This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Each week in Weekend Reading For Financial Planners, we seek to bring you synopses and commentaries on 12 articles covering news for financial advisors including topics covering technical planning, practice management, advisor marketing, career development, and more.

Also in industry news this week: According to a recent survey, advisors are putting an increasing share of client assets into model portfolios, allowing for customization and time savings that advisors appear to be using to provide more comprehensive planning services RIA M&A deal volume saw an annual record in 2024 as a lower cost of capital, (..)

Also in industry news this week: NASAA has proposed an amendment to its broker-dealer conduct model rule that would restrict the use of the terms “advisor” and “adviser” for broker-dealers and their registered representatives who are not also investment advisers or investment adviser representatives A recent study suggests that (..)

Each week in Weekend Reading For Financial Planners, we seek to bring you synopses and commentaries on 12 articles covering news for financial advisors including topics covering technical planning, practice management, advisor marketing, career development, and more.

As the year comes to a close, now is the time to review potential financial moves to help minimize your tax burden heading into 2025. Proactive year-end taxplanning can lead to significant savings and set you up for financial success in the new year. GET STARTED 1. For those over 50, the limit is $8,000.

Enjoy the current installment of "Weekend Reading For Financial Planners" – this week's edition kicks off with the news that a recent survey indicates that clients of financial advisors are more confident than others about their financial preparedness for retirement and are more likely to have a financial plan in place that can weather the ups (..)

Also in industry news this week: A survey indicates that while financial advisors remain the most trusted source of financial advice, they might increasingly encounter client questions and ideas that originated from social media Following the transition of advisors and clients from TD Ameritrade and amid competition from competing RIA custodians, Charles (..)

While this will help seniors keep pace with rising prices, it also creates taxplanning opportunities for advisors and raises the possibility that the Social Security Trust Fund could be depleted sooner than expected. How advisors can use the principles of ‘self-centered’ shopping to build a loyal client base.

A potential compromise during the lame-duck Congressional session could see a boost to the child tax credit and extended tax breaks for businesses. From there, we have several articles on taxplanning: How advisors can add value for their clients by managing their exposure to mutual fund capital gains distributions.

million in assets to both retire and pass on a legacy interest (though many have yet to establish an estate plan), according to a recent survey. Enjoy the current installment of "Weekend Reading For Financial Planners" – this week's edition kicks off with the news that affluent Americans believe they need an average of $5.5

House of Representatives and is now being considered in the Senate would increase the number of firms classified as “small entities” and would require the SEC to assess the impact of proposed regulation on this newly enlarged class of investment advisers (which tend to have fewer compliance staff and resources available compared to larger (..)

Which suggests that while firms might be tempted to zero in on compensation when it comes to retaining advisors, focusing on these other factors (which do not necessarily involve hard dollar expenses) could pay off in the form of increased advisor (and client) retention over time.

Although any investor with earned income can make a non-deductible contribution to an IRA (up to $7,000 in 2024-2025 if under age 50) and still take advantage of tax-deferred growth, it still may not be advisable. Many people end up paying taxes twice. In 2024 and 2025, the highest marginal tax rate is 37%. Yes and no.

Retirement is different for folks who are running a small business. Your retirement is something that isn’t set up by an employer, and you often must manage it on your own. If you are running your own business and are interested in setting yourself up for retirement, contacting a financial advisor can be a great idea.

If you’ve just inherited a retirement account like an IRA or 401(k) from a parent, sibling, or relative, you may be unsure about what your options are and what to do next. Most non-spouse beneficiaries inheriting an IRA, 401(k), or retirement account from the original account owner must take the money in 10 years.

Achieving financial freedom in retirement requires meticulous planning, dedicated effort, and strategic management. Without a solid plan, you risk drifting without direction. Within this framework, the concept of the five pillars of retirementplanning emerges as a valuable strategy.

After you’ve spent your whole life working, you may find that in retirement, you want to give some money to charity. But if you are living off of income streams from sources like your retirement accounts and Social Security, you may be worried about finding a way to make charity work for your financial picture.

If you think retirementplanning moves stop at retirement, think again. Although it won’t make sense in every situation, retirement can be a unique opportunity for Roth conversions for some investors. For high earners, converting an IRA to a Roth IRA while you’re still working could be the worst time of all.

Financial advisors play a crucial role in assisting you before your retire. They can also help you optimize your savings and investment plans, ensuring that you maximize your earning potential while minimizing risks. Here are 5 benefits of hiring a financial advisor after you retire: 1.

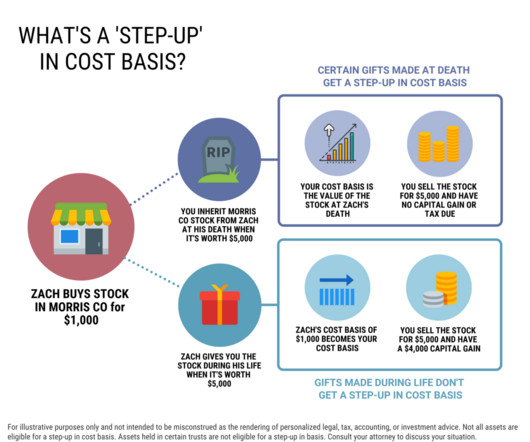

Example of a step-up in tax basis on stocks inherited at death What types of assets are eligible for a step-up? Non-retirement assets like stocks in a brokerage account, inherited home , antiques/art/collectables, or other real estate, are generally eligible for a step-up in cost basis.

A full list of tax provisions for states affected by natural disasters can be found here. In this article, well examine the most effective end-of-year tax strategies to help maximize your deductions and reduce your taxable income. Individual Retirement Accounts (IRAs): Contribute up to $7,000 for 2024 ($8,000 if aged 50+).

Congress is once again poised to make sweeping changes to the retirement and tax rules in the last two weeks of the year. retirement changes. retirement changes. In the new bill, the age when retirees must begin drawing from non-Roth tax-deferred retirement accounts would increase to 73 in 2023 and 75 in 2033.

just upended retirementplanning…again. The age when retirees must begin drawing from non-Roth retirement accounts increases to 73 in 2023, then 75 in 2033. Raising the age when withdrawals must begin is great as it gives investors more planning opportunities. The Secure Act 2.0

While most taxpayers dont need to worry about estate and gift taxes, having significant assets can make them a challenge. Also, like most UHNW individuals, you may have income from several sources like investments, real estate, and business interests that may require special taxplanning. Donate to qualified charities.

In this article, we’ll talk about what happens when you make this conversion and give you some examples of different financial situations for when this could be the right move for you. Like many retirement concerns, a Roth IRA has to be considered and handled delicately. Let’s say you’ve just changed jobs.

A financial or tax adviser can help you identify ways to capture that loss so you can offset gains from your liquidity event. Max out your retirement contributions. Many states provide tax benefits for 529 contributions, and earnings from a 529 aren’t subject to federal tax when used to pay for eligible schooling-related costs.

These are all interesting and important questions, but preparation for retirement is much more important than panicking over issues you have no control over. For many investors, however, the more important questions to ask and answer relate to your retirement strategy. Risk Tolerance: What is your asset allocation?

Blind spots in retirementplanning are those aspects that are often overlooked, either intentionally or subconsciously. From seemingly harmless low-interest debt to underestimating the emotional impact of transitioning out of the workforce, various factors can disrupt your peace of mind during your retirement years.

The ‘millionaires’ tax will also ensnare taxpayers who exceed the $1M limit after selling a home, business, stock options, or other types of one-time events. Article is a general communication only and should not be used as the basis for making any type of tax, financial, legal, or investment decision.

Backdoor strategies are retirement contribution methods that allow individuals to bypass income limits and contribute to tax-advantaged retirement accounts. The strategies typically involve making after-tax contributions to a traditional IRA or 401(k), then converting those funds into a Roth IRA or Roth 401(k).

According to a survey, a significant majority of Americans, approximately 80%, share the common notion that the point of working hard in your adult life is so you can enjoy a nice retirement. After years of dedicated labor and hard work, the prospect of a peaceful retirement appeals to everyone.

The passing of the 2019 Secure Act changed the rules about when non-spouse beneficiaries must begin taking money from inherited retirement accounts. The new guidelines currently wouldn’t alter existing post-Secure Act guidance for beneficiaries who inherited a retirement account from a non-spouse who died before reaching their RMD age.

You want to retire comfortably when the time comes. The truth is, saving for your retirement and your child’s education at the same time can be a challenge. Answering the following questions can help you get started: For retirement: How many years until you retire? Retirement takes priority.

When tax rates are stable, it’s wise for you to defer as much income as possible from one year to a later year and to accelerate deductions so that you can postpone payment of the tax. When you eventually realize the income at some future point, it’s possible that you’ll be retired and/or in a lower tax bracket.

This tax benefit is scheduled to sunset at the end of 2026. Taxplanning for 2026 Depending on your situation, income, and goals, your planning options will vary. As with anything in taxplanning, it’s important not to let the tax-tail wag the dog.

Planning can help optimize annual RMDs depending on your goals and cash flow needs. Mandatory withdrawals from retirement accounts begin for most taxpayers at age 72. For example, what’s the best time of year to take required minimum distributions, how to reinvest it, or if you can avoid paying tax on RMDs.

A good rule of thumb is to set aside at least 30% of every payment you receive to cover your estimated tax obligationshowever, this percentage may need to be adjusted based on your individual tax bracket. On the whole, its advisable to consult a tax adviso r to develop a dependable taxplan.

From retirementplanning to market volatility, equity compensation, family expenses, and major life transitions, it’s easy to feel overwhelmed with financial responsibilities. Those are the years when all your hard work pays off, and the last thing you want to do is worry about how you’ll afford your dream retirement lifestyle.

Navigating the complex world of personal finance, especially with retirement looming on the horizon, can be daunting. Working with a financial advisor can significantly enhance your chances of retiring with more wealth. Hiring the best financial advisors for retirement can lead to better savings and investment outcomes.

Most people feel a sense of anticipation and excitement before retirement. Yet, amidst the joy and delight, it is vital to remember that the journey to retirement is not one to be rushed. Hasty decisions made before retirement can lead to unexpected financial troubles and compromises.

Common types of assets that will pass via beneficiary designation include retirement accounts, life insurance, and some pensions and annuities. This article is a high-level overview of the various estate planning techniques and considerations when using revocable living trusts from the perspective of a wealth advisor (e.g.

There are lots of material legal issues at play which are entirely outside the scope of this article. This can also help with longer term taxplanning optimization. Questions to ask the company (and possibly negotiate depending on the answer) Is the company is planning to update the 409a soon?

However, unlike stocks and bonds, alternative investments, or alts as theyre commonly known, have unique tax treatments and complex reporting requirements that investors should carefully consider before investing. Can I hold alternative investments in my retirement accounts? This article is a product of Harness Tax LLC.

In a recent CNBC article, our Wealth Advisor, Catalina Franco-Cicero, MS, CFP®, CTS , was quoted on the topic of tax strategies during periods of unemployment. However, a period of lower income in 2024 could present valuable taxplanning opportunities.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content