This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

million in assets to both retire and pass on a legacy interest (though many have yet to establish an estate plan), according to a recent survey. Enjoy the current installment of "Weekend Reading For Financial Planners" – this week's edition kicks off with the news that affluent Americans believe they need an average of $5.5

The Wall Street Journal had an article about the fear common to retirees about outliving their money. The title of the WSJ article addresses outliving your money but doesn't spend very much time on a big part of the reason why this a concern which is needing needing to pay for some sort of very expensive assisted living or home health care.

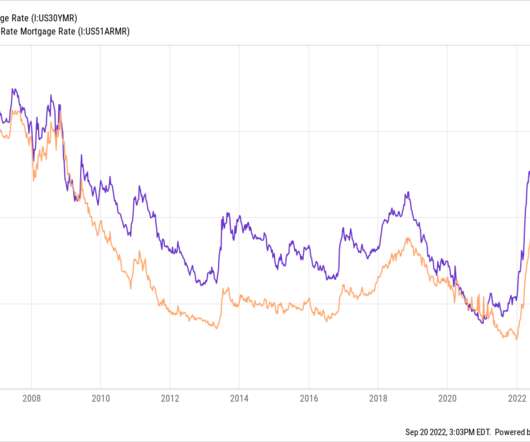

Is retiring with a mortgage a good idea? Retiring with a mortgage doesn’t typically pose a financial risk, and at times it’s the best financial decision. But paying off a mortgage before retirement has upsides also. Here’s when it may – and may not – make sense to pay off a mortgage before retiring.

It has further been estimated that as we approach retirement, this ratio increases to a factor of five times more pain for a loss as opposed to the joy we experience for a gain. There’s no shame in admitting that factor – for a lot of us, math can be very tough. For example, it’s natural to feel the pain of losses.

Yahoo Finance had kind of a long read recapping an update from Morningstar about safe retirement withdrawal rates. There are some interesting comments on the article though as is often the case. I would much rather withdraw 10% or more per year from my retirement accounts and do it without taking any principal.

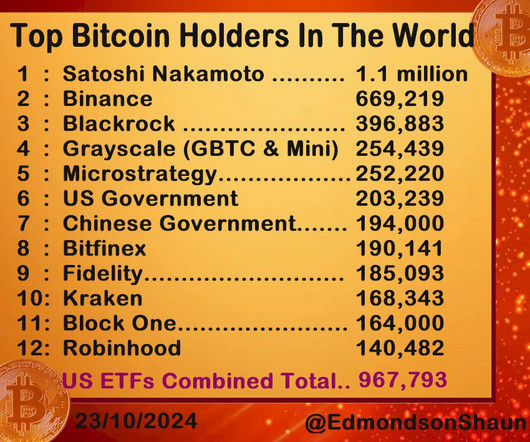

That number is from a Bankrate article I found on a Google search. First, is the math right based on my numbers? That roughly two million Bitcoin is actually more than 10% because approximately 3.8 million Bitcoin are lost forever due to lost hardware or passwords. How much Bitcoin, if any, do you own.

The title of today's post is essentially the question asked in a Bloomberg Article ( syndicated at Yahoo ). We've talked just a couple of times about the market becoming increasingly concentrated which just in terms of math means that a diversified strategy will lag for as long as the big names do well. The love the word ballast.

In the case of real estate a 2.29% weighting and for "private equity" companies it's about 17 basis points (looked at XLF holdings and then did a little math), that's just not going to move the needle. You may agree with Jack about not needing those things, that's valid, my point is that owning an index fund isn't a proxy for them.

The latest retirement disaster article from Yahoo focuses on 55 year olds who have a "median savings of less than $50,000." Yahoo says it's "bleak" because this cohort is "only about a decade from retiring." A harsh reality is that $50,000 is not a retirement fund but it is a pretty robust emergency fund.

Jonathan Clements : Yeah, when I was at Forbes after this initial spell as a fact checker, I was given the mutual funds beat and the core article as the mutual funds reporter for Forbes Magazine. I realized I had enough to retire if I wanted to. But learning how to spend in retirement. And it was very formulaic.

The value of the S&P 500 index of stocks, where most of us hopefully have a good chunk of our retirement savings stashed into index funds, is up about fifty seven percent in just the past two years. Does this make it more vulnerable to a huge crash in the future, and will it affect my retirement? Its just basic math.

There was an article on LinkedIn (via Abnormal Returns) by Victor Haghani that dug into the math working against leveraged ETFs. Eric Balchunas from Bloomberg was baffled because the 1x version only has $60 million in AUM and trades about $1 million per day.

Jason Zweig wrote an article titled How Not to Invest in the Bond Market. The article devoted a good amount of space to bond market math, focusing on the pain of owning the iShares 20+ Year Treasury ETF (TLT) and bond funds in general. The title of course piqued my interest. This quote from Jason surprised me.

This is very important for retirement, and knowing what your target net worth by age should be will help you better understand how to reach your personal financial goals. If you are curious about how much savings you should have by what age , you'll find references to this throughout the article. Your liabilities are your debts.

The term personal finance ratios might give you flashbacks to math class, learning various formulas, equations, and ratios. Articles related to organized finances and financial literacy Calculate your personal finance ratios! Retirement ratio 25x your annual expenses Ever find yourself asking, “ Can I retire yet?

I am less interested int he fund than this excerpt from the beginning of the article. The simple 40 year trade for bonds of "number go up" is finished and as a matter of math, can't be repeated. Barron's had a quick profile on the Blackrock Flexible Income Fund (BINC) which is an active ETF managed by Rick Reider.

More articles related to budgeting Save more money with the 60/30/10 budget! With this system, you will use 60% of your take-home pay to build your savings or even an early retirement account , invest, save up for a down payment, or repay debt. Another example is anyone interested in achieving FIRE; Financial Independence Retire Early.

The Wall Street Journal had an article about the standard 60/40 portfolio , that is 60% allocated to stocks and 40% allocated to fixed income. My experience is that the typical retired person/couple expects growth in exchange for some volatility from the equity portion of their portfolio, they don't want it from their fixed income sleeve.

Bloomberg had an article titled As Gen-X Nears Retirement, Many Fear They Can't Afford It-Now or Ever. The article profiled a half dozen Gen-Xers ranging from 45-60. You're gonna want to retire some day and your 401k is how do it. Generally they all plan to work to 70 or beyond out of necessity. Probably not. Probably so.

Barron's had a fun article that looked at some ideas from William Bernstein titled The Trick To A Bullet Proof Portfolio? I'm a sucker for this sort of article. That is difficult to pull off but if you do the math on that it shows long term outperformance. Invest For The Very Worst Of The Worst.

This post looks at several interesting articles in the current Barron's. Normal 0 false false false EN-US X-NONE X-NONE A quick hit article on HSAs which have evolved to be more of a mainstream type of health insurance offered now as a benefit to employees. Here is an interesting quote from the first Barron’s article.

Articles related to budgeting methods Give the 70-20-10 budget a try! Once you know your weekly or monthly income, you can do the simple math of calculating how much 70% would be. We all need an emergency fund, and to save more long-term (think: retirement). Time is one of the most powerful tools in retirement savings.

In this article, we guide you through the list of top personal finance courses designed for beginner to intermediate-level learners. By enrolling in this course you will learn to manage your finances more effectively by mastering budgeting and portfolio creating for a healthy retirement corpus. You can enroll in the course here.

A quick excerpt from a post a couple of weeks ago about retirement misconceptions. A commenter on a Yahoo article in italics and my reply if he'd have asked me in regular font. I would much rather withdraw 10% or more per year from my retirement accounts and do it without taking any principal.

Barron's dusted off the retirement bucket playbook in an article while also arguing that a 5% withdrawal rate in retirement can now be considered safe versus the more common 4%. The way the math works out, 4% has a success rate in the low 90's based on simulations and has never failed looking backward.

Articles related to the 50-30-20 budget Leverage the 50-30-20 budget today! And don’t worry if math isn’t your thing because we’ve included 50 30 20 budget spreadsheet ideas to help you stay on top of your budgeting strategies. Beyond that, focus on your retirement savings. Is the 50-30-20 budget gross or net?

Today's post will look at a couple of different retirementarticles that I stumbled into this weekend. The Economist posted an opinion piece titled Why You Should Never Retire that I found via a Thread from Unusual Whales. I don't think that everyone loses purpose by retiring or otherwise moving on to a new chapter.

Social Security Retirement Planning . I had the opportunity to share my thoughts on Social Security with Tracey Longo at Financial Advisor Magazine for her article Advisors Concerned As Covid Speeds Projected Social Security Shortfall. You really do get the extra 8% per year after you’ve reached your full retirement age.

They spend hours writing articles and finally hit that “Submit” button… only to not get anywhere near the number of leads that they thought they would. Other times, it’s because those articles were created without a real SEO strategy behind them. If, of course, they were even able to generate leads at all.

A couple of different articles that I think can weave together for a blog post. This article obviously favors more stocks but an interesting thing not said was at what number would it make sense to just flip from individual holdings to mutual funds and ETFs. The first one was in Barron's, it was a quick read studying diversification.

Calculation Breakdown Let’s break down the math to find out how much you could earn annually with a $30 hourly wage: Consider an average workweek of 40 hours and an average year consisting of 52 weeks. Let’s do math again! Retirement/Savings $832.00 . $30 an Hour Is How Much a Year? Utilities $300.00 Groceries $300.00

And in our research for this article, we were happy to learn that we are trending in the right direction. In this regard, financial planning seems to differ from science, technology, engineering and math (STEM) careers where many women leave their jobs in their mid-thirties after a few years of experience on the job.”

There was a lot of content from various places over the weekend about whether it is time to go back into bonds, what retired investors should do for yield and even whether retirees are better off going 100% into equities. As a matter of math, it cannot repeat the run from 8.5% Barron's also noted that 60/40 was up 9.6% in November.

We've got you covered in this article. Retirement accounts. Figuring out how to calculate liquid net worth is as simple as doing a quick math equation: Liquid assets - liabilities = liquid net worth. Don't worry—there is an answer to the question, "What is my liquid net worth" that doesn't involve solving math equations.

Articles related to leaving a job Leverage these tips for leaving a job the right way! Make sure you have done the math. Or perhaps you want to work fewer hours to spend time with your family, or maybe your retirement savings is well-funded , and you find that a part-time job would be a better choice.

The math for this adds up over years of work and can cost quite a bit of income. Needless to say, the ability of black women to achieve financial goals like homeownership and retirement is extremely difficult. The gender wage gap is much wider than average for people of color. The student debt crisis is part of that.

So I took it upon myself to go off and took a course in bond math, took another course in derivatives and realized the underlying fundamental concepts were barely, I mean, it wasn’t even high school math in most cases. I didn’t know what any of these terms meant. SALISBURY: Sure. SALISBURY: Yes. SALISBURY: Yes.

You may only earn about $50 per article when you start, but you can increase that to $200, $300, and more as you gain experience, depending on the subject. If you’re interested in freelance writing, check out Holly Johnson’s article on this site, How to Become a Freelance Writer (from 0 to $30,000+ per month).

Let’s look at one tried-and-true way of multiplying your assets: retirement accounts. How to turn 10K into 100K through investing in retirement accounts. Although it may not sound glamorous, retirement accounts are a solid means of increasing your money. IRAs or Roth IRAs. without penalties. Similar to the 401(k) is a 403(b).

So it may be surprising to hear that a Roth IRA—a vehicle ostensibly intended for retirement income—can be a powerful mechanism for next-generation wealth transfer. Background Since January 1, 2010, all individuals, regardless of income levels, have been able to convert existing retirement accounts such as traditional IRAs into Roth IRAs.

So it may be surprising to hear that a Roth IRA—a vehicle ostensibly intended for retirement income—can be a powerful mechanism for next-generation wealth transfer. Since January 1, 2010, all individuals, regardless of income levels, have been able to convert existing retirement accounts such as traditional IRAs into Roth IRAs.

One, one is true and I’ve always said is that I wanted people to stop, ask if I could doing math. And no one asked me if I can do math anymore with a degree from Booth, particularly in econometrics and statistics. So people really ask you, you take French and can you do math. So I applied to Maryland State retirement.

I’m good at math and science and you know, I always had an idea what go into business, but I felt that electrical engineering would be a good foundation. You know, I, it always, I I see different numbers all the time, so it’s always kinda like, who’s math if you will? 00:02:16 [Speaker Changed] Me too. Interesting.

Somebody had to write each and every one of those articles and posts. You can easily make $1,000 or more each month writing just a few articles. I write online content for a living, earning an average of $20,000 to $30,000 per month writing articles, book chapters, and slideshows for a variety of websites and individuals.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content