This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Strategy High uncertainty decisions, like investing, are by definition difficult. behaviouralinvestment.com) Do commodities have a role to play in a long-term, strategic assetallocation? bloomberg.com) SpaceX's valuation keeps rising, due in part to Starlink's success.

The economy has decelerated sharply in the last year, but we aren’t seeing data that is consistent with what the NBER would define as a “recession” So how concerned should we be about these technical definitions? In our view we’re still in the “muddle through” camp as it pertains to the economy.

Anytime I talk about letting markets work for you over the long term and the role that an adequate savings rate plays in financial success, I will usually caveat that with assuming a proper assetallocation. But down 40% and the multi-asset fund we've been talking about is still going to be pretty close to 25% in precious metals.

Definitely not! The simple solution is assetallocation. The investment in equity or any other risky asset class should not be a 0 or 1 game – get out or get in 100%. 35% when markets are extremely expensive and 80% when they are extremely cheap as per the historical valuation standards.

00:13:13 [Speaker Changed] It’s an improvement of value or refinement on the definition of value. 00:15:17 [Speaker Changed] So let’s get into some of the definitions of this. So as those assets, the relevance and then capital discipline are the key components for us. Is that, is that what you’re suggesting?

We’re currently seeing one of the largest disparities in valuations between growth and value stocks which in our opinion presents a very appealing opportunity for dividend seeking investors. While everyone is bantering about the official definitions of what a recession is, we’re very likely to see a period of stagflation.

While February’s volatility did not materially change our assetallocation views, it reinforced to us the importance of a comprehensive discussion about how we think about risk and how we manage it. Our assetallocation process accounts for a wide range of potential outcomes over the next 18–36 months.

But the drop in valuations experienced at year’s end, alongside higher bond yields, offer a foundation for better long-term return expectations across most asset classes. This is also a fitting moment to review the intersection of risk and valuation. Entering 2019, we face rising economic, political and market risks. In non-U.S.

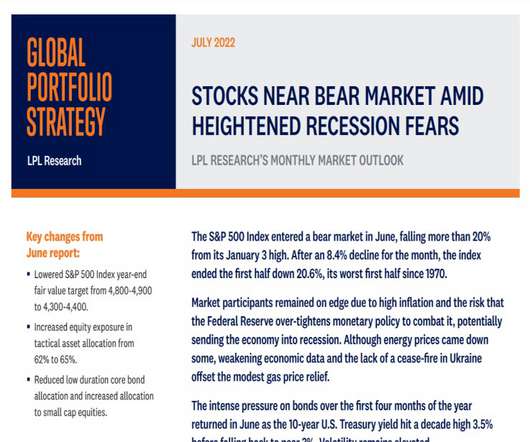

Increased equity exposure in tactical assetallocation from 62% to 65%. Reduced low duration core bond allocation and increased allocation to small cap equities. The Strategic and Tactical AssetAllocation Committee (STAAC) changed its recommended assetallocation for July, shifting from core bonds to small cap equities.

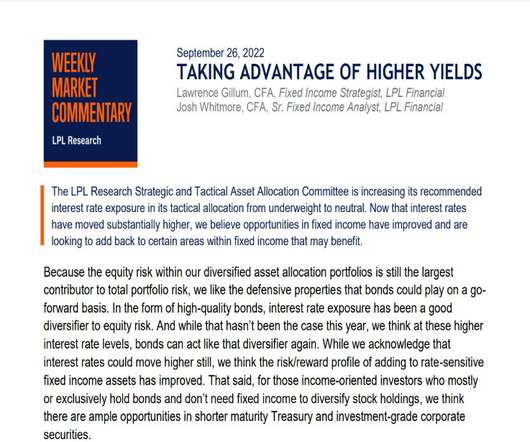

The LPL Research Strategic and Tactical AssetAllocation Committee is increasing its recommended interest rate exposure in its tactical allocation from underweight to neutral. Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock.

Sentiment cycles move from one extreme of greed to another extreme of fear which takes valuations also to extremes from their long-term averages. At the extreme of fear sentiment (which coincides with dirt-cheap valuations), the risk-reward is highly favorable i.e., higher potential upside with lower potential downside risk.

However, the impending end of the Federal Reserve (Fed) rate-hiking campaign, and the economy’s and corporate America’s resilience, help make the bull case that steers LPL Research toward a neutral, rather than negative, equities view from a tactical assetallocation perspective. At the same time, the resilience of the U.S.

The Strategic and Tactical AssetAllocation Committee (STAAC) made no changes to its recommended assetallocation for August. It is also a major component used to calculate the price-toearnings valuation ratio. We could see a retest of 3.5% over the next few months. All index data from FactSet.

economy to avoid recession, and support above-average valuations. The relationship between inflation and stock valuations is a strong one, as shown in Figure 2 , which meant the market could no longer support price-to-earnings (P/E) ratios over 20 (the same goes for the relationship between interest rates and stock valuations).

Retailer valuations have also taken a hit, as the forward (next 12 months) P/E multiple has contracted ~20% year to date, from ~27x to ~22x currently. Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. All index data from Bloomberg.

Still, as we survey what are better equity valuations, long-awaited income opportunities in the bond market, and a likely less-antagonistic Fed in 2023, there may be emerging reasons to believe that the next year may be more constructive than the last. Assetallocation does not ensure a profit or protect against a loss.

equity market: A comparatively quick interest rate increase counteracts the benefit from stronger economic growth, impairing profitability and valuations. Concern about future economic growth undermines valuations. equity valuations exceed the historical average and the strong dollar poses headwinds to corporate profitability.

The Strategic and Tactical AssetAllocation Committee’s (STAAC) S&P 500 year-end fair value target of 4,000-4,100 is based on a price-to-earnings ratio of 17.5 It is also a major component used to calculate the price-toearnings valuation ratio. Core bonds, as measured by the Bloomberg Aggregate Bond index, were up 3.7%

The Strategic and Tactical AssetAllocation Committee’s (STAAC) S&P 500 year-end fair value target of 4,000-4,100 is based on a price-to-earnings ratio of 17.5 It is also a major component used to calculate the price-toearnings valuation ratio. times the STAAC’s 2023 S&P 500 earnings per share forecast of $230.

The Strategic and Tactical AssetAllocation Committee (STAAC) upgraded its view of duration to neutral. It is also a major component used to calculate the price-toearnings valuation ratio. For a list of descriptions of the indexes referenced in this publication, please visit our website at lplresearch.com/definitions.

The Strategic and Tactical AssetAllocation Committee (STAAC) downgraded its view of emerging market (EM) equities in August. It is also a major component used to calculate the price-toearnings valuation ratio. Core bonds, as measured by the Bloomberg Aggregate Bond index, lost 2.8% All index data from FactSet.

LPL’s Strategic and Tactical AssetAllocation Committee (STAAC) recommends a neutral tactical allocation to equities, with a modest overweight to fixed income funded from cash. Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. All index data from FactSet.

While this latest rally may have outpaced fundamentals in the short term, from a technical analysis perspective, and valuations look full, at the same time, the resilience of the U.S. Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. All index data from FactSet.

We believe that the investment return needed to achieve that objective should be the most important guidepost for a portfolio’s assetallocation. With traditional assets like stocks and bonds at high valuations, the implications for future returns of those assets may be underwhelming. Source: BLOOMBERG. economy.

We believe that the investment return needed to achieve that objective should be the most important guidepost for a portfolio’s assetallocation. With traditional assets like stocks and bonds at high valuations, the implications for future returns of those assets may be underwhelming. Source: BLOOMBERG. economy.

Changes in their assumed rate of return can impact decisions ranging from assetallocation to the spending level that a portfolio can rationally support. Our Investment Solutions Group spends considerable time trying to gauge the long-term outlook for stocks since it is central to assetallocation decisions and recommendations.

Changes in their assumed rate of return can impact decisions ranging from assetallocation to the spending level that a portfolio can rationally support. Our Investment Solutions Group spends considerable time trying to gauge the long-term outlook for stocks since it is central to assetallocation decisions and recommendations.

Please see disclosure at the end of the article for a complete list of indexes and definitions used to represent Japanese and global asset classes in this chart. Given the many unknowns in today’s environment, we believe that a moderately defensive assetallocation that provides ample liquidity is prudent.

Please see disclosure at the end of the article for a complete list of indexes and definitions used to represent Japanese and global asset classes in this chart. Given the many unknowns in today’s environment, we believe that a moderately defensive assetallocation that provides ample liquidity is prudent.

In this article, our head of assetallocation discusses how we are managing trade risk, while still embracing global growth opportunities in our portfolios. Our European investments definitely include a large allocation to multinationals. Tariffs: Bark or Bite? These companies are far less exposed than U.S.

In this article, our head of assetallocation discusses how we are managing trade risk, while still embracing global growth opportunities in our portfolios. Our European investments definitely include a large allocation to multinationals. Tariffs: Bark or Bite? Thu, 05/10/2018 - 11:18.

Defining the question in this way is appealing: it demands a definitive yes-or-no answer. There are many challenges to finding definitive causality between ESG data and financial performance. Risk Factors as Building Blocks for Portfolio Diversification: The Chemistry of AssetAllocation." Podkaminer, E. 2013(1): 1-15.

Defining the question in this way is appealing: it demands a definitive yes-or-no answer. There are many challenges to finding definitive causality between ESG data and financial performance. Risk Factors as Building Blocks for Portfolio Diversification: The Chemistry of AssetAllocation." Podkaminer, E. 2013(1): 1-15.

Investment Perspectives | Corrections jsayo Tue, 03/13/2018 - 12:38 The abrupt stock market downturn in February was “officially” a market correction, according to the conventional definition (a market decline of more than 10%). Deficits are rising in the U.S., Diversification strategies, including exposure to non-U.S.

The abrupt stock market downturn in February was “officially” a market correction, according to the conventional definition (a market decline of more than 10%). The future course of interest rates is probably the greatest single concern for investors today, from both a fundamental and a valuation perspective. Tue, 03/13/2018 - 12:38.

And so in the 1990s, I developed the, the late 1980s, early 1990s, I developed a skillset around valuation, in particular discounted cash flow or residual income type models, along with a couple of peers out of the consulting industry. Definitely 00:07:32 [Speaker Changed] True. 00:07:28 [Speaker Changed] Hey, listen, smart is good.

CHANCELLOR: And look — yeah, but then if you look at the valuation of the market at that time, the market was — the U.S. CHANCELLOR: And look — yeah, but then if you look at the valuation of the market at that time, the market was — the U.S. And that definitely belongs to the Library of Mistakes.

So there’s been a big push for folks to get the appropriate level of assetallocation in a highly diversified, low cost way. But is it fair to say that this year and perhaps last year, you saw a big shift of client cash assets into money markets? And the reality is for a lot of investors, it truly is free money, right?

While we acknowledge that a V-shaped recovery is probably not in the cards and prior valuation targets no longer appear achievable, we remain constructive on equities for the second half, but not complacent. Remember stock valuations are inversely correlated to inflation and interest rates. So a P/E over 20 is probably too rich.

00:01:59 [David Snyderman] I don’t know why I thought I could, but I definitely thought I could at the time and so I wanted to play at the highest level possible. So they’d give individual assetallocation to people and they’d go invest their money. I wanted to play football really at the highest level I could.

Finomial looked at the excess return generated long only factors like momentum, quality, various valuation metrics and I would add covered call fund to this discussion too. The time period is short obviously but the assetallocation appears to work. A few different things for this post. MBXIX is a proxy for FIG's macro sleeve.

EOG is poised to breakout and trades at bargain valuation of about nine times earnings (relative to the S&P at 23 times earnings and a touch under the overall energy sector of 12 times earnings). That said, it loses early in round one simply due to us believing it’s close to full valuation and due for a breather.

I think it’s very hard to say stocks are objectively cheap because all of these valuation metrics have, have become unreliable over the decades as the nature of the stock market has changed. People definitely seem to be happier to give away money now. I did it during the coronavirus collapse in 2020, and I did it again in 2022.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content