This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

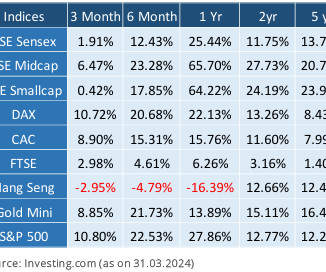

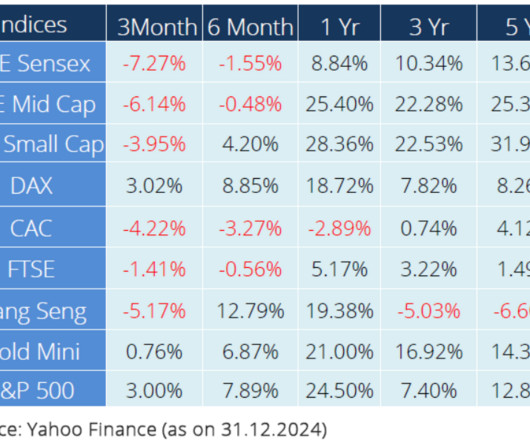

Indian equity benchmark BSE Sensex went up by only 2% due to already stretched equity valuations. Mid & small cap indices witnessed some correction after the SEBI expressed concerns regarding frothy valuations and nudged mutual funds to restrict inflows. European indices also saw decent returns.

Like the circle of life, good times are followed by bad times, and bad times are followed by good times, stock markets also go through cycles of excessive greed/optimism to excessive fear/pessimism. For the sustainable long-term progress of financialmarkets, corrections are healthy and useful.

Like the circle of life, good times are followed by bad times, and bad times are followed by good times, stock markets also go through cycles of excessive greed/optimism to excessive fear/pessimism. For the sustainable long-term progress of financialmarkets, corrections are healthy and useful.

Several factors were common between the two markets: robust corporate earnings growth, expected cuts in interest rates and a shift in investor expectations from a valuation-led phase to an earnings-led phase. Additionally, cooling inflation supported the equity markets. However, this quarter has been different.

India being highlighted as a beneficiary from the shift in Global equations along with the expected highest economic growth among major economies has attracted strong flows from the FIIs lifting overall market sentiments. The recent rally in the market has made the valuations more expensive compared to historical standards.

Higher valuation of Indian markets compared to Global peers along with negligible earnings growth also didn’t help. One should not be over-allocated to equity (check the 3rd page for assetallocation) at the current levels and any exposure should primarily be towards large cap-oriented value portfolios against growth stocks.

That’s exactly what we’ve seen in India’s financialmarkets in the quarter ending September 2024. Here is what’s happening currently- Stock markets are rising Bond Prices are increasing / Bond Yields are falling Gold is trending upwards Real Estate Prices are inching upwards ALL KEY ASSET PRICES ARE GOING NORTHWARDS!

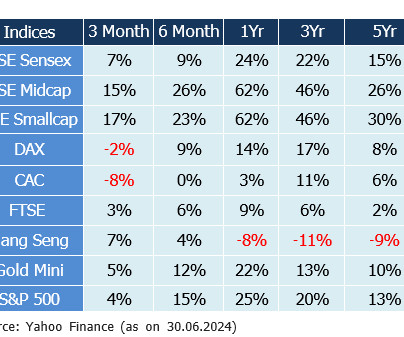

Some of the fund managers continued discouraging flows in Mid & Small Cap stocks by either sounding cautious, dropping coverage, or stopping the inflows owing to frothy valuations in the space. We maintain our underweight position to equity (check the 3rd page for assetallocation) due to an unfavorable risk-reward ratio.

In the meantime, the overnight rate at 5% puts a lot of pressure on credit markets and this increases the probability of an outlier credit event. When you combine this with a very low unemployment rate and high marketvaluations you tend to see the sort of choppy stock market that we’ve been experiencing in the last few years.

September 2016 Insights on Markets and Investments achen Mon, 09/12/2016 - 01:00 In this issue: Investors Facing Rising Risks Need Solid Defense, Savvy Offense Increasing political and economic risk during the past year has widened the range of possible positive and negative scenarios for financialmarkets.

In this issue: Investors Facing Rising Risks Need Solid Defense, Savvy Offense Increasing political and economic risk during the past year has widened the range of possible positive and negative scenarios for financialmarkets. Equities Private Credit Outshines Many High-Valuation Stocks, Bonds. Strategic Advisory.

Financial services became the backbone of India’s growth. Key indicators like banked population and market capitalization improved. Indian households traditionally invested most savings in physical assets. However, financialassetallocation increased recently. lakh crore and ₹3.1 Comment below.

Alternatively, nonprofits can boost potential portfolio returns, which often means tolerating more risk and illiquidity, through a recalibration of assetallocation— the single biggest driver of long-term gains. Reassess assetallocation. Consider changes to portfolio construction. and Germany—have fueled volatility.

No central bank has ever wound down such massive stimulus, so the potential impact on the economy and financialmarkets is not clear. The easing helped stabilize financialmarkets, reduced the risk of deflation and resuscitated the economy and job growth. Concern about future economic growth undermines valuations.

And so in the 1990s, I developed the, the late 1980s, early 1990s, I developed a skillset around valuation, in particular discounted cash flow or residual income type models, along with a couple of peers out of the consulting industry. We ended up buying, this is one of the wonderful things about financialmarkets and degrees of completeness.

They certainly could, but valuations remain attractive given where interest rates currently stand. If interest rates rise dramatically, all else equal, then that will be challenging for all asset pricing. Source: Yardeni.com. Could the headwinds previously described cause prices to go lower? www.Sidoxia.com. Slome, CFA, CFP®.

This helps to meet your immediate needs and instill discipline in a longterm context, averting excessive spending when valuations are rising. There are three fundamental variables to monitor in portfolio management: market performance, changes in tax policy and a portfolio’s rate of drawdown (expenses and spending).

It was 16 hour days and it was six or seven days a week, but you really got to learn the financialmarkets there. So they’d give individual assetallocation to people and they’d go invest their money. What happened over the last year and a half or so is rates went up and valuations went down.

THE “JAPANIFICATION” QUESTION Investors who were active in the late 1980s will recall that asset prices in Japan reached extreme levels as money poured into the country from all over the world, propelled by extraordinary economic growth. financialmarkets, to be a global leader for more than a century.

Investors who were active in the late 1980s will recall that asset prices in Japan reached extreme levels as money poured into the country from all over the world, propelled by extraordinary economic growth. financialmarkets, to be a global leader for more than a century. PORTFOLIO IMPLICATIONS. economy, and by extension U.S.

As I have discussed numerous times in the past, money goes where it is treated best, which is why interest rates, cash flows, and valuations play such a key role in ultimately determining long-term values across all asset classes. This notion rings especially true when it comes to finance and investing.

Consider how we defined investment risk in our 2018 assetallocation publication, Confronting the Unknown: “The probability that a portfolio will not meet an investor’s needs.” ILLIQUIDITY IMPACTS These dynamics have dramatically shifted the liquidity landscape across financialmarkets.

Consider how we defined investment risk in our 2018 assetallocation publication, Confronting the Unknown: “The probability that a portfolio will not meet an investor’s needs.” These dynamics have dramatically shifted the liquidity landscape across financialmarkets. Source: BLOOMBERG. . ILLIQUIDITY IMPACTS.

And so we go back to the basics of what our job should be, risk underwriting, risk assessment, asset prices are different from assetvaluation. I mean the valuation is the future cash flow discounted at a risk-free rate plus a risk premium. RITHOLTZ: (LAUGHTER) CHABRAN: And find a reason why they would allocate there.

The positive global perception and growing domestic inflows ensure that the premium valuations of the Indian market are maintained. Some of the institutions dropped coverage or discouraged investing in Mid & Small Cap stocks owing to very expensive valuations boosted primarily by retail participation lured by past returns.

As we write this letter, financialmarkets are grappling with plenty of controversy and uncertainty, from the aftershocks of the dramatic fall in oil prices, to the potential impact of a British exit from the EU, to the implications of the pending U.S. Secure valuation discounts by obtaining necessary valuations early in the year. .

I mean, he was essentially market timer, for a lack of a a better word. He wasn’t tactical assetallocator. 00:11:43 [Speaker Changed] And one of the more rare successful market times 00:11:47 [Speaker Changed] Unbelievably successful. And I had a professor give me a little sort of hint. It wasn’t the case.

Overall, we maintain our underweight position to equity (check the assetallocation below) on the back of pricey markets- the current PE ratio of 22.7x Most of our portfolios include a small allocation to Chinese markets. is still above its historical averages. Do read our blog here to know more!

And one of the worst performing factors has been valuation. So we’re now in an environment where all the 45-year-old portfolio managers out there have been, have worked their entire careers in these momentum fueled markets, and they’ve been trained to believe that valuation doesn’t matter.

And so I worked a lot on the assetallocation side. Again, as I said, we’ve worked in assetallocation. But definitely markets are cyclical in nature. And you know, it’s the same thing when valuation gets outta control too. Valuations are tight, they’re tight for a reason.

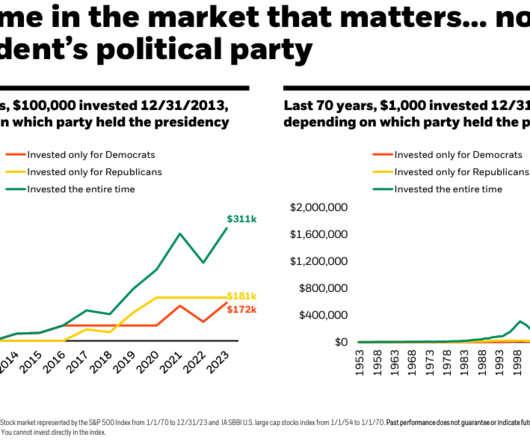

For example, the September 11th terrorist attacks and the 2008 Great Financial Crisis occurred under President G.W. President Obama’s term, starting in 2009, began when stock marketvaluations were near the bottom and as is well documented now, the stock market went on to its longest bull market in history.

For example, the September 11th terrorist attacks and the 2008 Great Financial Crisis occurred under President G.W. President Obama’s term, starting in 2009, began when stock marketvaluations were near the bottom and as is well documented now, the stock market went on to its longest bull market in history.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content