This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Not exactly for the Russia-Ukraine event, but for all the possible events that can puncture the bubble in various asset classes that were created on the back of unlimited and cheap liquidity. The runup in any asset class creates a delusion that the rally will be permanent. Well, we were at Truemind Capital.

AssetAllocation: Caution Toward High Dividend Yielding Stocks achen Fri, 10/28/2016 - 11:25 Why Have High Dividend Yielding Sectors Done Well This Year? According to Morningstar, overall assets in dividend-focused ETFs and mutual funds have ballooned to $672.6 billion in assets they held in 2011. Reach for yield.

AssetAllocation: Caution Toward High Dividend Yielding Stocks. According to Morningstar, overall assets in dividend-focused ETFs and mutual funds have ballooned to $672.6 billion in assets they held in 2011. Stretched Valuations. Fri, 10/28/2016 - 11:25. Why Have High Dividend Yielding Sectors Done Well This Year?

CIO Perspectives Webinar, 2022 AssetAllocation Outlook mhannan Fri, 03/18/2022 - 06:42 Markets have been unsteady at the start of 2022, driven by geopolitical tensions, inflation, and concerns about equity valuations. The war in Ukraine is causing even more uncertainty. Rodrigo is now available.

CIO Perspectives Webinar, 2022 AssetAllocation Outlook. Markets have been unsteady at the start of 2022, driven by geopolitical tensions, inflation, and concerns about equity valuations. CIO Perspectives Webinar, 2022 AssetAllocation Outlook . Fri, 03/18/2022 - 06:42. Download transcript. Watch the Video.

I mean, it was an existential event. But in some ways, those events, and we saw it again in March of 2020, we saw it again around where you see these big moments where it draws people together. So you’re Chief Investment officer of Asset and Wealth Management. And then you see some surprise events.

In the meantime, the overnight rate at 5% puts a lot of pressure on credit markets and this increases the probability of an outlier credit event. When you combine this with a very low unemployment rate and high market valuations you tend to see the sort of choppy stock market that we’ve been experiencing in the last few years.

Assetallocation for a year where bonds offer the most attractive returns they have compared to the expected returns for stocks in decades. MORE ON THIS TOPIC 2023 AssetAllocation Perspectives and Outlook We are pleased to share Brown Advisory’s 2023 Outlook. multinationals and aggregate demand.

Anytime I talk about letting markets work for you over the long term and the role that an adequate savings rate plays in financial success, I will usually caveat that with assuming a proper assetallocation. Ten years is a reasonable time period but someone who bought in 2012 based on the previous ten years really got left behind.

Several factors were common between the two markets: robust corporate earnings growth, expected cuts in interest rates and a shift in investor expectations from a valuation-led phase to an earnings-led phase. We continue to hold 7-10% exposure to Southeast Asian markets due to attractive valuations and improving growth prospects.

The recent rally in the market has made the valuations more expensive compared to historical standards. However, heightened valuations do not provide comfort in replicating higher returns of the past in the medium term. However, heightened valuations do not provide comfort in replicating higher returns of the past in the medium term.

Everyone thinks that due to the recent events caused by Coronavirus we are in uncertain times. The emergence of any event has multiple co-dependent factors and nothing gets created out of a vacuum. The investors who do poorly are those who are always very sure of the future events. I believe we are always in uncertain times.

Increased equity exposure in tactical assetallocation from 62% to 65%. Reduced low duration core bond allocation and increased allocation to small cap equities. The Strategic and Tactical AssetAllocation Committee (STAAC) changed its recommended assetallocation for July, shifting from core bonds to small cap equities.

EUROPEAN RE-ENTRY: Why We Are Shifting Portfolios Toward European Stocks achen Thu, 06/01/2017 - 02:47 Assetallocation—at least for us—is an exercise in nuance. We move slowly and carefully when it comes to shifting our portfolios away from one asset class or region and toward another. is not particularly notable.

Assetallocation—at least for us—is an exercise in nuance. We move slowly and carefully when it comes to shifting our portfolios away from one asset class or region and toward another. EUROPEAN RE-ENTRY: Why We Are Shifting Portfolios Toward European Stocks. Thu, 06/01/2017 - 02:47. is not particularly notable.

Instead, we got a shockingly fast collapse of a financial institution with over $200 billion in assets, which turned the market’s focus toward the stability of the banking system and what systemic risks banks might be facing. But valuations strongly favor value over growth. The S&P 600 small cap index has returned about 1.5%

The Strategic and Tactical AssetAllocation Committee (STAAC) made no changes to its recommended assetallocation for August. This strategy involves significant risk as events may not occur as planned and disruptions to a planned merger may result in significant loss to a hedged position. over the next few months.

And so in the 1990s, I developed the, the late 1980s, early 1990s, I developed a skillset around valuation, in particular discounted cash flow or residual income type models, along with a couple of peers out of the consulting industry. So I met him once briefly, I think it was on his, at his apartment at Park Avenue for some event.

But the drop in valuations experienced at year’s end, alongside higher bond yields, offer a foundation for better long-term return expectations across most asset classes. This is also a fitting moment to review the intersection of risk and valuation. Entering 2019, we face rising economic, political and market risks.

IBM loses to QCOM based on valuation. Obviously this rattled a lot of nerves and the way we see it is that it won’t be a 2008 “Lehman” type event, however there will be other casualties or at least some banks that get major pressure. Watch for those that have even worse financials and balance sheets than SVB did.

While February’s volatility did not materially change our assetallocation views, it reinforced to us the importance of a comprehensive discussion about how we think about risk and how we manage it. Our assetallocation process accounts for a wide range of potential outcomes over the next 18–36 months.

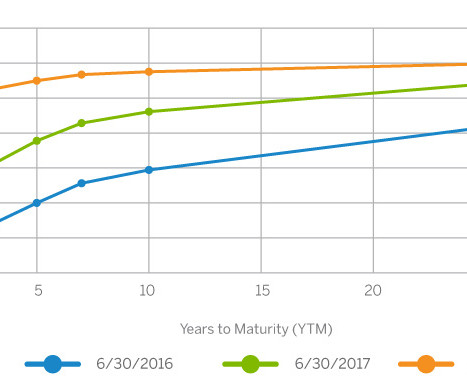

As we stated in “Confronting the Unknown,” our 2018 assetallocation publication, standard deviation is “a helpful shortcut for thinking about risk, but it is not a fully effective proxy.” The “shoestring curve” below depicts these risks for a hypothetical portfolio, assuming various assetallocation targets.

As we stated in “Confronting the Unknown,” our 2018 assetallocation publication, standard deviation is “a helpful shortcut for thinking about risk, but it is not a fully effective proxy.” The “shoestring curve” below depicts these risks for a hypothetical portfolio, assuming various assetallocation targets.

But beyond the economic cycle’s age, several factors suggest that a more defensive mindset is worth considering: Valuations are elevated. Robust Q1 2018 earnings growth improved the valuation picture for U.S. It is worth noting that valuations are more reasonable in developed international and emerging markets; however, U.S.

But beyond the economic cycle’s age, several factors suggest that a more defensive mindset is worth considering: Valuations are elevated. Robust Q1 2018 earnings growth improved the valuation picture for U.S. It is worth noting that valuations are more reasonable in developed international and emerging markets; however, U.S.

Alternatively, nonprofits can boost potential portfolio returns, which often means tolerating more risk and illiquidity, through a recalibration of assetallocation— the single biggest driver of long-term gains. Reassess assetallocation. Callan estimated that a portfolio in 2005 could achieve a 7.5% large-cap strategies.

In good times i.e. when the market valuations are usually very high, everyone agrees to the logic of buying low and selling high. Not understanding the role & importance of tactical assetallocation (overweight debt in euphoric times and overweight equity in a time of acute pessimism) in creating superior returns over the long term.

These items are not static, and can change over time, therefore it’s important to revisit your assetallocation periodically as financial circumstances and life events change your objectives. Short-term news cycle headlines shouldn’t drive portfolio decision-making, but rather your personal objectives, goals, and risk tolerance.

The Strategic and Tactical AssetAllocation Committee’s (STAAC) S&P 500 year-end fair value target of 4,000-4,100 is based on a price-to-earnings ratio of 17.5 This strategy involves significant risk as events may not occur as planned and disruptions to a planned merger may result in significant loss to a hedged position.

The Strategic and Tactical AssetAllocation Committee’s (STAAC) S&P 500 year-end fair value target of 4,000-4,100 is based on a price-to-earnings ratio of 17.5 This strategy involves significant risk as events may not occur as planned and disruptions to a planned merger may result in significant loss to a hedged position.

The Strategic and Tactical AssetAllocation Committee (STAAC) upgraded its view of duration to neutral. This strategy involves significant risk as events may not occur as planned and disruptions to a planned merger may result in significant loss to a hedged position.

The Strategic and Tactical AssetAllocation Committee (STAAC) downgraded its view of emerging market (EM) equities in August. This strategy involves significant risk as events may not occur as planned and disruptions to a planned merger may result in significant loss to a hedged position.

equity market: A comparatively quick interest rate increase counteracts the benefit from stronger economic growth, impairing profitability and valuations. Concern about future economic growth undermines valuations. equity valuations exceed the historical average and the strong dollar poses headwinds to corporate profitability.

We tend to be strategic rather than tactical in our approach to investing, but a combination of recent fundamental developments and valuation changes has caused us to add a note of caution in conversations with clients and in the management of their portfolios. Concentration: Much of the U.S. Opportunity to Rebalance?

We tend to be strategic rather than tactical in our approach to investing, but a combination of recent fundamental developments and valuation changes has caused us to add a note of caution in conversations with clients and in the management of their portfolios. Concentration: Much of the U.S. Opportunity to Rebalance? Risks in Bonds.

When macro conditions are uncertain, a banker’s approach to valuation can help. David, a former investment banker, has always brought a banker’s mentality to valuing smaller companies by breaking down their assets and operations into components that can be more accurately assessed.

In Engines That Move Markets, a 2002 book about the cycles of technology investing, Alasdair Nairn defines “bubbles” as periods when investors appear to suspend rational valuation, much as they had during the dotcom craze shortly before the book was published. Unsurprisingly, as volume has increased, so have valuations. Possible Signs.

So they’d give individual assetallocation to people and they’d go invest their money. What happened over the last year and a half or so is rates went up and valuations went down. Tell us about the opportunities that came up from those events. And first was, we’re gonna have a culture of collaboration.

The securities should have diversified and specific streams of revenue and solid legal protections that give creditors senior status in the event of default. By Taylor Graff, CFA, AssetAllocation Analyst. These views are not intended to be a forecast of future events or a guarantee of future results.

This helps to meet your immediate needs and instill discipline in a longterm context, averting excessive spending when valuations are rising. By Taylor Graff, CFA, AssetAllocation Analyst. These views are not intended to be a forecast of future events or a guarantee of future results.

Sometimes a major event makes it clear that an immediate course correction is needed. As head of assetallocation research in our Investment Solutions Group, he is responsible for analyzing the relative attractiveness of various asset classes and investment strategies. GDP than it was 100 years ago.

Sometimes a major event makes it clear that an immediate course correction is needed. As head of assetallocation research in our Investment Solutions Group, he is responsible for analyzing the relative attractiveness of various asset classes and investment strategies. Tue, 08/06/2019 - 08:46. Little River Band, 1979.

We believe that the investment return needed to achieve that objective should be the most important guidepost for a portfolio’s assetallocation. With traditional assets like stocks and bonds at high valuations, the implications for future returns of those assets may be underwhelming. Source: BLOOMBERG.

We believe that the investment return needed to achieve that objective should be the most important guidepost for a portfolio’s assetallocation. With traditional assets like stocks and bonds at high valuations, the implications for future returns of those assets may be underwhelming. Source: BLOOMBERG.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content