts. Along with the opportunity for increased wealthaccumulation, Mega Backdoor strategies offer other benefits.

When you are presented with the option to distribute your assets, you will have the choice to roll them into an IRA or place the stock into a taxable account and then roll the remaining assets into an IRA or 401(k). In addition, shares of employer securities for the NUA must be moved in-kind to a taxable brokerage account.

In a remarkable feat of financial prowess, a 28-year-old individual has shattered traditional notions of wealthaccumulation. Creating multiple streams of income allows you to diversify your earnings, reduce risk, and unlock the potential for wealthaccumulation.

Furthermore, investment planning enables you to capitalize on market opportunities and harness the potential for wealthaccumulation. Strategically selecting tax-efficient investment vehicles, such as retirement accounts, tax-deferred annuities, and municipal bonds, helps reduce the effect of taxes on your investment returns.

They can work with you to create a plan that balances your current financial needs with long-term wealthaccumulation, ensuring you make informed decisions regarding your equity compensation. A financial advisor can assist you in managing all the details that you must account for. Ready to Grow Your Wealth?

Consequently, the middle class may experience slower wealthaccumulation and struggle to keep pace with inflation. This involves employing a range of tools, from tax-advantaged and offshore accounts to setting up complex trusts. These tools help them minimize their overall tax liability and preserve as much wealth as possible.

Accountant 5. Their duties also include managing payroll and working with an accountant or tax preparer to file the company’s tax return. AccountantAccountants balance a business’s books and file tax returns. Nowadays, many of the processes of accounting are done through the cloud and also automation. Paralegal 7.

A note: be sure to keep your emergency fund in an easily accessible account. Don’t put it into a retirement account where you won’t be able to get the money out for years.) A high-yield savings account is a good option for your basic emergency fund. Keep in mind that these accounts are tax-deferred, not tax-free.

Anyone with dependents, retirement accounts, life insurance or real property. A beneficiary is the person or entity who receives the death benefit of an insurance policy, or retirement account proceeds at the death of an insured or account owner. In your 30s and 40s wealthaccumulates. Who needs estate planning?

This article explores different ways in which financial advisors can help you with wealthaccumulation for retirement. How do financial advisors help in retirement income accumulation? Below are some ways in which a financial advisor can help accumulatewealth for retirement: 1.

Articles related to wealth building Leverage the secrets of stealth wealth to improve your financial future! That’s a mistake because it doesn’t account for those around us who have built wealth quietly. What is stealth wealth? Avoid lifestyle inflation More money can appear in your bank account in so many ways.

While we can tell clients that the markets over time have an upward trend, it’s still a challenge to help them remain rational when they are looking at recent account statements and seeing a loss. Roth Conversion If a Roth conversion makes sense for your client’s planning strategy, consider executing it during a market downturn.

Background Since January 1, 2010, all individuals, regardless of income levels, have been able to convert existing retirement accounts such as traditional IRAs into Roth IRAs. Roth and traditional IRAs both provide tax-free growth on invested assets to account owners, but the two options also differ in a variety of ways.

Since January 1, 2010, all individuals, regardless of income levels, have been able to convert existing retirement accounts such as traditional IRAs into Roth IRAs. Roth and traditional IRAs both provide tax-free growth on invested assets to account owners, but the two options also differ in a variety of ways.

Should you have separate bank accounts, or do you want to consider opening a joint bank account ? Investing is a vehicle for building wealth. If you want to build generational wealth , you should be thinking about how you can invest your money so that it can grow. Do they believe that you should combine finances?

Different cultures have varied attitudes toward saving, spending, debt, and wealthaccumulation. About Dash Investments Dash Investments is privately owned by Jonathan Dash and is an independent investment advisory firm, managing private client accounts for individuals and families across America.

This can help optimize your wealthaccumulation while mitigating unnecessary risks. They help you optimize tax planning Tax planning is an important aspect of financial planning that can significantly impact your long-term wealthaccumulation.

As you can see, there are plenty of reasons equity compensation recipients can point to, for remaining overly concentrated in their company account. Somehow, inaction often feels “safer,” even though no decision is a decision after all. Some of the reasons are quite valid, such as a blackout period.

That’s a mistake, though, because it doesn’t account for those around us who have stealth wealth. What is stealth wealth? Read on for the benefits, signs, and secrets of stealth wealth that you can adopt in your own financial life. Stealth wealth can give you just that. Is it something you should aspire to?

One practical approach is to convert traditional retirement accounts, like a 401(k) or a traditional IRA, into a Roth IRA. However, it is important to consider the immediate tax liabilities that come with converting to a Roth account. In addition, you must hold the account for at least five years before making a withdrawal.

Tax Planning: Financial advisors can help manage your tax liability, advising on strategies to minimize capital gains taxes, maximizing tax-efficient investments in retirement accounts, and charitable giving. When selecting a financial advisor, it’s important to take into account more than just their investment performance.

That’s one reason we advocate for maintaining an appropriate mix between wealth-accumulating and wealth-preserving investments. For example: Asset Location : Among your taxable and tax-favored accounts, where will you locate your stocks, bonds, and other assets for tax-efficiently accumulating and spending your wealth? .

Whether you’re aiming for long-term wealthaccumulation or exploring short-term opportunities, the courses guide you through proper financial planning. Best Mutual Fund Courses : Starting the journey of investing in mutual funds as a beginner is a wise step toward financial growth.

Common examples of short-term investments include: High-yield saving accounts Money market funds Peer-to-peer lending High-yield savings accounts If you’re looking for a safe and straightforward way to invest $20k, a high-yield savings account may be the way to go. A high-yield savings account is like a regular one.

The wealthy make strategic investments that help them grow their wealth, mitigate risks and minimize taxes. Rich individuals do not simply hoard their money in bank accounts. These investments serve not only to grow their wealth but also to protect it against market volatility and economic downturns.

Below are 5 steps that can help catch up on retirement savings in your 50s: Step 1: Max out your 401(k) and IRAs If you are 50 and have no retirement savings, one crucial strategy is to maximize contributions to your 401(k) and Individual Retirement Accounts (IRAs). Additionally, IRAs are retirement accounts you can open and fund on your own.

For instance, if your goal is wealthaccumulation, the financial advisor may recommend different strategies versus if your goal is wealth preservation. Your investment returns, distributions from retirement and pension accounts, Social Security benefits, dividend payments, etc., account for your retirement income.

Chloe is a Woman of Color, a group that is vastly underrepresented in wealth management, and she serves tech professionals in their 30s or 40s who often are women, People of Color, or LGBTQ+, many of whom are transitioning in their wealth journey from setting up the initial foundation to the next level. Here’s an example.

The Harness Concierge team gives Kelley the support from a dedicated individual to help facilitate administrative tasks, client and prospect communication, as well as, in Kelley’s words, “hold me accountable for client follow ups.” The goal of the Concierge team is to enable advisors and clients to get more done faster.

Chloe is a Woman of Color, a group which is vastly underrepresented in wealth management, and she serves tech professionals in their 30s or 40s who often are women, People of Color, or LGBTQ+, many of whom are transitioning in their wealth journey from setting up the initial foundation to the next level. Here’s an example.

However not all states collect income tax, so check with your accountant before proceeding with a non-resident state return filing. 1099-INT: Any accounts or investments that produce interest will be required to send out a 1099-INT form. Freelancers and contractors may also receive their 1099 as a 1099-MISC, as opposed to a 1099-NEC.

Open those savings accounts that you’ve included in your plan. Then, automatically transfer money into your accounts so that you don’t have to think about it. Not just wealth that you can enjoy now but generational wealth for your future family. Investing is the vehicle for wealthaccumulation.

Some of the responsibilities of a coach include setting goals with clients, building strategies to achieve the goals, and holding clients accountable. You can put any income you make into savings or invest the money to get started with wealthaccumulation. Blogger Blogging isn’t something that will make you money right away.

How do we achieve goals for family capital, considering pending changes in the estate tax laws and, for families with geographically dispersed members, taking into account cross-border legal and tax considerations? Should we modify existing plans considering changing market conditions?

In particular, we want each client’s operating account to be large enough to provide for spending needs and emotional peace, so that they can comfortably maintain their long-term investments without feeling the need to disrupt them. Prepare for the unexpected.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content