This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

This week, we speak with Savita Subramanian , head of US Equity and Quantitative strategy at Bank of America. He helps to oversee DoubleLine’s investment management committee implementing policies & processes, He is a member of DoubleLine’s executive management and fixed income assetallocation committee.

2021 AssetAllocation Perspectives and Outlook. Valuations seem stretched, and there may be many signs that animal spirits are soaring. The impact of the COVID-19 pandemic and the potential consequences of the unprecedented response by central banks and policy makers. Fri, 02/26/2021 - 13:22. Download the full report >.

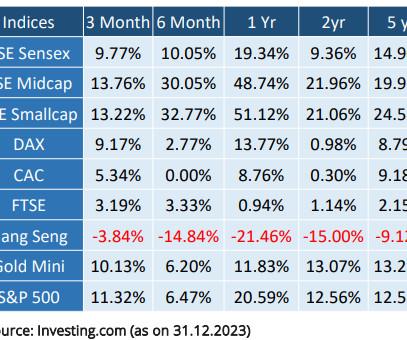

RBI also goes in tandem with the other central banks regarding rate cuts to maintain stability in the exchange rate and avoid the risk of loosening too early. Indian equity benchmark BSE Sensex went up by only 2% due to already stretched equity valuations. Other Asset Classes: Gold sparkled in the last quarter, going up by 9%.

AssetAllocation: Caution Toward High Dividend Yielding Stocks achen Fri, 10/28/2016 - 11:25 Why Have High Dividend Yielding Sectors Done Well This Year? In response to weak nominal growth, central banks have maintained accommodative monetary policies, pushing interest rates to historic lows. billion in assets they held in 2011.

AssetAllocation: Caution Toward High Dividend Yielding Stocks. In response to weak nominal growth, central banks have maintained accommodative monetary policies, pushing interest rates to historic lows. According to Morningstar, overall assets in dividend-focused ETFs and mutual funds have ballooned to $672.6

Historically, this bracket has been dominated by the tech sector, but after years of outsized gains, big tech valuations are stretched. Small & Mid-Cap Region: SOFI Surges in a Changing Market The small and mid-cap asset class has long been overshadowed by large-cap dominance, with the past decade favoring mega-cap technology stocks.

Investment banks were not really a known concept in the area where I grew up. I lined up a bunch of job interviews with a variety of banks. So I got to know banks a little bit. So I interviewed with a bunch of banks, got a number of job offers by the end of the week, and joined Goldman Sachs in October 1998.

His latest book could not be more timely, “The Price of Time: The Real Story of Interest,” it’s all about the history of interest rates, money lending, investing speculation, funded by banks and loans and credit. And Jeremy said, “Well, at least there’s enough structural redundancy in the banking system.”

Several factors were common between the two markets: robust corporate earnings growth, expected cuts in interest rates and a shift in investor expectations from a valuation-led phase to an earnings-led phase. Central bank actions and future policy signals influenced by US election outcomes, will be crucial for the rest of the financial year.

IBM loses to QCOM based on valuation. By the way, speaking of financials, and specifically bank stocks… this news is hot off the press with Silicon Valley Bank collapsing this past week. Watch for those that have even worse financials and balance sheets than SVB did.

After one of the fastest increases in interest rates in history by all the major Central Banks in a matter of 12 months to contain inflation, the cracks have started showing in the form of bank collapses in the USA (SVB and Signature) and Europe (Credit Suisse). 5%) and by RBI (25 bps to 6.5%). For the last 1.5

The interesting question is why the recession has yet not occurred even after one of the fastest increases in interest rates in history by all the major Central Banks in a very short span of time. The recent rally in the market has made the valuations more expensive compared to historical standards.

After the subprime crisis in 2008, many developed countries’ Central Banks started printing money and flooding the global economies with cheap liquidity. However, we can think of three possible scenarios ahead: Irrespective of what scenario will pan out, equity valuations inevitably have to adjust according to the principle of mean reversion.

Instead, we got a shockingly fast collapse of a financial institution with over $200 billion in assets, which turned the market’s focus toward the stability of the banking system and what systemic risks banks might be facing. But valuations strongly favor value over growth.

So they’d give individual assetallocation to people and they’d go invest their money. And so I remember back, back in 2005 when we first started, you know, we think about the banks. The banks would have an equity trading desk and they’d have a debt desk, right? H how did you figure that out?

Significant debasement of money has happened and will continue to happen as per the promises made by the Central banks all around the world. There is no price for guessing that gold as an asset class can protect against the risk created by the actions of our policy makers. Nifty currently is trading at a multi-year’s high valuation.

The exchange also received the CII EXIM Bank Excellence Prize in 2014 and 2016. Key indicators like banked population and market capitalization improved. Indian households traditionally invested most savings in physical assets. However, financial assetallocation increased recently. lakh crore and ₹3.1

The assumption that asset prices will keep rising can quickly be challenged by things like escalating geopolitical tensions, a U.S. This is where our disciplined dynamic assetallocation approach will really shine, keeping us steady through any rough waters ahead. The tech sector, too, was a star with BSE IT returning 13.71%.

They like to talk about Bajaj Finance and not Yes Bank in their portfolio. Most of the time, even the winners account for very low weight in the overall assets, resulting in miniscule contribution to the portfolio returns. We continue to hold positions in large-cap value stocks and maintain no allocation to mid & small-cap funds.

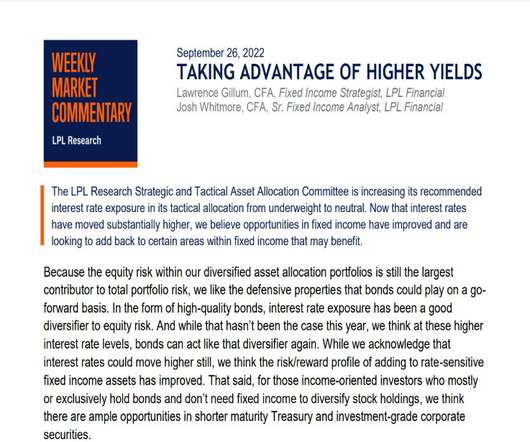

The LPL Research Strategic and Tactical AssetAllocation Committee is increasing its recommended interest rate exposure in its tactical allocation from underweight to neutral. Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. All index data from FactSet.

My mental image was that he worked in the bank of, back of a bank approving mortgage applications. And speaking of the.com implosion, like Microsoft via a case study where we, in previous strategies, we held Microsoft for a very long time, that’s where the valuation could help us in the.com bus. It was over 50 right?

Sentiment cycles move from one extreme of greed to another extreme of fear which takes valuations also to extremes from their long-term averages. At the extreme of fear sentiment (which coincides with dirt-cheap valuations), the risk-reward is highly favorable i.e., higher potential upside with lower potential downside risk.

However, the impending end of the Federal Reserve (Fed) rate-hiking campaign, and the economy’s and corporate America’s resilience, help make the bull case that steers LPL Research toward a neutral, rather than negative, equities view from a tactical assetallocation perspective. At the same time, the resilience of the U.S.

Ahead of the first tightening by the Federal Reserve in nine years, we are shifting into less-traditional assets, anticipating that, at best, U.S. stocks and fixed income securities will probably languish when the central bank begins to withdraw record stimulus. Concern about future economic growth undermines valuations.

While February’s volatility did not materially change our assetallocation views, it reinforced to us the importance of a comprehensive discussion about how we think about risk and how we manage it. Our assetallocation process accounts for a wide range of potential outcomes over the next 18–36 months.

economy to avoid recession, and support above-average valuations. The relationship between inflation and stock valuations is a strong one, as shown in Figure 2 , which meant the market could no longer support price-to-earnings (P/E) ratios over 20 (the same goes for the relationship between interest rates and stock valuations).

EUROPEAN RE-ENTRY: Why We Are Shifting Portfolios Toward European Stocks achen Thu, 06/01/2017 - 02:47 Assetallocation—at least for us—is an exercise in nuance. We move slowly and carefully when it comes to shifting our portfolios away from one asset class or region and toward another. is not particularly notable.

Assetallocation—at least for us—is an exercise in nuance. We move slowly and carefully when it comes to shifting our portfolios away from one asset class or region and toward another. EUROPEAN RE-ENTRY: Why We Are Shifting Portfolios Toward European Stocks. Thu, 06/01/2017 - 02:47. is not particularly notable.

But beyond the economic cycle’s age, several factors suggest that a more defensive mindset is worth considering: Valuations are elevated. Robust Q1 2018 earnings growth improved the valuation picture for U.S. It is worth noting that valuations are more reasonable in developed international and emerging markets; however, U.S.

But beyond the economic cycle’s age, several factors suggest that a more defensive mindset is worth considering: Valuations are elevated. Robust Q1 2018 earnings growth improved the valuation picture for U.S. It is worth noting that valuations are more reasonable in developed international and emerging markets; however, U.S.

As with many things in life, the truth is somewhere between the extremes: While both simulated and real-world data suggest momentum may not be suitable as a driver of long-term assetallocations, we believe momentum considerations can be integrated in a cost-effective way to help inform daily portfolio management decisions.

In good times i.e. when the market valuations are usually very high, everyone agrees to the logic of buying low and selling high. Not understanding the role & importance of tactical assetallocation (overweight debt in euphoric times and overweight equity in a time of acute pessimism) in creating superior returns over the long term.

One equity market debate discussed frequently in the LPL Research Strategic & Tactical AssetAllocation Committee (STAAC) is the growth vs. value style reversal experienced the past 12 months. Increasing the discount rate, which lowers the present value of future cash flows, and company valuations.

Later on, funding becomes essential, either via private equity, venture capital, or a direct relationship with investment banks, and even the Bank of Mom and Dad. sectors) with the exception of preferred securities, which look attractive after having sold off due to stresses in the banking system.

Retailer valuations have also taken a hit, as the forward (next 12 months) P/E multiple has contracted ~20% year to date, from ~27x to ~22x currently. Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. All index data from Bloomberg. 12/2023).

Still, as we survey what are better equity valuations, long-awaited income opportunities in the bond market, and a likely less-antagonistic Fed in 2023, there may be emerging reasons to believe that the next year may be more constructive than the last. Assetallocation does not ensure a profit or protect against a loss.

Higher interest rates are challenging stock valuations and perhaps pushing the gains further out in 2023, but we still see solid potential for double-digit returns for stocks this year. Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. All index data from FactSet.

I was born in London and when I was three and a half, my father got a job for the World Bank in Washington DC So we all moved to Washington DC Then just before my 10th birthday, my father was posted to Bangladesh for four years. Barry Ritholtz : So you are from the uk but you’ve spent a lot of time in the us.

We tend to be strategic rather than tactical in our approach to investing, but a combination of recent fundamental developments and valuation changes has caused us to add a note of caution in conversations with clients and in the management of their portfolios. Concentration: Much of the U.S.

We tend to be strategic rather than tactical in our approach to investing, but a combination of recent fundamental developments and valuation changes has caused us to add a note of caution in conversations with clients and in the management of their portfolios. Concentration: Much of the U.S. Risks in Bonds.

The Strategic and Tactical AssetAllocation Committee’s (STAAC) S&P 500 year-end fair value target of 4,000-4,100 is based on a price-to-earnings ratio of 17.5 It is also a major component used to calculate the price-toearnings valuation ratio. times the STAAC’s 2023 S&P 500 earnings per share forecast of $230.

LPL’s Strategic and Tactical AssetAllocation Committee (STAAC) recommends a neutral tactical allocation to equities, with a modest overweight to fixed income funded from cash. sectors) with the exception of preferred securities, which look attractive after having recently sold off due to the banking stresses.

We maintain our preference for equities over fixed income and cash in our recommended tactical assetallocation. Stock valuations are higher but bond yields are still low enough to support valuations with the 10-year Treasury yield well under 3% despite the big jobs number. All index data from FactSet.

In Engines That Move Markets, a 2002 book about the cycles of technology investing, Alasdair Nairn defines “bubbles” as periods when investors appear to suspend rational valuation, much as they had during the dotcom craze shortly before the book was published. Unsurprisingly, as volume has increased, so have valuations. Possible Signs.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content