This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

By Jake Anderson, CFP ® , Wealth Planner When helping clients begin retirementplanning, the same questions often arise: What should my retirementplan look like? Your lifestyle, goals, family situation, and risk tolerance will give a unique signature to your retirementplan. How much should I be saving?

Financial advisors have a wide range of strategies at their disposal to create financial plans for their clients. And when it comes to retirementplanning, one popular technique is the use of ‘guardrails’, which set an initial monthly withdrawal rate that can be later adjusted as the size of the client’s portfolio changes.

just upended retirementplanning…again. The age when retirees must begin drawing from non-Roth retirement accounts increases to 73 in 2023, then 75 in 2033. Raising the age when withdrawals must begin is great as it gives investors more planning opportunities. The Secure Act 2.0

Decide upon your assetallocation The first step in investing your 401(k) is determining your “assetallocation,” which is simply the mix of stocks, bonds and cash you’ll hold. This mix of assets is the main building block of your portfolio and will primarily determine the risk and return in the account.

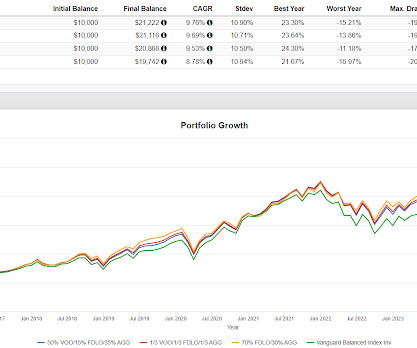

The first example to look at they call Leverage In The Strategic AssetAllocation via this table in the paper. The distribution of results are pretty even. These are easy to model. We'll use Fidelity Low Volatility Factor ETF (FDLO) as a proxy for low volatility for this post. The results here are consistent with the paper.

Your assetallocation is the percentage of your portfolio that you distribute between different asset classes, like stocks and bonds. To rebalance your portfolio, you’ll buy and sell certain investments to realign to your accounts with your desired assetallocation.

The contributions made to the account may be tax-deductible or non-deductible, depending on the individual’s income level and participation in an employer-sponsored retirementplan. The deductibility of contributions depends on the individual’s income level and participation in an employer-sponsored retirementplan.

Take Advantage of RetirementPlans and Matching Contributions. Most employer retirementplans allow you to save on a tax-deferred basis, meaning that contributions into these types of accounts are not considered in calculating your taxable income. . Determine an Appropriate Risk Tolerance for a Longer Time Horizon .

AssetAllocation and Goals. We are big advocates of time based assetallocation. This means you should try to create specific buckets for your portfolio where you’re matching future expenses and liabilities to specific corresponding assets. RetirementPlanning Review your retirement goals and objectives.

There's pending legislation that if passed could be very favorable for retirement savers and retirees in terms of providing more flexibility. Increasing the RMD age to 75 will change quite a few aspects of this part of retirementplanning. Obviously any money not put into an IRA loses the benefit of tax deferred compounding.

In our planning with clients, we like to employ a “pay yourself first” approach, especially as it relates to retirementplanning. You may have been contemplating starting contributions to a retirementplan, or you may have been contributing small amounts and are worried that you are behind in the game.

Understanding the importance of assetallocation is like building a strong financial foundation. It’s all about spreading your investments across different asset classes, like stocks, bonds, and real estate, to manage risk and maximize returns. Financial advisors work alongside clients to create a retirement roadmap.

Long-term goals typically encompass retirementplanning, wealth preservation and estate planning. Your risk tolerance will influence your investment strategy and assetallocation. RetirementPlanningRetirementplanning is a primary focus for many clients.

If you pass away without one, the state will be in charge of distributing the resources and, most likely, give them all to your children, which may have been your plan anyway. A will becomes more important if you have specific instructions regarding assetallocation or would like to donate to a non-profit organization. .

Some specific reasons you may want an estate plan include: . You want to ensure your assets are distributed according to your wishes following your death or incapacity (also referred to as heritage wealth planning ). . The state will distribute your wealth as they see fit, which may not match your wishes.

Long-term goals typically encompass retirementplanning, wealth preservation and estate planning. Your risk tolerance will influence your investment strategy and assetallocation. RetirementPlanningRetirementplanning is a primary focus for many clients.

This really is about having the right assetallocation. A balance needs to be struck between enough growth potential for a 50 or 60 year retirement and enough cash to get through the next 30 month bear market, Bear markets tend to run 18-30 months and while 2022 was shorter than that, a longer one will happen eventually.

The 401(k) retirementplan is one of the most powerful tools. Reaching the age of 50 with over $2 million in your 401(k) is an impressive financial landmark that can provide you with a comfortable retirement if managed wisely. Therefore, careful planning of your withdrawals is essential to minimize your tax liability.

In contrast, the contributions you make to a Roth IRA aren’t tax deductible, but qualified distributions are tax-free. Keep an eye on assetallocation Not all investments are created equally. As you build a portfolio for retirement, it’s important to strike the right balance of risk for your situation.

Similarly, the professional may advise investing in different instruments for goals such as retirementplanning, funding your children’s education expenses, buying a home, or other objectives. What rate of return should I aim for to live a financially secured retirement? account for your retirement income.

Here you do not put all your eggs in one basket, which implies distributing your wealth across different instruments. No matter the assetallocation, keeping a healthy mix of stocks is always advised, especially if you are not nearing retirement anytime soon. you will be able to distribute risk and curtail your losses.

Additionally, traditional IRAs are subjected to the rules of Required Minimum Distributions (RMDs), which implies that you must withdraw a fixed part of your IRA fund from the age of 72 to avoid penalties and taxes. The Roth IRA is exempt from RMDs. Since it is a tax-advantaged account, it can help you save money otherwise paid in tax.

It is crucial to note that tax-loss harvesting is not about avoiding certain asset classes that are not doing well. Instead, it is a strategic approach to maintaining your overall assetallocation and rebalancing goals while taking advantage of tax benefits.

Paraphrasing Cliff Asness, if your retirementplan is thrown into upheaval when the stock market goes down 3%, you might want to rethink your retirementplan. To address the premise of the Yahoo article, this is an assetallocation question. Yes, I am being snarky.

Increasing life expectancies have reshaped our understanding of retirement and financial planning in recent years, and well likely become more concerned about effectively managing financial resources throughout a potentially very long life in the future. 21:38) Overcoming fear of decline requires a shift in mindset and planning.

AssetAllocation and Goals. We are big advocates of time based assetallocation. This means you should try to create specific buckets for your portfolio where youre matching future expenses and liabilities to specific corresponding assets. RetirementPlanning Review your retirement goals and objectives.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content