This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

2023 AssetAllocation Perspectives and Outlook ajackson Mon, 03/06/2023 - 14:43 We are pleased to share Brown Advisory’s 2023 Outlook. Each year, the Annual Outlook report assesses the current investment landscape and discusses some of the main themes being expressed in client portfolios.

2021 AssetAllocation Perspectives and Outlook. Each year, our Investment Solutions Group (ISG) assess the current investment landscape and discuss how we are positioning client portfolios. Each year, the Annual Outlook report assesses the current investment landscape and discusses how we are positioning client portfolios.

2023 AssetAllocation Perspectives and Outlook ajackson Mon, 03/06/2023 - 14:43 We are pleased to share Brown Advisory’s 2023 Outlook. Each year, the Annual Outlook report assesses the current investment landscape and discusses some of the main themes being expressed in client portfolios.

(ADVERTISEMENT) RITHOLTZ: Tell us a little bit about what the Goldman Sachs asset and wealth management business is like. SALISBURY: At the simplest level we manage money for our clients. trillion dollars of assets today. Three main client segments. SALISBURY: Look, every client is different. What do they focus on?

I wonder what stories will be told when the portfolios will decline to such an extent for those who are not following a suitable assetallocation. During this recent correction, none of our clients reached out to us with concerns. Because our client’s portfolios declined much less than the correction in the markets.

AssetAllocation: Caution Toward High Dividend Yielding Stocks achen Fri, 10/28/2016 - 11:25 Why Have High Dividend Yielding Sectors Done Well This Year? According to Morningstar, overall assets in dividend-focused ETFs and mutual funds have ballooned to $672.6 billion in assets they held in 2011. Reach for yield.

AssetAllocation: Caution Toward High Dividend Yielding Stocks. According to Morningstar, overall assets in dividend-focused ETFs and mutual funds have ballooned to $672.6 billion in assets they held in 2011. Stretched Valuations. Fri, 10/28/2016 - 11:25. Why Have High Dividend Yielding Sectors Done Well This Year?

CIO Perspectives Webinar, 2022 AssetAllocation Outlook mhannan Fri, 03/18/2022 - 06:42 Markets have been unsteady at the start of 2022, driven by geopolitical tensions, inflation, and concerns about equity valuations. The war in Ukraine is causing even more uncertainty. Rodrigo is now available.

CIO Perspectives Webinar, 2022 AssetAllocation Outlook. Markets have been unsteady at the start of 2022, driven by geopolitical tensions, inflation, and concerns about equity valuations. CIO Perspectives Webinar, 2022 AssetAllocation Outlook . Fri, 03/18/2022 - 06:42. Download transcript. Watch the Video.

A client said – I understand market valuations are expensive but it doesn’t seem that it will correct much. The fundamental driver of market peaks and exorbitant valuations is the perception that there is nothing to worry about – there is no investment risk. There is nothing to worry about.

Assetallocation for a year where bonds offer the most attractive returns they have compared to the expected returns for stocks in decades. MORE ON THIS TOPIC 2023 AssetAllocation Perspectives and Outlook We are pleased to share Brown Advisory’s 2023 Outlook. multinationals and aggregate demand.

The recent rally in the market has made the valuations more expensive compared to historical standards. However, heightened valuations do not provide comfort in replicating higher returns of the past in the medium term. Valuations across all sectors do not offer any margin of safety.

Higher valuation of Indian markets compared to Global peers along with negligible earnings growth also didn’t help. One should not be over-allocated to equity (check the 3rd page for assetallocation) at the current levels and any exposure should primarily be towards large cap-oriented value portfolios against growth stocks.

Still, as we survey what are better equity valuations, long-awaited income opportunities in the bond market, and a likely less-antagonistic Fed in 2023, there may be emerging reasons to believe that the next year may be more constructive than the last. Assetallocation does not ensure a profit or protect against a loss.

By Taylor Graff, Head of AssetAllocation Research and Ed Chadwyck-Healey, Head of International Private Clients ⚑ Investment Outlook Falling Interest Rates Trigger Investor Hunger For Yield Investors snapping up U.S. securities are seeking yield as much as safety as interest rates plunge toward record lows.

By Taylor Graff, Head of AssetAllocation Research and Ed Chadwyck-Healey, Head of International Private Clients ? Equities Private Credit Outshines Many High-Valuation Stocks, Bonds. Consequently, investors need to build a solid defensive position while seizing opportunities that arise amid the instability.

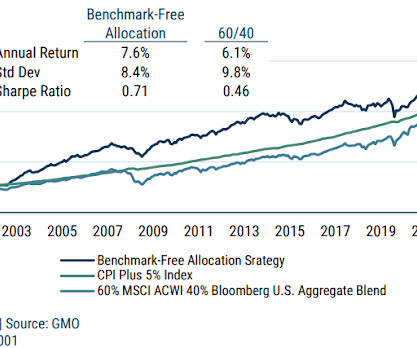

GMO posted a short paper in support of its Benchmark Free AssetAllocation Strategy (BFAAS). For this post we'll focus on BFAAS' assetallocation. The asset mix is 53.6% A more detailed look at the asset mix shows the the following. BTAL is a client and personal holding. to equities, 29.7%

Throughout 2017, our meetings and conversations with clients very frequently focused on the topic of risk. While February’s volatility did not materially change our assetallocation views, it reinforced to us the importance of a comprehensive discussion about how we think about risk and how we manage it. Fri, 03/30/2018 - 11:57.

We’re currently seeing one of the largest disparities in valuations between growth and value stocks which in our opinion presents a very appealing opportunity for dividend seeking investors. Going forward we’ll update our readers and clients about the strategy and performance on a quarterly basis.

And ev all the sort of compliance, client service, legal, kind of, everything was done sort of on the side by investment people. So it’s, 00:09:11 [Speaker Changed] You’ve become an enterprise, it’s 10 x what it once was in terms of headcount, it’s much bigger in terms of assets. 00:18:41 [Speaker Changed] Yep.

In this paper, we will discuss our framework for spend-rate analysis, and how we help our endowment and foundation clients translate this analysis into decisions for their portfolios. Each “shoestring” curve represents the expected outcomes for various allocation targets, assuming a given spend rate.

In this paper, we will discuss our framework for spend-rate analysis, and how we help our endowment and foundation clients translate this analysis into decisions for their portfolios. Each “shoestring” curve represents the expected outcomes for various allocation targets, assuming a given spend rate.

It requires not just sophisticated skill-set for assetallocation calls (across asset classes, sub-categories, and schemes), the temperament to keep emotions under check but also an ability to quickly understand the impact of the latest market developments (global and domestic) on various asset classes in a rapidly-changing world.

Our job was basically to give sort of strategic advice to Lazard clients, which would generate capital-raising mergers and debt financing. I remember once, one of my colleagues says that a friend, one of the French Lazard Frerers partners was asked by a sort of junior, “How much should we tell our client to bid?” CHANCELLOR: Yes.

EUROPEAN RE-ENTRY: Why We Are Shifting Portfolios Toward European Stocks achen Thu, 06/01/2017 - 02:47 Assetallocation—at least for us—is an exercise in nuance. We move slowly and carefully when it comes to shifting our portfolios away from one asset class or region and toward another. is not particularly notable.

Assetallocation—at least for us—is an exercise in nuance. We move slowly and carefully when it comes to shifting our portfolios away from one asset class or region and toward another. We maintain a model portfolio internally to track the results of our assetallocation stances. Thu, 06/01/2017 - 02:47.

Alternatively, nonprofits can boost potential portfolio returns, which often means tolerating more risk and illiquidity, through a recalibration of assetallocation— the single biggest driver of long-term gains. We believe that this structure enables our clients to contain risk while meeting their long-term objectives for returns.

But beyond the economic cycle’s age, several factors suggest that a more defensive mindset is worth considering: Valuations are elevated. Robust Q1 2018 earnings growth improved the valuation picture for U.S. It is worth noting that valuations are more reasonable in developed international and emerging markets; however, U.S.

But beyond the economic cycle’s age, several factors suggest that a more defensive mindset is worth considering: Valuations are elevated. Robust Q1 2018 earnings growth improved the valuation picture for U.S. It is worth noting that valuations are more reasonable in developed international and emerging markets; however, U.S.

But the drop in valuations experienced at year’s end, alongside higher bond yields, offer a foundation for better long-term return expectations across most asset classes. Given that backdrop, many of our client conversations during the back half of 2018 centered on how we might balance these opportunities and risks. In non-U.S.

In anticipation of the policy switch, we have reallocated across a wide range of asset classes in an effort to limit risks and seize new opportunities. In many clients’ portfolios we have eliminated our overweight position in U.S. Concern about future economic growth undermines valuations. stocks after trimming exposure to U.S.

When macro conditions are uncertain, a banker’s approach to valuation can help. David, a former investment banker, has always brought a banker’s mentality to valuing smaller companies by breaking down their assets and operations into components that can be more accurately assessed.

As with many things in life, the truth is somewhere between the extremes: While both simulated and real-world data suggest momentum may not be suitable as a driver of long-term assetallocations, we believe momentum considerations can be integrated in a cost-effective way to help inform daily portfolio management decisions.

In good times i.e. when the market valuations are usually very high, everyone agrees to the logic of buying low and selling high. Not understanding the role & importance of tactical assetallocation (overweight debt in euphoric times and overweight equity in a time of acute pessimism) in creating superior returns over the long term.

We tend to be strategic rather than tactical in our approach to investing, but a combination of recent fundamental developments and valuation changes has caused us to add a note of caution in conversations with clients and in the management of their portfolios. Just to be clear, this is not a sudden or abrupt shift in our thinking.

We tend to be strategic rather than tactical in our approach to investing, but a combination of recent fundamental developments and valuation changes has caused us to add a note of caution in conversations with clients and in the management of their portfolios. Just to be clear, this is not a sudden or abrupt shift in our thinking.

By walking through four steps with a client, we can refocus his or her mindset on the fundamental issues that help safeguard financial stability and achieve steady outperformance. Here are four ways we think about preparing clients to stay the course regardless of the market’s mood: Clarify your mission. Set hard numbers.

In Engines That Move Markets, a 2002 book about the cycles of technology investing, Alasdair Nairn defines “bubbles” as periods when investors appear to suspend rational valuation, much as they had during the dotcom craze shortly before the book was published. Unsurprisingly, as volume has increased, so have valuations. Possible Signs.

Second, if investors aren’t willing to assign the same valuation to stocks (due to higher interest rates and uncertainty), that also has a negative effect. We’ve spent considerable time looking for unique combinations of these portfolios in an attempt to find the mix that is best for our retired and risk-adverse clients.

These items are not static, and can change over time, therefore it’s important to revisit your assetallocation periodically as financial circumstances and life events change your objectives. Short-term news cycle headlines shouldn’t drive portfolio decision-making, but rather your personal objectives, goals, and risk tolerance.

So I was a mile deep on a subject matter of bond indexing, but now I had the opportunity to lead an equity indexing group, the entire fixed income team, our investment strategy team that does research for our clients around portfolio construction, those types of things. It’s client related, it’s media like we’re doing today.

At Sidoxia , we are determined to objectively stick to the facts and migrate investments to the areas of the market that provide the best risk-reward opportunities to our clients, based on their unique objectives and constraints. They certainly could, but valuations remain attractive given where interest rates currently stand.

But today, you know, a lot of brokers, you know, whether they’re with the big full service brokerage firms now have advisory accounts that they flog to clients where they can buy ETFs. And one of the common conversations is, I have a client, he’s got millions of dollars invested. We can’t get him to spend money.

Investment Perspectives | Real Returns achen Fri, 07/01/2016 - 06:00 One of the most penetrating and recurring questions we receive from clients is, “what is a reasonable long-term expectation for U.S. Private clients typically find themselves in a similar position, although they may not describe it in the same terms.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content