This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Ed Yardeni, President of Yardeni Research , a provider of global investment strategies and asset-allocation analyses and recommendations. He previously served as Chief Investment Strategist of Oak Associates, Prudential Equity Group, and Deutsche Bank’s US equities division in New York City.

Thoughts Equity markets look to extend their winning streak to three weeks despite continued uncertainty in the banking sector. Fund managers remain historically conservative per Bank of America’s Global Fund Manager Survey showing assetallocators long cash and short equities. over the past two weeks.

Strategy Shifting your assetallocation based on economic forecasts is a fool's errand. blogs.cfainstitute.org) Banks Bitcoin is benefiting from the banking crisis. theirrelevantinvestor.com) Bank turmoil is now on everyone's dance card for 2023. washingtonpost.com) Why public restrooms in the U.S.

RBI also goes in tandem with the other central banks regarding rate cuts to maintain stability in the exchange rate and avoid the risk of loosening too early. Consequently, the portfolio allocation should reflect these probabilities depending on the risk profiles. Other Asset Classes: Gold sparkled in the last quarter, going up by 9%.

It has been my experience when reviewing portfolios that diversification is typically expressed simply as a number of various stocks owned, or owning a handful of asset classes, usually stocks of various sizes and geographies, and bonds of varying maturities.

It’s a town of about 4,000 people, so exposure to markets or investment banking or any of the careers in finance was not something that you really envisioned. And so, coming out of school, I studied Economics and Spanish Literature, and I applied to a — a program that actually targeted Liberal Arts majors. RITHOLTZ: Right.

We’ve seen some signs of credit buckling earlier this year with the bank panic, but so far it’s remained mostly under control. The financial markets are especially jittery during periods like this because there is so much uncertainty about the future impact of policy and economic activity.

His latest book could not be more timely, “The Price of Time: The Real Story of Interest,” it’s all about the history of interest rates, money lending, investing speculation, funded by banks and loans and credit. And Jeremy said, “Well, at least there’s enough structural redundancy in the banking system.”

Rooted in the firm’s deep capital market analysis, the CMA report informs the investment decisions and assetallocation recommendations made by Northern Trust, which as of June 30, 2023, had US$1.4 trillion in assets under management.

Central bank actions and future policy signals influenced by US election outcomes, will be crucial for the rest of the financial year. Given the high valuations and fuzzy near-term outlook, our ideal strategy is to stick the assetallocation framework which best suits our risk profile. The current P/E Multiple of ~24.5x

So I switched to be an economics major. I graduated economics with, with a lot of coursework in accounting and finance. So they’d give individual assetallocation to people and they’d go invest their money. And so I remember back, back in 2005 when we first started, you know, we think about the banks.

Understanding Modern Portfolio Construction Understanding the Modern Monetary System Everything you need to know about finance and investing in less than an hour How The Economic Machine Works in 30 Minutes Section 1 – Understanding Money & the Macroeconomy What Is Money? What Are Central Bank Reserves? Where Does Money Come From?

But before proclaiming cash is king and parking your money in an FDIC insured bank account, consider your time frame and how you plan to use the money. It’s the reference interest rate for overnight borrowing between financial institutions like banks. Hold cash or invest?

Instead, we got a shockingly fast collapse of a financial institution with over $200 billion in assets, which turned the market’s focus toward the stability of the banking system and what systemic risks banks might be facing. Recent economic data has pointed to continued growth—giving rise to the “no landing” narrative.

After the subprime crisis in 2008, many developed countries’ Central Banks started printing money and flooding the global economies with cheap liquidity. The quantum of money printing jumped massively after Corona-led economic shutdowns. But first a quick recap. US Fed increased its balance sheet size from ~$4-4.5 trillion to ~$8-8.5

Combined with India’s own economic strength and lower interest rates, asset prices—stocks, real estate, gold—could rise even further. The assumption that asset prices will keep rising can quickly be challenged by things like escalating geopolitical tensions, a U.S. What does this mean for India? But so will inflation!

The interesting question is why the recession has yet not occurred even after one of the fastest increases in interest rates in history by all the major Central Banks in a very short span of time. We continue to stay under-allocated to equity (check the 3rd page for assetallocation) at the current valuation levels.

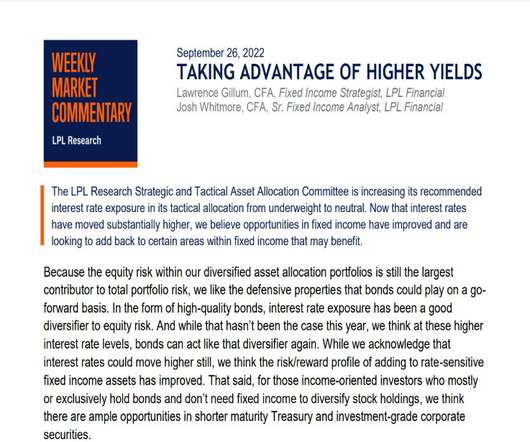

The LPL Research Strategic and Tactical AssetAllocation Committee is increasing its recommended interest rate exposure in its tactical allocation from underweight to neutral. As we know from historical precedents, when the Fed aggressively raises rates, economic growth slows or outright contracts, which is the Fed’s goal.

Significant debasement of money has happened and will continue to happen as per the promises made by the Central banks all around the world. There is no price for guessing that gold as an asset class can protect against the risk created by the actions of our policy makers. Nifty currently is trading at a multi-year’s high valuation.

By the way, speaking of financials, and specifically bank stocks… this news is hot off the press with Silicon Valley Bank collapsing this past week. Trading on First Republic Bank ( FRC ) was halted on Friday and that’s clearly a serious cautionary sign of what could happen to them and other smaller, regional names.

Many believe that the possibility of losses is very minimal since the central banks are on their side. To quantify, the Central bank of the USA – Fed printed more than 20% of total US dollars ever printed in the last year. Why then central banks never did such a thing earlier which can make so many people wealthy.

As with many things in life, the truth is somewhere between the extremes: While both simulated and real-world data suggest momentum may not be suitable as a driver of long-term assetallocations, we believe momentum considerations can be integrated in a cost-effective way to help inform daily portfolio management decisions.

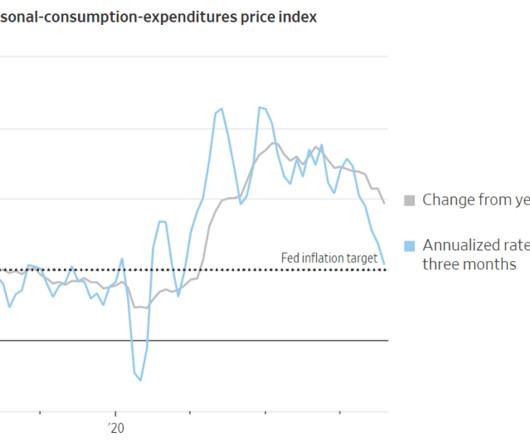

Source: Trading Economics Declining inflation and interest rates explain a lot of investor optimism, but there are additional reasons to be sanguine. There are always plenty of unforeseen issues that could slow or reverse our economic train. a few months ago to 3.9% today (see chart below). Source: Yardeni.com What could go wrong?

Some recent softening in economic data, coupled with signals from the bond market, may be indicating that Fed policymakers’ concerted inflation fight may be closer to the end than the beginning. We should also have slowing corporate earnings growth and greater economic uncertainty to contend with, some formidable seas to navigate.

They like to talk about Bajaj Finance and not Yes Bank in their portfolio. Most of the time, even the winners account for very low weight in the overall assets, resulting in miniscule contribution to the portfolio returns. We continue to hold positions in large-cap value stocks and maintain no allocation to mid & small-cap funds.

However, the impending end of the Federal Reserve (Fed) rate-hiking campaign, and the economy’s and corporate America’s resilience, help make the bull case that steers LPL Research toward a neutral, rather than negative, equities view from a tactical assetallocation perspective. Diversification does not protect against market risk.

EUROPEAN RE-ENTRY: Why We Are Shifting Portfolios Toward European Stocks achen Thu, 06/01/2017 - 02:47 Assetallocation—at least for us—is an exercise in nuance. We move slowly and carefully when it comes to shifting our portfolios away from one asset class or region and toward another.

Assetallocation—at least for us—is an exercise in nuance. We move slowly and carefully when it comes to shifting our portfolios away from one asset class or region and toward another. EUROPEAN RE-ENTRY: Why We Are Shifting Portfolios Toward European Stocks. Thu, 06/01/2017 - 02:47.

In their updated “ Summary of Economic Projections ,” they revised their estimates of core inflation for 2023 down from 3.7% Markets were off to the races after the Fed released its statement and economic projections. has now raced ahead of other developed markets in economic growth since the pandemic. Here’s why.

While you can keep your emergency fund in any account you want, it’s smart to look for online banks that pay high rates on savings, money markets, and certificates of deposit (CDs). Some examples of banks that fit the bill include: CIT Bank Synchrony Bank BBVA (formerly BBVA Compass). 88 cents on your behalf.

Cash in consumer wallets and money in the bank help the economy keep chugging along at a healthy clip. Source: Trading Economics As long as consumers continue to hold a job, they will continue spending to buoy economic activity – remember, consumer spending accounts for roughly 70% of our country’s economic activity.

JOHNSON: And then I moved into, we had a bank at the time, and I moved into running part of the bank. RITHOLTZ: So Franklin obviously divests out of the banking business, the credit card business, the auto financing business. The requirements for asset managers to have a bank were such that it would inhibit us a bit.

Strong Defense: The Falling Opportunity Cost of Allocating to Bonds ajackson Tue, 07/24/2018 - 09:25 For years, “defense” in portfolios—i.e., allocations to cash and core fixed income holdings—has meant a willingness to accept extremely low returns. stocks play in most investors’ core equity allocations.

allocations to cash and core fixed income holdings—has meant a willingness to accept extremely low returns. But after many years of economic recovery, we finally have reached a point where defensive allocations once again provide a reasonable yield. stocks play in most investors’ core equity allocations.

Economic activity does not stop like an airplane eventually does, but rather the economy will settle into a steady state where growth is consistent with factors such as population and productivity. Perhaps that was not the first time market watchers used the term, but the conversations at the Economic Club of New York were prescient.

That’s not suggesting another 2008 is coming, but rather highlights how fast the economic environment can change. Along with the statement, the Committee updated the Summary of Economic Projections (SEP), which is arguably more important than the brief monetary policy statement.

Ahead of the first tightening by the Federal Reserve in nine years, we are shifting into less-traditional assets, anticipating that, at best, U.S. stocks and fixed income securities will probably languish when the central bank begins to withdraw record stimulus. Concern about future economic growth undermines valuations.

While activity remains muted at best, expectations are focused on 2024, when there is a prevailing consensus that the Federal Reserve (Fed) will be finished with its rate hike campaign, and that economic conditions will be resilient enough to underpin a strong capital markets environment. With economic data continuing to suggest the U.S.

Economic and corporate data support the initial strong reads on holiday retail sales despite the macro headwinds, reinforcing the idea that today’s consumer is in a better position than usual at this point in the business cycle. Any economic forecasts set forth may not develop as predicted and are subject to change.

While February’s volatility did not materially change our assetallocation views, it reinforced to us the importance of a comprehensive discussion about how we think about risk and how we manage it. Our assetallocation process accounts for a wide range of potential outcomes over the next 18–36 months.

I was born in London and when I was three and a half, my father got a job for the World Bank in Washington DC So we all moved to Washington DC Then just before my 10th birthday, my father was posted to Bangladesh for four years. And I think it partly depends on the economic comfort in which you grew up. Where, where did you grow up?

could fall victim to long-term economic stagnation, similar to the fate that befell Japan starting in the 1990s. Japan’s GDP had grown by an average of more than 5% per year from 1950 to 1989—a true post-War economic miracle. As important, however, is the contrast in how the two countries have dealt with financial or economic crises.

could fall victim to long-term economic stagnation, similar to the fate that befell Japan starting in the 1990s. Investors who were active in the late 1980s will recall that asset prices in Japan reached extreme levels as money poured into the country from all over the world, propelled by extraordinary economic growth.

Through conservative, bottom-up analysis, we are taking advantage of current market dynamics to buy attractively priced debt in companies with solid revenues and limited vulnerability to an economic downturn. Debt in well-managed companies positioned to weather an economic slump return nearly three times the 2.3%

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content