This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

2023 AssetAllocation Perspectives and Outlook ajackson Mon, 03/06/2023 - 14:43 We are pleased to share Brown Advisory’s 2023 Outlook. Each year, the Annual Outlook report assesses the current investment landscape and discusses some of the main themes being expressed in client portfolios.

2023 AssetAllocation Perspectives and Outlook ajackson Mon, 03/06/2023 - 14:43 We are pleased to share Brown Advisory’s 2023 Outlook. Each year, the Annual Outlook report assesses the current investment landscape and discusses some of the main themes being expressed in client portfolios.

2021 AssetAllocation Perspectives and Outlook. Valuations seem stretched, and there may be many signs that animal spirits are soaring. Valuations across asset classes, and the importance of interest rates to these valuations. Fri, 02/26/2021 - 13:22. Download the full report >. Download the full report >.

CIO Perspectives Webinar, 2022 AssetAllocation Outlook mhannan Fri, 03/18/2022 - 06:42 Markets have been unsteady at the start of 2022, driven by geopolitical tensions, inflation, and concerns about equity valuations. The war in Ukraine is causing even more uncertainty. Rodrigo is now available.

CIO Perspectives Webinar, 2022 AssetAllocation Outlook. Markets have been unsteady at the start of 2022, driven by geopolitical tensions, inflation, and concerns about equity valuations. CIO Perspectives Webinar, 2022 AssetAllocation Outlook . Fri, 03/18/2022 - 06:42. Download transcript. Watch the Video.

AssetAllocation: Caution Toward High Dividend Yielding Stocks achen Fri, 10/28/2016 - 11:25 Why Have High Dividend Yielding Sectors Done Well This Year? According to Morningstar, overall assets in dividend-focused ETFs and mutual funds have ballooned to $672.6 billion in assets they held in 2011. Reach for yield.

AssetAllocation: Caution Toward High Dividend Yielding Stocks. According to Morningstar, overall assets in dividend-focused ETFs and mutual funds have ballooned to $672.6 billion in assets they held in 2011. Stretched Valuations. Fri, 10/28/2016 - 11:25. Why Have High Dividend Yielding Sectors Done Well This Year?

So what we find, and then of course we have a multi-asset solutions business where we talk to clients about the entirety of their portfolio, their strategic assetallocation models. So you’re Chief Investment officer of Asset and Wealth Management. So we start with a strategic assetallocation.

Assetallocation for a year where bonds offer the most attractive returns they have compared to the expected returns for stocks in decades. MORE ON THIS TOPIC 2023 AssetAllocation Perspectives and Outlook We are pleased to share Brown Advisory’s 2023 Outlook. multinationals and aggregate demand.

In the world of market valuation metrics, few have gained as much prominence as the Shiller P/E Ratio, also known as the Cyclically Adjusted P/E (CAPE) Ratio. Made famous during the late 1990s tech bubble, this metric continues to be a valuable tool for investors seeking to understand market valuations and potential future returns.

She was CIO at Merrill Lynch Asset Management, and now CIO at both Morgan Stanley Wealth Management and runs their assetallocation models and their outsourced chief investment officer models. 00:20:56 [Speaker Changed] So, so let’s talk a little bit about what goes into managing a hundred plus billion dollars in assets.

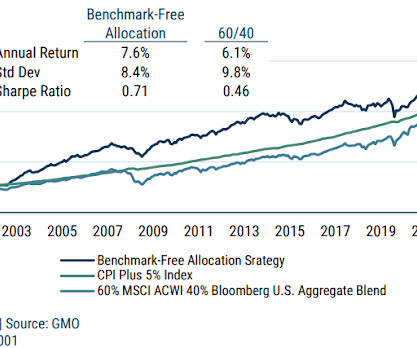

GMO posted a short paper in support of its Benchmark Free AssetAllocation Strategy (BFAAS). For this post we'll focus on BFAAS' assetallocation. The asset mix is 53.6% A more detailed look at the asset mix shows the the following. A more detailed look at the asset mix shows the the following.

Smart investors are very careful about market valuations (prices) and investor behaviour. The chart below illustrates that the smart money enters when valuations are low and the majority of the investors aren’t looking at that asset class or security.

Instead, we got a shockingly fast collapse of a financial institution with over $200 billion in assets, which turned the market’s focus toward the stability of the banking system and what systemic risks banks might be facing. But valuations strongly favor value over growth. The S&P 600 small cap index has returned about 1.5%

While February’s volatility did not materially change our assetallocation views, it reinforced to us the importance of a comprehensive discussion about how we think about risk and how we manage it. Our assetallocation process accounts for a wide range of potential outcomes over the next 18–36 months.

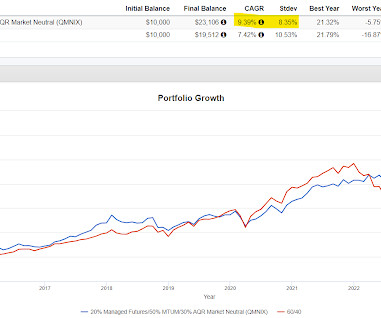

Finomial looked at the excess return generated long only factors like momentum, quality, various valuation metrics and I would add covered call fund to this discussion too. The time period is short obviously but the assetallocation appears to work. A few different things for this post. MBXIX is a proxy for FIG's macro sleeve.

Alternatively, nonprofits can boost potential portfolio returns, which often means tolerating more risk and illiquidity, through a recalibration of assetallocation— the single biggest driver of long-term gains. Reassess assetallocation. Callan estimated that a portfolio in 2005 could achieve a 7.5% large-cap strategies.

Formally, this is often referred to as “capital sufficiency” planning and more informally, it is often called spend-rate planning. As we stated in “Confronting the Unknown,” our 2018 assetallocation publication, standard deviation is “a helpful shortcut for thinking about risk, but it is not a fully effective proxy.”

Formally, this is often referred to as “capital sufficiency” planning and more informally, it is often called spend-rate planning. As we stated in “Confronting the Unknown,” our 2018 assetallocation publication, standard deviation is “a helpful shortcut for thinking about risk, but it is not a fully effective proxy.”

I found this conversation to be fascinating, informative. CHANCELLOR: And look — yeah, but then if you look at the valuation of the market at that time, the market was — the U.S. CHANCELLOR: And look — yeah, but then if you look at the valuation of the market at that time, the market was — the U.S.

EUROPEAN RE-ENTRY: Why We Are Shifting Portfolios Toward European Stocks achen Thu, 06/01/2017 - 02:47 Assetallocation—at least for us—is an exercise in nuance. We move slowly and carefully when it comes to shifting our portfolios away from one asset class or region and toward another. is not particularly notable.

Assetallocation—at least for us—is an exercise in nuance. We move slowly and carefully when it comes to shifting our portfolios away from one asset class or region and toward another. EUROPEAN RE-ENTRY: Why We Are Shifting Portfolios Toward European Stocks. Thu, 06/01/2017 - 02:47. is not particularly notable. is much clearer.

As with many things in life, the truth is somewhere between the extremes: While both simulated and real-world data suggest momentum may not be suitable as a driver of long-term assetallocations, we believe momentum considerations can be integrated in a cost-effective way to help inform daily portfolio management decisions.

The LPL Research Strategic and Tactical AssetAllocation Committee is increasing its recommended interest rate exposure in its tactical allocation from underweight to neutral. This material is for general information only and is not intended to provide specific advice or recommendations for any individual.

But beyond the economic cycle’s age, several factors suggest that a more defensive mindset is worth considering: Valuations are elevated. Robust Q1 2018 earnings growth improved the valuation picture for U.S. It is worth noting that valuations are more reasonable in developed international and emerging markets; however, U.S.

But beyond the economic cycle’s age, several factors suggest that a more defensive mindset is worth considering: Valuations are elevated. Robust Q1 2018 earnings growth improved the valuation picture for U.S. It is worth noting that valuations are more reasonable in developed international and emerging markets; however, U.S.

Increased equity exposure in tactical assetallocation from 62% to 65%. Reduced low duration core bond allocation and increased allocation to small cap equities. The Strategic and Tactical AssetAllocation Committee (STAAC) changed its recommended assetallocation for July, shifting from core bonds to small cap equities.

IBM loses to QCOM based on valuation. Sticking back to the balancing theme of quality businesses, great valuations, meshed with the reward of a dividend, you get Ford yielding 4.62% and Conoco only at 2.16% but trading for a bargain P/E of 7. times and return on equity (ROE) of 9%. As an economy, however, China will soar this year.

But the drop in valuations experienced at year’s end, alongside higher bond yields, offer a foundation for better long-term return expectations across most asset classes. This is also a fitting moment to review the intersection of risk and valuation. Entering 2019, we face rising economic, political and market risks.

DotEx International Limited distributes real-time market information. The exchange operates an “anywhere, any asset” trading platform. Indian households traditionally invested most savings in physical assets. However, financial assetallocation increased recently. lakh crore and ₹3.1

However, the impending end of the Federal Reserve (Fed) rate-hiking campaign, and the economy’s and corporate America’s resilience, help make the bull case that steers LPL Research toward a neutral, rather than negative, equities view from a tactical assetallocation perspective. At the same time, the resilience of the U.S.

The Strategic and Tactical AssetAllocation Committee (STAAC) made no changes to its recommended assetallocation for August. This material has been prepared for informational purposes only, and is not intended as specific advic or recommendations for any individual. We could see a retest of 3.5%

economy to avoid recession, and support above-average valuations. The relationship between inflation and stock valuations is a strong one, as shown in Figure 2 , which meant the market could no longer support price-to-earnings (P/E) ratios over 20 (the same goes for the relationship between interest rates and stock valuations).

When macro conditions are uncertain, a banker’s approach to valuation can help. David, a former investment banker, has always brought a banker’s mentality to valuing smaller companies by breaking down their assets and operations into components that can be more accurately assessed.

equity market: A comparatively quick interest rate increase counteracts the benefit from stronger economic growth, impairing profitability and valuations. Concern about future economic growth undermines valuations. equity valuations exceed the historical average and the strong dollar poses headwinds to corporate profitability.

One equity market debate discussed frequently in the LPL Research Strategic & Tactical AssetAllocation Committee (STAAC) is the growth vs. value style reversal experienced the past 12 months. Increasing the discount rate, which lowers the present value of future cash flows, and company valuations. IMPORTANT DISCLOSURES.

Retailer valuations have also taken a hit, as the forward (next 12 months) P/E multiple has contracted ~20% year to date, from ~27x to ~22x currently. This material is for general information only and is not intended to provide specific advice or recommendations for any individual. IMPORTANT DISCLOSURES. All index data from Bloomberg.

These items are not static, and can change over time, therefore it’s important to revisit your assetallocation periodically as financial circumstances and life events change your objectives. Short-term news cycle headlines shouldn’t drive portfolio decision-making, but rather your personal objectives, goals, and risk tolerance.

In Engines That Move Markets, a 2002 book about the cycles of technology investing, Alasdair Nairn defines “bubbles” as periods when investors appear to suspend rational valuation, much as they had during the dotcom craze shortly before the book was published. Unsurprisingly, as volume has increased, so have valuations. Possible Signs.

Higher interest rates are challenging stock valuations and perhaps pushing the gains further out in 2023, but we still see solid potential for double-digit returns for stocks this year. IMPORTANT DISCLOSURES This material is for general information only and is not intended to provide specific advice or recommendations for any individual.

Still, as we survey what are better equity valuations, long-awaited income opportunities in the bond market, and a likely less-antagonistic Fed in 2023, there may be emerging reasons to believe that the next year may be more constructive than the last. Assetallocation does not ensure a profit or protect against a loss.

We tend to be strategic rather than tactical in our approach to investing, but a combination of recent fundamental developments and valuation changes has caused us to add a note of caution in conversations with clients and in the management of their portfolios. Concentration: Much of the U.S.

We tend to be strategic rather than tactical in our approach to investing, but a combination of recent fundamental developments and valuation changes has caused us to add a note of caution in conversations with clients and in the management of their portfolios. Concentration: Much of the U.S. Risks in Bonds.

The Strategic and Tactical AssetAllocation Committee’s (STAAC) S&P 500 year-end fair value target of 4,000-4,100 is based on a price-to-earnings ratio of 17.5 This material has been prepared for informational purposes only, and is not intended as specific advice or recommendations for any individual. IMPORTANT DISCLOSURES.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content