This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Which could prove to be a boon for the financial advice industry as more consumers are willing to entrust their assets to an advisor (while at the same time possibly making it tougher for some advisors to differentiate themselves primarily by how they put their clients' interests first?).

Also in industry news this week: According to a recent survey, 40% of financial advisory clients would switch to an advisor who offers estateplanning services, with help with specific tasks like beneficiary designations or tax strategies as the most sought-after service among respondents RIA M&A activity set a first-quarter record to start the (..)

million in assets to both retire and pass on a legacy interest (though many have yet to establish an estateplan), according to a recent survey. Enjoy the current installment of "Weekend Reading For Financial Planners" – this week's edition kicks off with the news that affluent Americans believe they need an average of $5.5

Also in industry news this week: Top Democratic Senators are urging the Treasury Department to crack down on a range of estateplanning strategies for high-net-worth individuals, including GRATs and IDGTs Amid fallout from recent bank failures, both Republicans and Democrats are considering whether current FDIC insurance limits should be increased (..)

Tax deductions can save you thousands annually by reducing your taxable income through legitimate business expenses. Understanding these deductions is more critical than ever as tax laws evolve, presenting new opportunities for savings. Understanding this distinction is crucial for maximizing your tax benefits effectively.

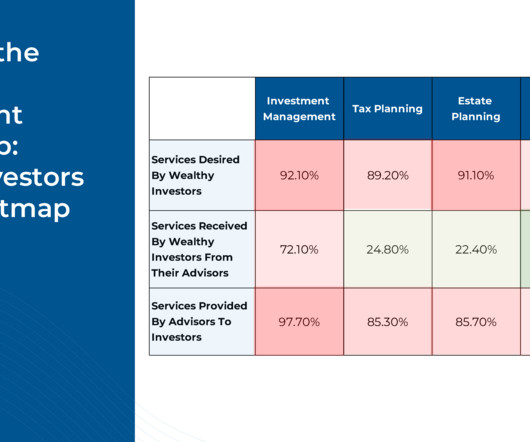

In this 'hybrid' video-based article, Michael Kitces and John Bowen, CEO and founder of CEG Worldwide and CEG Insights (formerly Spectrem Group), dive into CEG's extensive data on the "gap" between the services that financial advisors actually offer to their clients and what HNW clients truly want from their advisors.

As the year comes to a close, now is the time to review potential financial moves to help minimize your tax burden heading into 2025. Proactive year-end taxplanning can lead to significant savings and set you up for financial success in the new year. Find your next tax advisor at Harness today. Starting at $2,500.

Also in industry news this week: Backers announced the new Texas Stock Exchange, which seeks to provide companies with a lower-cost alternative to the NYSE and Nasdaq, which, if successful, could create a more competitive landscape and potentially better execution and reduced trading costs for financial advisors and their clients The American College (..)

As is traditional, the 2025 IRS tax filing deadline is April 15th. In this guide, well explore the 2025 tax extension process, the reasons for requesting an extension, and how a tax advisor from Harness can help you. Table of Contents What is a tax extension? Why do I need a tax extension? This is not the case.

Yet despite this – and perhaps even because of it – advisory firms are putting an ever-greater focus on financial planning in 2022, as a way to both show value to clients in the midst of difficult market returns, and, more broadly, to help clients navigate the current environment.

The 2017 Tax Cuts and Jobs Act (TCJA) brought sweeping changes to the tax code, impacting every taxpayer and business owner. Here’s a summary of the major tax law changes coming in 2026 and some steps individuals and business owners can take to prepare. For some, this may lead to more taxes paid on capital gains.

Charitable Contributions: Donating appreciated stock to charity while reducing capital gains tax. A complete discussion of the pros and cons and workings of swap funds is outside the scope of this article, but there are many things to consider before investing. Gifting: Transferring stock to family members or trusts.

While a Roth conversion may never make sense for some individuals, for others, early retirement years may be the best time to convert pre-tax accounts to tax-free Roth. Your current and projected future tax rate is often a main component of the decision, but there are other considerations and benefits as well. 4 key benefits.

Roth IRA conversions present a significant challenge for retirement planners: pay taxes now or later? Moving funds from traditional IRAs to Roth accounts triggers immediate taxation but promises tax-free withdrawals in retirement.

If youre searching for a fiduciary financial planner, flat-fee financial planning, or the best alternative to AUM-based advisors, this article will help you decide which model is right for you. Comprehensive Financial Planning is Included Many AUM advisors charge extra for estateplanning, tax strategies, and retirement planning.

While a financial plan focuses on managing your finances during your lifetime, an estateplan is essential for determining the fate of your assets after you pass away. Estateplanning involves the transfer of your assets to your heirs in the event of your passing.

A deep discussion of these strategies is outside the scope of this overview, and because every situation is so different, be sure to discuss your situation with your tax and financial advisor. Taxes should always be a component of any investment decision — but not the main driver.

Working together, these professionals can conduct a "stress test" of the client's current situation to proactively identify potential areas of weakness in the client's financial, tax, and estateplanning. For instance, many business owners have loosely defined succession plans (or none at all!),

A strategy for managing your investments is also key: understanding your risk capacity vs appetite, balancing a need for a current income stream and future growth, and ways to be more tax efficient in taxable accounts. Put the plan into action. The tax consequences from the sale can be highly complex.

This article goes over several benefits of hiring a financial advisor after you retire to help you decide if you need a financial advisor after retirement. A financial advisor can craft tax-efficient withdrawal strategies to minimize the tax burden on your retirement income. Taxplanning is not solely about federal taxes.

But that doesn’t mean the actual assets are just split down the middle, and some assets are much more favorable from a tax perspective than others. Once the divorce is finalized, a crucial (but often overlooked) part of the process is updating estate documents and beneficiary designations. Cash assets have no tax implications.

The Symposium is an event for professionals dedicated to philanthropy, estateplanning, and charitable giving. Shell explore how a comprehensive financial plan can serve as a roadmap for giving, helping clients make thoughtful decisions that support both personal and philanthropic priorities. The event is held from 8:00 a.m.

Here is a great way to value those items if you are eligible to take a tax deduction. Property donations will need acknowledgment of receipt from the charity and items totaling over $500 will need a special form (IRS Form 8283) when filing your taxes. Here is an additional Mainstreet article that dives a little deeper into this topic.

That’s why this article will provide valuable tips and insights to help retirees build a legacy for their families and future generations. The Foundations of Financial Planning Proper financial planning is widely considered the first step to building generational wealth. [1]

The 2017 Tax Cuts and Jobs Act (TCJA) brought sweeping changes to the tax code, impacting every taxpayer and business owner. Here’s a summary of the major tax law changes coming in 2026 and some steps individuals and business owners can take to prepare. For some, this may lead to more taxes paid on capital gains.

Key Takeaways: Too many tax practices are bogged down in commoditized administrative tasks and compliance work, making it challenging to cross-sell services to expand client relationships. Take an inventory of how your practice spends time Reflect on how your own tax practice spends the bulk of its time.

In this guide, we explore the four main types of tax professionals and the benefits of working with a tax advisor to help navigate challenging tax scenarios. We’ll dive into what a tax advisor does, and help you make an informed decision about which type of tax professional is right for you.

Depending on the nature of the windfall, planning opportunities and considerations will vary. For example, the tax laws and distribution terms for an inheritance is quite different to the tax and liquidity considerations during an IPO. In their situation, it meant they could sell all their shares tax free.

Your business advisory team may consist of: a business broker or M&A advisor, accounting and tax advisors, and transaction/M&A attorney. On the personal side, your financial advisor , estateplanning attorney, and CPA/tax advisor should be involved throughout the process.

10 steps to manage a financial windfall Expert tip: Keep living your life normally Factoring in taxes How do you deal with sudden financial windfall? Articles related to being wise with money Manage your large sum of money smartly! Tax refunds that are more than you expected. What should you do with a $1,000 windfall?

For the purpose of this article, we will refer to all of these as Supported RIAs. As clients are demanding more from advisors, many firms have added subject matter expertise in the areas of advanced financial planning, tax advisory, estateplanning, tax preparation, and even life coaching.

As a company founder, early startup employee, or small business owner, you may find yourself in a higher tax bracket as your business grows or you realize gains from equity compensation. But that doesn’t mean you simply have to accept a higher tax bill. Here are 20 tax-efficient actions to consider when filing your taxes in 2024.

Tax advisors, and other tax professionals , offer services from preparing and filing annual tax returns to comprehensive tax strategies that help minimize taxes and preserve wealth over time. In this guide, we’ll explore the average fees of tax advisors in the US for 2024.

Retirement Planning, Income Taxes. I had the opportunity to share my thoughts on SEP IRAs with Rachel Hartman of US News & World Reports for her fine article titled, “What is a SEP IRA?” Since we have some deadlines coming up, I thought I’d promote her article again here in my blog. What is a SEP IRA?

Create or revise your estateplan 9. Plan for emergency expenses 11. Articles related to expanding your family Leverage these tips to save for a baby! As a mom to twins, I can tell you first-hand that babies are an incredible blessing, but if you are able to, you definitely want to plan your finances out ahead of time.

How are UTMAs/UGMAs taxed? This account is owned by the child, so earnings are generally taxed at the child’s assumed lower tax rate instead of the parent’s rate. Note: This is not tax-advantaged like a 529 plan. This is the power of this type of account. What is the impact on Financial Aid?

In this article, I’ll take you through everything you need to know in order to plan for your financial future. Keep reading, then get ready to take some action to kick-start your own solid money plan. So what is a financial plan in simple terms? Plan for taxes. Yup, taxes! Create an estateplan.

Create a list of things to plan for How to make a financial plan Expert tip: Consider your needs for each life stage Determine the type of financial plan you need Tips on how to frequently review your financial plan What is a financial plan using an example? Is a financial plan the same as a budget?

In addition to this, you can save more and plan for more significant purchases with greater ease. The tax liabilities for married couples filing their taxes jointly will differ from single individuals and those filing individually. Married couples can file their taxes jointly under the filing status of married filing jointly.

Key Takeaways: Accounting advisory services extend beyond traditional tax preparation to offer strategic financial guidance. Specialized areas can include estateplanning and tax-efficient investment strategies. Table of Contents What Are Accounting Advisory Services?

A financial advisor can help you identify common retirement planning blind spots. This article will also uncover some of the key blind spots you need to be aware of in your retirement planning journey. As a couple aged 65 in 2023, you may need approximately $315,000 saved (after tax) to cover your healthcare expenses.

When planning for retirement, one of the most important decisions you will likely make is which type of retirement account to use. The Roth Individual Retirement Account (IRA) and the pre-tax retirement account are two common options. A Roth IRA is a tax-advantaged retirement savings account funded with your after-tax dollars.

And ultimately, how to invest a windfall will depend on a number of factors, including your risk tolerance, time horizon, and spending plans. And that’s before even considering taxes or market volatility! Depending on your goals and personal financial situation, there may be many more planning opportunities to consider.

And ultimately, how to invest a windfall will depend on a number of factors, including your risk tolerance, time horizon, and spending plans. And that’s before even considering taxes or market volatility! Depending on your goals and personal financial situation, there may be many more planning opportunities to consider.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content