This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

She also leads the firm’s environmental, social and governance research. We discuss what her valuation models are showing: “I think that where we are today is actually a reasonably healthy point for equities…I don’t worry as much about big cap companies that everybody is tracking and watching and monitoring.”

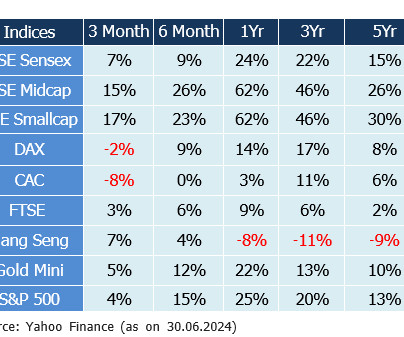

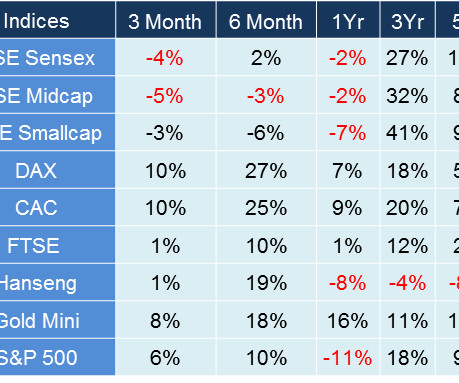

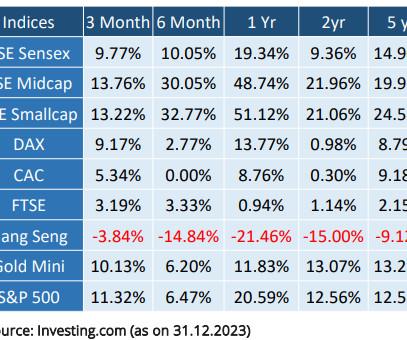

Central Governments have given hope of meaningful rate cuts within this year. Equity markets are riding on the expectations of the strong comeback of the NDA-led Government resulting in policy continuity. Indian equity benchmark BSE Sensex went up by only 2% due to already stretched equity valuations.

CIO Perspectives Webinar, 2022 AssetAllocation Outlook mhannan Fri, 03/18/2022 - 06:42 Markets have been unsteady at the start of 2022, driven by geopolitical tensions, inflation, and concerns about equity valuations. The war in Ukraine is causing even more uncertainty. Rodrigo is now available.

CIO Perspectives Webinar, 2022 AssetAllocation Outlook. Markets have been unsteady at the start of 2022, driven by geopolitical tensions, inflation, and concerns about equity valuations. CIO Perspectives Webinar, 2022 AssetAllocation Outlook . Fri, 03/18/2022 - 06:42. Download transcript. Watch the Video.

AssetAllocation: Caution Toward High Dividend Yielding Stocks achen Fri, 10/28/2016 - 11:25 Why Have High Dividend Yielding Sectors Done Well This Year? According to Morningstar, overall assets in dividend-focused ETFs and mutual funds have ballooned to $672.6 billion in assets they held in 2011. Reach for yield.

AssetAllocation: Caution Toward High Dividend Yielding Stocks. According to Morningstar, overall assets in dividend-focused ETFs and mutual funds have ballooned to $672.6 billion in assets they held in 2011. Stretched Valuations. Fri, 10/28/2016 - 11:25. Why Have High Dividend Yielding Sectors Done Well This Year?

A client said – I understand market valuations are expensive but it doesn’t seem that it will correct much. The fundamental driver of market peaks and exorbitant valuations is the perception that there is nothing to worry about – there is no investment risk. Certainly not if you are sticking to your assetallocation.

On June 4, the election results showed that the ruling BJP did not achieve a majority on its own, although it remained the largest party in a coalition government. Given the high valuations and fuzzy near-term outlook, our ideal strategy is to stick the assetallocation framework which best suits our risk profile.

There could be the following three broader outcomes on 4th June: Outcome #1 NDA forming the government with BJP winning the full majority on its own: This is the most probabilistic scenario as per the investment community which means that this scenario is already discounted in the stock prices. This outcome is perceived as less probable.

To ensure the stability of the Government and keep its popularity maintained, the policymakers are forced to work out solutions to curb inflation and inflationary expectations. This strategy based on possibilities is called tactical assetallocation which always leads to higher portfolio returns at a given level of risk.

Thankfully, the Governments intervened to avoid major spillover effects on the overall economy. Higher valuation of Indian markets compared to Global peers along with negligible earnings growth also didn’t help. The rising risk of Global financial uncertainties affected Indian markets as well. The Adani saga also aggravated volatility.

Thus, by debasement of the currency, they were able to make more coins which led to higher spending by the Government. Fast forward to the present times, the gold standard is not used by any government now. This has resulted in skyrocketing valuations of the stock markets. Britain abolished the gold standard in 1931.

The assumption that asset prices will keep rising can quickly be challenged by things like escalating geopolitical tensions, a U.S. This is where our disciplined dynamic assetallocation approach will really shine, keeping us steady through any rough waters ahead. The Sep’24 ending PE Ratio of 24.8x

I recall one particularly glaring moment during 2009 when AIG became mostly owned by the US government and failed to meet S&P liquidity requirements, but they just ignored it. It forced me to think in a multi-temporal sense which has completely changed how I think about assetallocation.

CHANCELLOR: And look — yeah, but then if you look at the valuation of the market at that time, the market was — the U.S. CHANCELLOR: And look — yeah, but then if you look at the valuation of the market at that time, the market was — the U.S. CHANCELLOR: Well, he sort of — yeah, he thought about it.

Instead, we got a shockingly fast collapse of a financial institution with over $200 billion in assets, which turned the market’s focus toward the stability of the banking system and what systemic risks banks might be facing. But valuations strongly favor value over growth. The S&P 600 small cap index has returned about 1.5%

Increased equity exposure in tactical assetallocation from 62% to 65%. Reduced low duration core bond allocation and increased allocation to small cap equities. The Strategic and Tactical AssetAllocation Committee (STAAC) changed its recommended assetallocation for July, shifting from core bonds to small cap equities.

While February’s volatility did not materially change our assetallocation views, it reinforced to us the importance of a comprehensive discussion about how we think about risk and how we manage it. Our assetallocation process accounts for a wide range of potential outcomes over the next 18–36 months.

Historically, this bracket has been dominated by the tech sector, but after years of outsized gains, big tech valuations are stretched. While Lockheed Martin remains a solid performer with government contracts and steady demand, it lacks the same growth potential as Eli Lilly , which is positioned to benefit from the global healthcare push.

IBM loses to QCOM based on valuation. Sticking back to the balancing theme of quality businesses, great valuations, meshed with the reward of a dividend, you get Ford yielding 4.62% and Conoco only at 2.16% but trading for a bargain P/E of 7. times and return on equity (ROE) of 9%.

The LPL Research Strategic and Tactical AssetAllocation Committee is increasing its recommended interest rate exposure in its tactical allocation from underweight to neutral. Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. All index data from FactSet.

As we stated in “Confronting the Unknown,” our 2018 assetallocation publication, standard deviation is “a helpful shortcut for thinking about risk, but it is not a fully effective proxy.” The “shoestring curve” below depicts these risks for a hypothetical portfolio, assuming various assetallocation targets.

As we stated in “Confronting the Unknown,” our 2018 assetallocation publication, standard deviation is “a helpful shortcut for thinking about risk, but it is not a fully effective proxy.” The “shoestring curve” below depicts these risks for a hypothetical portfolio, assuming various assetallocation targets.

The Strategic and Tactical AssetAllocation Committee (STAAC) made no changes to its recommended assetallocation for August. Corporate bonds are considered higher risk than government bonds. It is also a major component used to calculate the price-toearnings valuation ratio. We could see a retest of 3.5%

Despite reducing overall liquidity and increasing interest rates by the FED, the widening of the government fiscal deficit, a tight labor market, rising wages, receding inflation, and positive wealth effects helped maintain abundant liquidity and boosted sentiments.

Later in the year, markets became anxious about other topics, such as a potential economic slowdown, a new level of dysfunction in Washington (including unusual executive challenges to the Fed's independence and an extended partial government shutdown), and escalating trade disputes between the U.S.

But beyond the economic cycle’s age, several factors suggest that a more defensive mindset is worth considering: Valuations are elevated. Robust Q1 2018 earnings growth improved the valuation picture for U.S. It is worth noting that valuations are more reasonable in developed international and emerging markets; however, U.S.

But beyond the economic cycle’s age, several factors suggest that a more defensive mindset is worth considering: Valuations are elevated. Robust Q1 2018 earnings growth improved the valuation picture for U.S. It is worth noting that valuations are more reasonable in developed international and emerging markets; however, U.S.

However, the impending end of the Federal Reserve (Fed) rate-hiking campaign, and the economy’s and corporate America’s resilience, help make the bull case that steers LPL Research toward a neutral, rather than negative, equities view from a tactical assetallocation perspective. At the same time, the resilience of the U.S.

economy to avoid recession, and support above-average valuations. The relationship between inflation and stock valuations is a strong one, as shown in Figure 2 , which meant the market could no longer support price-to-earnings (P/E) ratios over 20 (the same goes for the relationship between interest rates and stock valuations).

equity market: A comparatively quick interest rate increase counteracts the benefit from stronger economic growth, impairing profitability and valuations. Concern about future economic growth undermines valuations. equity valuations exceed the historical average and the strong dollar poses headwinds to corporate profitability.

Industry data already show declining rent prices, so it’s just a matter of time before the official government statistics reflect that easing. Higher interest rates are challenging stock valuations and perhaps pushing the gains further out in 2023, but we still see solid potential for double-digit returns for stocks this year.

The Strategic and Tactical AssetAllocation Committee’s (STAAC) S&P 500 year-end fair value target of 4,000-4,100 is based on a price-to-earnings ratio of 17.5 Corporate bonds are considered higher risk than government bonds. It is also a major component used to calculate the price-toearnings valuation ratio.

As with many things in life, the truth is somewhere between the extremes: While both simulated and real-world data suggest momentum may not be suitable as a driver of long-term assetallocations, we believe momentum considerations can be integrated in a cost-effective way to help inform daily portfolio management decisions.

One equity market debate discussed frequently in the LPL Research Strategic & Tactical AssetAllocation Committee (STAAC) is the growth vs. value style reversal experienced the past 12 months. Increasing the discount rate, which lowers the present value of future cash flows, and company valuations.

Even our government is now attempting to increase supply by releasing up to 180 million barrels of oil from our country’s Strategic Petroleum Reserve (the largest release in the almost 50-year history of the reserve ), while also pushing for penalties on those energy companies sitting on unused permits (i.e., Source: Yardeni.com.

The Strategic and Tactical AssetAllocation Committee’s (STAAC) S&P 500 year-end fair value target of 4,000-4,100 is based on a price-to-earnings ratio of 17.5 Corporate bonds are considered higher risk than government bonds. It is also a major component used to calculate the price-toearnings valuation ratio.

Retailer valuations have also taken a hit, as the forward (next 12 months) P/E multiple has contracted ~20% year to date, from ~27x to ~22x currently. Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. All index data from Bloomberg. 12/2023).

The Strategic and Tactical AssetAllocation Committee (STAAC) upgraded its view of duration to neutral. Corporate bonds are considered higher risk than government bonds. It is also a major component used to calculate the price-toearnings valuation ratio. Municipal bonds are subject to availability and change in price.

The Strategic and Tactical AssetAllocation Committee (STAAC) downgraded its view of emerging market (EM) equities in August. Corporate bonds are considered higher risk than government bonds. It is also a major component used to calculate the price-toearnings valuation ratio.

Still, as we survey what are better equity valuations, long-awaited income opportunities in the bond market, and a likely less-antagonistic Fed in 2023, there may be emerging reasons to believe that the next year may be more constructive than the last. Assetallocation does not ensure a profit or protect against a loss.

Job gains were broad-based and especially prominent in sectors such as education, health care, and government. We maintain our preference for equities over fixed income and cash in our recommended tactical assetallocation. It is also a major component used to calculate the price-to-earnings valuation ratio. 08/23).

And so in the 1990s, I developed the, the late 1980s, early 1990s, I developed a skillset around valuation, in particular discounted cash flow or residual income type models, along with a couple of peers out of the consulting industry. 00:04:02 That’s what value add software was originally. They are too concentrated relative to that.

We tend to be strategic rather than tactical in our approach to investing, but a combination of recent fundamental developments and valuation changes has caused us to add a note of caution in conversations with clients and in the management of their portfolios. Concentration: Much of the U.S.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content