This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

By Jake Anderson, CFP ® , Wealth Planner When helping clients begin retirementplanning, the same questions often arise: What should my retirementplan look like? Your lifestyle, goals, family situation, and risk tolerance will give a unique signature to your retirementplan. How much should I be saving?

Also in industry news this week: While an infusion of Private Equity (PE) capital has shaken up the RIA M&A market, the ultimate implications for advisors, their clients, and the PE firms themselves remain unclear A recent study has found that a significant portion of 'DIY' investors are open to working with a human advisor (and paying for the (..)

Because of these differences, stocks and bonds accomplish different things in an assetallocation. Note: Since most investors are more familiar with stocks, a comparison of risk and return within the equity market has been intentionally omitted from this article). With bonds, you’re buying the issuer’s debt.

Quoted in a Wall Street Journal article before the 2016 game, respected Wall Street analyst Robert Stoval said, “There is no intellectual backing for this sort of thing, except that it works.”. Perhaps it’s time to rebalance and to rethink your ongoing assetallocation. Some notable misses for the indicator include: St.

Living off dividends in retirement: hypothetical income today for portfolios between $2M and $15M Investors may wonder how much money they could expect in dividend income annually given today’s market. In another words, if your assetallocation is 60% stocks and 40% bonds, the current weighted average yield is 2.19%.

If youre searching for a fiduciary financial planner, flat-fee financial planning, or the best alternative to AUM-based advisors, this article will help you decide which model is right for you. Unlike AUM advisors, they dont have an incentive to keep assets under management, so their recommendations are truly objective.

But volatile markets aren’t necessarily a negative thing, especially when it comes to retirementplanning. When you are planning for retirement, a lost decade can mean stagnated savings and loss of buying power to inflation. Target Date Funds Can Help AssetAllocation. LPL Tracking #1-05275467.

As you would expect from an outstanding organization like Microsoft, it offers a very robust 401(k) to help employees save for retirement. This article will discuss the key features of the Microsoft 401(k) plan, and after reading it, you should leave with a clear game plan of how to: Maximize the match (free money! )

Barron's had an interesting article about a BofA study showing that over a period of many decades an assetallocation of 60% equities/40% commodities outperformed an allocation of 60% equities/40% fixed income by 0.80% per year. I haven't looked in awhile I guess but yowza, a lot of option-centric funds.

I found their assetallocation and wanted to see from the top down if there's a way to mimic them to some extent and get decent results. Yahoo Finance had a cleverly titled article; Generation X is gloomy, but their retirement reality may not bite. A few different things today. Here's how I built the portfolio.

just upended retirementplanning…again. The age when retirees must begin drawing from non-Roth retirement accounts increases to 73 in 2023, then 75 in 2033. Raising the age when withdrawals must begin is great as it gives investors more planning opportunities. The Secure Act 2.0

The starting point today is the that Rational ReSolve Adaptive AssetAllocation Fund (RDMIX) has gone through a strategy change, renaming as the ReturnStacked Balanced Allocation & Systematic Macro Fund and keeping the same symbol. " balanced allocation and $1 of exposure to a systematic macro strategy."

The idea that fund company determines the assetallocation, referred to in this context as a glide path, makes no sense to me and then factor in that fund companies uses different glide paths. The refrain from the article is to stay the course which is not surprising even if a little disappointing. That can be true.

The title of today's post is essentially the question asked in a Bloomberg Article ( syndicated at Yahoo ). How many articles have you read about bonds being a good ballast for equity volatility? The TLDR is that broad diversification has lagged behind simple market cap weighting for the last 15 years. The love the word ballast.

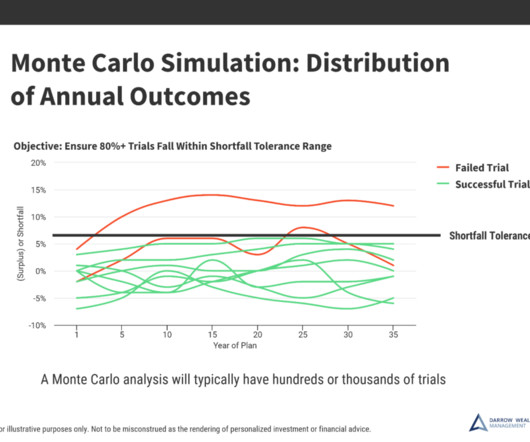

Don’t stress out about every headline, stress test your retirementplan instead.Markets move every day and the news cycle is 24-7. Even if actual average returns meet targets over time, market volatility can still derail your portfolio and retirementplans. This produces a probability of success across all trials.

GAA stands for Global AssetAllocation and it has been lagging for 15 years. Barron's had an article about alternatives sought by the "super rich. Included in the article were aging whiskey which I don't what that is, like maybe something to do with leasing the barrels? Here's a great chart to illustrate the point.

Barron's has an article this weekend titled 3 Things To Do To Manage A Bear Market Early In Retirement. As I read the article I thought about the above referenced scene where Michael Corleone counters Senator Geary. The 2 or 3 diversifiers would likely go up and you'd avoid selling other assets low. of now anyway.

This article will explore how often to rebalance your 401(k). Rebalancing a 401(k) refers to adjusting the assetallocation of your investment portfolio back to its original target percentages. As a result, your portfolio’s allocation changes from its original, and it now consists of 60% stocks, 25% bonds, and 15% cash.

There has been discussion in the last couple of days in articles and Tweets trying to look at some of the drawbacks with bond funds beyond the obvious and what might be described as an exploration about what to use instead of bonds, like the types of alternatives we've been looking at for a long time here.

Morningstar had an article titled 3 Ways To Simplify Your Portfolio and while some of the points made sense, others missed the target somewhat. Owning two actively managed mutual funds may or may not be ideal but that's not the point, the point of the article is simplification. This isn't automatically an act of simplification.

Consider consulting with a professional financial advisor who can help you understand and employ suitable retirement investment strategies based on your income, age, and retirement expectations. This article explores different ways in which financial advisors can help you with wealth accumulation for retirement.

Risk Tolerance: What is your assetallocation? If you are close to retirement, and you have too much exposure to equities, a retrenchment in the stock market could delay your retirementplans by years. This concept highlights the importance of rebalancing your portfolio as you get closer to retirement.

You can also get information on your performance and assetallocation. This will help you to create an assetallocation that will get you where you need to go with your investments. It can be used to help you with your assetallocation, at least based on the investment options that your plan includes.

In an ideal world, every retiree would time their retirement to coincide with a bull market, but even during a severe downturn retirees can make their money last, contends an article in The Wall Street Journal. The first five years of retirement are crucial for figuring out a lifestyle that can sustain you for years to come.

Barron's had a fun article that looked at some ideas from William Bernstein titled The Trick To A Bullet Proof Portfolio? I'm a sucker for this sort of article. That is not guessing what markets will do, that is just managing assetallocation and cash needs. Invest For The Very Worst Of The Worst.

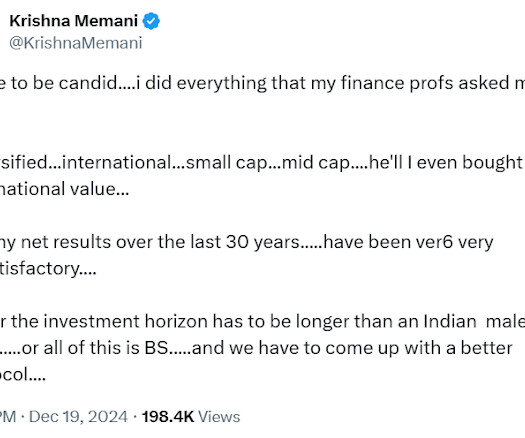

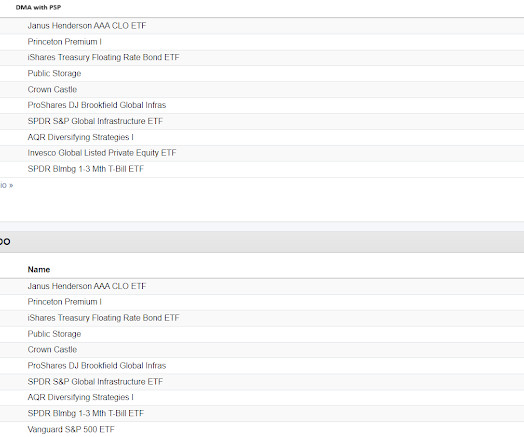

Here's the latest about Harvard from Bloomberg that included this chart of the assetallocation. It's not that someone could not copy the asset class exposure, just that the return streams would not look the same and often, various forms of sophistication replication does not really work in fund form. Black is 2023.

First up, the Harvard Endowment which posted the following assetallocation. Here's an article at theStreet.com from 2007 where I bagged on PSP. Arguably neither one is very close in terms of how it replicates but borrowing the assetallocation from the top down yields what I would call a valid result. I used PSP.

In this article, we guide you through the list of top personal finance courses designed for beginner to intermediate-level learners. The topics covered are personal finance & investment planning, risk, return & assetallocation, equity markets, analysis, investing, mutual funds and strategies for wealth creation.

The answer lies in smart and strategic retirementplanning. Gone are the days when retiring at 60 was a one-size-fits-all goal. It’s time to rethink when to start stashing away those savings and how to modify your plan in a world that’s constantly changing. So, how do we tackle this?

Here's an article taking the other side that would be worth reading. Client and personal holding Standpoint Multi Asset (BLNDX/REMIX) is an exception that proves the rule but it only blends two things together; equities and managed futures. Strategies can cancel each other out which might be going on with FIG. What's going on?

Consult with a professional financial advisor who can help create a balanced strategy toward retirementplanning and portfolio reviewing, ensuring both financial stability and peace of mind on your journey toward retirement. You can use this time to adjust your assetallocation to prioritize capital preservation.

This really is about having the right assetallocation. A balance needs to be struck between enough growth potential for a 50 or 60 year retirement and enough cash to get through the next 30 month bear market, Bear markets tend to run 18-30 months and while 2022 was shorter than that, a longer one will happen eventually.

From retirementplanning to market volatility, equity compensation, family expenses, and major life transitions, it’s easy to feel overwhelmed with financial responsibilities. An advisor can answer questions like: When can I fully retire? Here are 5 signs it might be time to hire a financial advisor.

That is the title of an article at Yahoo where they look at savings benchmarks for 30, 40, 50 and I am guessing one will get published for 60. This topic can be useful and my hunch is that Yahoo has run pretty much the same series several times before but either way there's utility here and hopefully I can add a little nuance to it.

Allison Schrager wrote an article for Bloomberg last week that Wall Just Doesn't Get It On Retirement. The relevance ties into assetallocation. I shared on Facebook noting that Schrager suggested better and cheaper annuity products and that given how undersaved we collectively are, it may come to more annuity products.

Speaking of simplicity, there's this from CalPERS; It seems like these guys are moving their goal posts in terms of assetallocation every couple of years, they're going heavier into private equity and VC then they're dialing it back, now increasing again. Here's a great read about retirement. The second point fascinates me.

Over the years, we've made some fun of CalPERS for seeming to change their assetallocation strategy every couple of years such that they end up chasing heat, that is chasing the thing that worked last year. It started with this article from The Athletic. Apparently, he was a great teammate.

This article will help you understand the benefits of working with a financial advisor to secure your financial future. Below are five benefits of working with a financial advisor and how they can help you retire with more wealth: 1. For example, imagine a scenario where you have several decades until retirement.

That reality can change some of the calculus between endowments and individual investor accounts but there are things we can learn from their assetallocations all the same. The article blames behavioral factors for the huge allocations to alts including vanity. Back to QLEIX which again struggled in 2020.

If the sell off was "exacerbated" by 0dte's as mentioned in the Bloomberg article, ok but down 1.5% They build out a few different types with various allocation percentages for each type. I was curious of course so I looked at the 60/40 blend under Strategic AssetAllocation. world is a good first impression.

He wrote several articles about it for IndexUniverse which was the precursor to ETF.com but unfortunately, John's content is no longer up on the site anywhere. I did a search for Serrapere's articles because in at least one of them he went into detail about what he used to build the portfolio.

Table of contents 11 Tips on how to save for retirement in your 40s and 50s Expert tip: Leverage catch up contributions and celebrate your wins as you save How much to save when saving for retirement at 40+ Catch-up contribution details Is it too late to start saving for retirement at 40?

I'm not too interested in the story but toward the end of the article there was a breakdown of the assetallocation as of the end of Q1 and I am fascinated. The allocation at the end of Q1 was 57% crypto, 21% in multi-strategy (presumably hedge funds), 7% in equities and 15% in structured credit.

Yesterday we wrote about whether it makes sense to go heavier into liquid alts with an article from Morningstar as the catalyst. I want to start with the comments on the article. That, combined with an adequate savings rate, suitable assetallocation and the wherewithal to avoid panic will probably get the job done.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content