This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

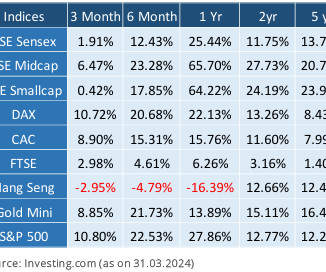

Indian equity benchmark BSE Sensex went up by only 2% due to already stretched equity valuations. Mid & small cap indices witnessed some correction after the SEBI expressed concerns regarding frothy valuations and nudged mutual funds to restrict inflows. European indices also saw decent returns.

AssetAllocation: Caution Toward High Dividend Yielding Stocks achen Fri, 10/28/2016 - 11:25 Why Have High Dividend Yielding Sectors Done Well This Year? According to Morningstar, overall assets in dividend-focused ETFs and mutual funds have ballooned to $672.6 billion in assets they held in 2011. Reach for yield.

AssetAllocation: Caution Toward High Dividend Yielding Stocks. According to Morningstar, overall assets in dividend-focused ETFs and mutual funds have ballooned to $672.6 billion in assets they held in 2011. Stretched Valuations. Fri, 10/28/2016 - 11:25. Why Have High Dividend Yielding Sectors Done Well This Year?

CIO Perspectives Webinar, 2022 AssetAllocation Outlook mhannan Fri, 03/18/2022 - 06:42 Markets have been unsteady at the start of 2022, driven by geopolitical tensions, inflation, and concerns about equity valuations. The war in Ukraine is causing even more uncertainty. Rodrigo is now available.

CIO Perspectives Webinar, 2022 AssetAllocation Outlook. Markets have been unsteady at the start of 2022, driven by geopolitical tensions, inflation, and concerns about equity valuations. CIO Perspectives Webinar, 2022 AssetAllocation Outlook . Fri, 03/18/2022 - 06:42. Download transcript. Watch the Video.

And again, I ended up in the financialservices audit practice at KPMG. So what we find, and then of course we have a multi-asset solutions business where we talk to clients about the entirety of their portfolio, their strategic assetallocation models. So we start with a strategic assetallocation.

Financialservices became the backbone of India’s growth. Indian households traditionally invested most savings in physical assets. However, financialassetallocation increased recently. This trend is expected to continue due to better financial literacy, a focus on inclusion, and market confidence.

Watch for renewed demand for health care, communication services, retail, and financialservices. Higher interest rates are challenging stock valuations and perhaps pushing the gains further out in 2023, but we still see solid potential for double-digit returns for stocks this year. All index data from FactSet.

We tend to be strategic rather than tactical in our approach to investing, but a combination of recent fundamental developments and valuation changes has caused us to add a note of caution in conversations with clients and in the management of their portfolios. Concentration: Much of the U.S.

We tend to be strategic rather than tactical in our approach to investing, but a combination of recent fundamental developments and valuation changes has caused us to add a note of caution in conversations with clients and in the management of their portfolios. Concentration: Much of the U.S. Risks in Bonds.

So I saw many companies then taxed and financialservices. So they’d give individual assetallocation to people and they’d go invest their money. What happened over the last year and a half or so is rates went up and valuations went down. And first was, we’re gonna have a culture of collaboration.

We believe that the investment return needed to achieve that objective should be the most important guidepost for a portfolio’s assetallocation. These can include aspects like size, time horizon, expertise, financial situation and governance. We believe this is fundamental to building a diversified assetallocation.

We believe that the investment return needed to achieve that objective should be the most important guidepost for a portfolio’s assetallocation. These can include aspects like size, time horizon, expertise, financial situation and governance. We believe this is fundamental to building a diversified assetallocation.

Changes in their assumed rate of return can impact decisions ranging from assetallocation to the spending level that a portfolio can rationally support. Our Investment Solutions Group spends considerable time trying to gauge the long-term outlook for stocks since it is central to assetallocation decisions and recommendations.

Changes in their assumed rate of return can impact decisions ranging from assetallocation to the spending level that a portfolio can rationally support. Our Investment Solutions Group spends considerable time trying to gauge the long-term outlook for stocks since it is central to assetallocation decisions and recommendations.

Equity returns are less predictable, but we believe they are more likely than not to be lower going forward compared to the post-crisis period, given the outlook for modest GDP growth around the world alongside today’s elevated valuations. A core allocation to high-grade bonds can play a similar role.

Equity returns are less predictable, but we believe they are more likely than not to be lower going forward compared to the post-crisis period, given the outlook for modest GDP growth around the world alongside today’s elevated valuations. A core allocation to high-grade bonds can play a similar role.

In this article, our head of assetallocation discusses how we are managing trade risk, while still embracing global growth opportunities in our portfolios. Criteria evaluated include market capitalization, financial viability, liquidity, public float, sector representation and corporate structure. Tariffs: Bark or Bite?

In this article, our head of assetallocation discusses how we are managing trade risk, while still embracing global growth opportunities in our portfolios. Criteria evaluated include market capitalization, financial viability, liquidity, public float, sector representation and corporate structure. Tariffs: Bark or Bite?

On the upside, active managers are often reluctant to overweight or “chase” the leading stocks in the market because those stocks typically sell at premium valuations. It underperformed primarily during very strong markets, as might be expected given its discipline with regard to valuations. Reasons for this tendency are varied.

On the upside, active managers are often reluctant to overweight or “chase” the leading stocks in the market because those stocks typically sell at premium valuations. It underperformed primarily during very strong markets, as might be expected given its discipline with regard to valuations. Reasons for this tendency are varied.

The future course of interest rates is probably the greatest single concern for investors today, from both a fundamental and a valuation perspective. Without making a call on the near-term direction of the markets, we continue to stress the importance of maintaining liquidity and safety as a critical component of assetallocation.

The future course of interest rates is probably the greatest single concern for investors today, from both a fundamental and a valuation perspective. Without making a call on the near-term direction of the markets, we continue to stress the importance of maintaining liquidity and safety as a critical component of assetallocation.

Consider how we defined investment risk in our 2018 assetallocation publication, Confronting the Unknown: “The probability that a portfolio will not meet an investor’s needs.” Criteria evaluated include: market capitalization, financial viability, liquidity, public float, sector representation, and corporate structure.

Consider how we defined investment risk in our 2018 assetallocation publication, Confronting the Unknown: “The probability that a portfolio will not meet an investor’s needs.” Criteria evaluated include: market capitalization, financial viability, liquidity, public float, sector representation, and corporate structure.

You know, that’s one thing in Europe where London was, I actually think, still remains the one place where you want to get exposure when you join financialservices. And so we go back to the basics of what our job should be, risk underwriting, risk assessment, asset prices are different from assetvaluation.

While February’s volatility did not materially change our assetallocation views, it reinforced to us the importance of a comprehensive discussion about how we think about risk and how we manage it. Our assetallocation process accounts for a wide range of potential outcomes over the next 18–36 months.

But the drop in valuations experienced at year’s end, alongside higher bond yields, offer a foundation for better long-term return expectations across most asset classes. This is also a fitting moment to review the intersection of risk and valuation. Entering 2019, we face rising economic, political and market risks. In non-U.S.

EUROPEAN RE-ENTRY: Why We Are Shifting Portfolios Toward European Stocks achen Thu, 06/01/2017 - 02:47 Assetallocation—at least for us—is an exercise in nuance. We move slowly and carefully when it comes to shifting our portfolios away from one asset class or region and toward another. is not particularly notable.

Assetallocation—at least for us—is an exercise in nuance. We move slowly and carefully when it comes to shifting our portfolios away from one asset class or region and toward another. EUROPEAN RE-ENTRY: Why We Are Shifting Portfolios Toward European Stocks. Thu, 06/01/2017 - 02:47. is not particularly notable. is much clearer.

As Morgan Housel has cautioned : “The business model of the majority of financialservices companies relies on exploiting the fears, emotions, and lack of intelligence of customers. 2014 : “What concerns us beyond valuations is the full ensemble of overvalued, overbought, overbullish conditions.”

It is a financialservices hub. It’s certainly not New York City, but it’s, it’s definitely the top two or three in terms of large financialservices. Mike Freno : It’s become, it’s become an asset for us to be located there for, for sure. So it’s been, it’s been great.

Outlook for 2017 | Balance in an Uncertain Time achen Fri, 02/03/2017 - 14:19 With that said, we present this discussion of our assetallocation approach and our current portfolio stance as we begin the year. Provide our assetallocation perspective as it stands at the beginning of 2017—also based on a longer-term view.

With that said, we present this discussion of our assetallocation approach and our current portfolio stance as we begin the year. In writing this report, we set out to accomplish two goals: Provide a window into our assetallocation philosophy and process, which emphasize a long-term view. Fri, 02/03/2017 - 14:19.

And meanwhile, I was doing, you know, I was working at this financialservices company and I was really interested in what they were doing. And one of the worst performing factors has been valuation. And I think that’s wrong because valuation does matter. Eventually it, 00:30:12 [Speaker Changed] It matters.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content