This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

AssetAllocation: Developing a Long-Term Investment Strategy for Mission-Driven Organizations. When putting a plan in place, we believe it is critical for any mission-driven organization to develop an effective, long-term assetallocation strategy to manage its endowment assets. Tue, 09/06/2022 - 10:30.

However, what is equally critical when it comes to creating a portfolio is assetallocation and selection. Assetallocation aims to balance risk and reward through a portfolio composition of different kinds of assets. If not allocated efficiently, you may become subject to a slew of taxes and other charges.

Because of these differences, stocks and bonds accomplish different things in an assetallocation. while bonds are broken down by duration and sectors (for example government bonds such as municipal or Treasury bonds or corporate bonds, including investment grade or high yield bonds), etc.

It has been my experience when reviewing portfolios that diversification is typically expressed simply as a number of various stocks owned, or owning a handful of asset classes, usually stocks of various sizes and geographies, and bonds of varying maturities.

This included: 2:44 Defined Duration Investing – my new assetallocation process by which I focus on quantifying the time horizons over which to use certain instruments and help match them to a financial plan. More importantly, we learned during Covid that big inflation comes from big government spending, not QE.

Central Governments have given hope of meaningful rate cuts within this year. Equity markets are riding on the expectations of the strong comeback of the NDA-led Government resulting in policy continuity. Consequently, the portfolio allocation should reflect these probabilities depending on the risk profiles.

While Lockheed Martin remains a solid performer with government contracts and steady demand, it lacks the same growth potential as Eli Lilly , which is positioned to benefit from the global healthcare push. This bracket focuses on who benefits most when the Russia-Ukraine war ends and economic rebuilding begins.

The financial markets are especially jittery during periods like this because there is so much uncertainty about the future impact of policy and economic activity. AssetAllocation The Discipline Index is our core benchmark index and has an average duration, as measured in the Defined Duration strategy , of 10 years.

On June 4, the election results showed that the ruling BJP did not achieve a majority on its own, although it remained the largest party in a coalition government. Given the high valuations and fuzzy near-term outlook, our ideal strategy is to stick the assetallocation framework which best suits our risk profile.

Combined with India’s own economic strength and lower interest rates, asset prices—stocks, real estate, gold—could rise even further. The assumption that asset prices will keep rising can quickly be challenged by things like escalating geopolitical tensions, a U.S. What does this mean for India? But so will inflation!

The quantum of money printing jumped massively after Corona-led economic shutdowns. The liquidity support since 2008 and massive stimulus post March 2020 has inflated all the asset prices be it equity, debt, or real estate. US Fed increased its balance sheet size from ~$4-4.5 trillion to ~$8-8.5 trillion in a span of just 2 years.

They can help you better prepare for future economic challenges and prevent you from going into debt. The key to building wealth is diversification and assetallocation. And the ability to adjust your assetallocation as your financial goals change strategically.

3) China (2nd largest economic engine of the world) is struggling and so is Europe. (4) Let’s briefly explore the potential scenarios: (1) Credit Event or Recession: In times of a credit event or economic recession, investors often seek safety, and U.S. investment-grade bonds, including corporate and government bonds.

Understanding Modern Portfolio Construction Understanding the Modern Monetary System Everything you need to know about finance and investing in less than an hour How The Economic Machine Works in 30 Minutes Section 1 – Understanding Money & the Macroeconomy What Is Money? Where Does Money Come From? What Backs the Value of Money?

Increased equity exposure in tactical assetallocation from 62% to 65%. Reduced low duration core bond allocation and increased allocation to small cap equities. Although energy prices came down some, weakening economic data and the lack of a cease-fire in Ukraine offset the modest gas price relief.

Thus, by debasement of the currency, they were able to make more coins which led to higher spending by the Government. Fast forward to the present times, the gold standard is not used by any government now. Whereas, the complete economic recovery is still far away and uncertain in terms of its timing and structure.

The LPL Research Strategic and Tactical AssetAllocation Committee is increasing its recommended interest rate exposure in its tactical allocation from underweight to neutral. As we know from historical precedents, when the Fed aggressively raises rates, economic growth slows or outright contracts, which is the Fed’s goal.

The steps private companies are taking to respond to the current economic backdrop, how different VC subsegments are performing and where we may be in a potential correction in private markets, which tend to lag pubic markets by several months. Inflection Points: 2022 AssetAllocation Perspectives and Outlook Report.

due to expectations of slowing economic growth. The Strategic and Tactical AssetAllocation Committee (STAAC) made no changes to its recommended assetallocation for August. Any economic forecasts set forth may not develop as predicted and are subject to change. We could see a retest of 3.5%

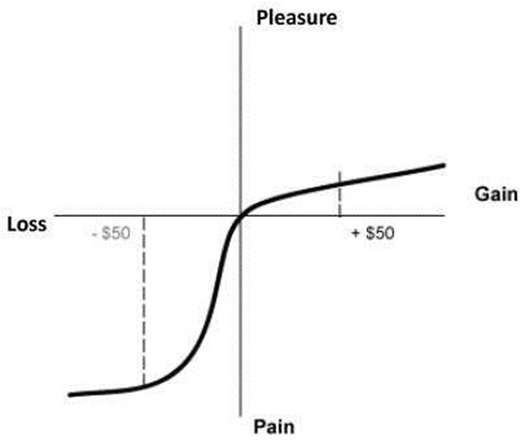

As we stated in “Confronting the Unknown,” our 2018 assetallocation publication, standard deviation is “a helpful shortcut for thinking about risk, but it is not a fully effective proxy.” The “shoestring curve” below depicts these risks for a hypothetical portfolio, assuming various assetallocation targets.

As we stated in “Confronting the Unknown,” our 2018 assetallocation publication, standard deviation is “a helpful shortcut for thinking about risk, but it is not a fully effective proxy.” The “shoestring curve” below depicts these risks for a hypothetical portfolio, assuming various assetallocation targets.

Also, it discusses tax saving options, awareness of unregistered advisers and government schemes. The topics covered are personal finance & investment planning, risk, return & assetallocation, equity markets, analysis, investing, mutual funds and strategies for wealth creation. You can enroll in the course here.

Instead, we got a shockingly fast collapse of a financial institution with over $200 billion in assets, which turned the market’s focus toward the stability of the banking system and what systemic risks banks might be facing. Recent economic data has pointed to continued growth—giving rise to the “no landing” narrative.

While February’s volatility did not materially change our assetallocation views, it reinforced to us the importance of a comprehensive discussion about how we think about risk and how we manage it. Our assetallocation process accounts for a wide range of potential outcomes over the next 18–36 months.

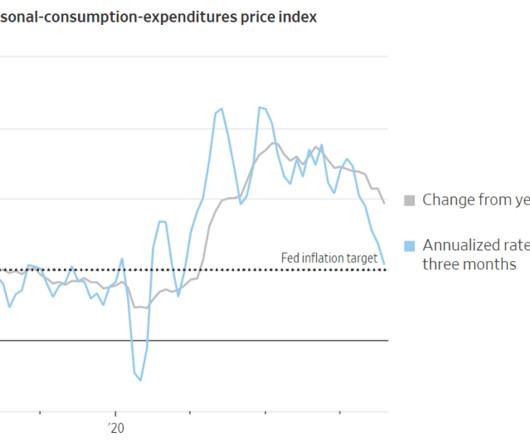

Source: Trading Economics Declining inflation and interest rates explain a lot of investor optimism, but there are additional reasons to be sanguine. There are always plenty of unforeseen issues that could slow or reverse our economic train. a few months ago to 3.9% today (see chart below). Source: Yardeni.com What could go wrong?

Some recent softening in economic data, coupled with signals from the bond market, may be indicating that Fed policymakers’ concerted inflation fight may be closer to the end than the beginning. We should also have slowing corporate earnings growth and greater economic uncertainty to contend with, some formidable seas to navigate.

Economic activity does not stop like an airplane eventually does, but rather the economy will settle into a steady state where growth is consistent with factors such as population and productivity. Perhaps that was not the first time market watchers used the term, but the conversations at the Economic Club of New York were prescient.

Source: Trading Economics As long as consumers continue to hold a job, they will continue spending to buoy economic activity – remember, consumer spending accounts for roughly 70% of our country’s economic activity. rate (see chart below). Under this scenario, you are likely to stay put and not sell your home. for the month.

Strong Defense: The Falling Opportunity Cost of Allocating to Bonds ajackson Tue, 07/24/2018 - 09:25 For years, “defense” in portfolios—i.e., allocations to cash and core fixed income holdings—has meant a willingness to accept extremely low returns. stocks play in most investors’ core equity allocations.

allocations to cash and core fixed income holdings—has meant a willingness to accept extremely low returns. But after many years of economic recovery, we finally have reached a point where defensive allocations once again provide a reasonable yield. stocks play in most investors’ core equity allocations.

As with many things in life, the truth is somewhere between the extremes: While both simulated and real-world data suggest momentum may not be suitable as a driver of long-term assetallocations, we believe momentum considerations can be integrated in a cost-effective way to help inform daily portfolio management decisions.

And so, coming out of school, I studied Economics and Spanish Literature, and I applied to a — a program that actually targeted Liberal Arts majors. You have a background, undergraduate, your economics degree from Notre Dame, but you were dual-major Spanish language and Literature degree, how useful was that in Latin America?

The Manufacturing Renaissance is Here Sonu Varghese, VP and Global Macro Strategist I’ve never seen an economic chart like this, especially one related to factory construction. Sure enough, late last year shelter inflation began to slow and the Fed began to pivot at its final policy committee meeting of the year, which concluded Dec.

The hangover from COVID has created significant supply chain disruptions and widespread economic shortages. Source: Trading Economics. The rising Baker Hughes drilling rig count below reflects the miracle of supply-demand economics operating in full force. Source: Trading Economics. over the next couple of years.

Contrary to the expectation of an economic slowdown in 2023, the year turned out to be full of surprises, mostly positive ones. We maintain our underweight position to equity (check the 3rd page for assetallocation) due to an unfavorable risk-reward ratio.

However, the impending end of the Federal Reserve (Fed) rate-hiking campaign, and the economy’s and corporate America’s resilience, help make the bull case that steers LPL Research toward a neutral, rather than negative, equities view from a tactical assetallocation perspective. Diversification does not protect against market risk.

That’s not suggesting another 2008 is coming, but rather highlights how fast the economic environment can change. Along with the statement, the Committee updated the Summary of Economic Projections (SEP), which is arguably more important than the brief monetary policy statement.

Jeremy called and said, “Would you like to join the assetallocation team?” So he wanted a sort of non-quanty view input into the assetallocation process. And GMO was still sitting on a massive emerging market position in the assetallocation team. All our economic actions are taking place across time.

As you can see from the chart below, there have been no shortage of issues and events to worry about over the last 15 years (2007 – 2022): 2008-2009: Financial Crisis 2010: Flash Crash (electronic trading collapse) 2011: Debt Ceiling – Eurozone Collapse 2012: Greek Debt Crisis – Arab Spring (anti-government protests) 2012: Presidential Elections (..)

The Strategic and Tactical AssetAllocation Committee’s (STAAC) S&P 500 year-end fair value target of 4,000-4,100 is based on a price-to-earnings ratio of 17.5 Any economic forecasts set forth may not develop as predicted and are subject to change. Corporate bonds are considered higher risk than government bonds.

Economic and corporate data support the initial strong reads on holiday retail sales despite the macro headwinds, reinforcing the idea that today’s consumer is in a better position than usual at this point in the business cycle. Any economic forecasts set forth may not develop as predicted and are subject to change.

Keeping our assetallocation and increasing our wealth. I have been doing this for 25 years now and I can tell you that every single person who has made me sell out because of anticipating some event or a market downturn has regretted it in the long run.

Consider this scenario: An economy is shrinking, government debt is ballooning and emigration is eroding the workforce. Yet creditors shrug off signs of decline and cling to public-sector bonds yielding as much as 15%—until the government abruptly drops the pretense of fiscal solidity and labels the debt unpayable. Not Appropriate.

As you can see below, the worst economic impact is forecasted to be felt by Russia (consensus on 2/24/22 of approximately a -1.0% hit to economic growth), more than twice as bad as the -0.2% a rounding error and less than 1% of total global economic activity). knock to growth for the U.S., Source: The Financial Times.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content