This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Nonetheless, given the scale and brand awareness of the wirehouses, and as their own use of fee-based models increases (as opposed to primarily relying on commissions from selling products), competition for clients (and advisors) will likely remain stiff going forward, even amidst the favorable trends for RIAs Also in industry news this week: A recent (..)

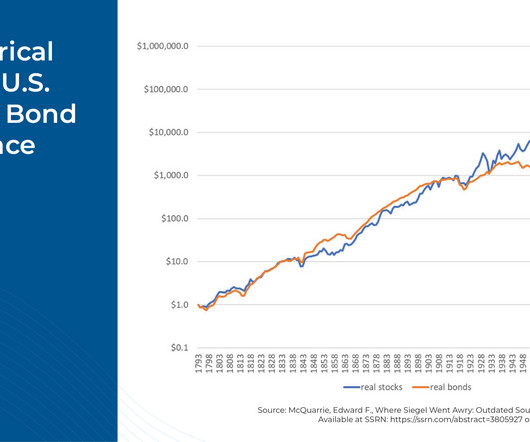

Every document that considers the facts around any particular asset class will invariably include that disclaimer, but constructing a portfolio consisting of a mix of equities, fixed income, and other assets requires investors and advicers to make some fundamental assumptions around long-term expected returns and correlations between assets.

Enjoy the current installment of “Weekend Reading For Financial Planners” – this week’s edition kicks off with the news that RIA clients of an insurance broker providing Errors & Omissions (E&O) coverage saw a 213% increase in claims paid in 2023, attributed to significant jumps in suitability claims (likely stemming (..)

Rebalancing your 401(k) and investment portfolio is an important part of a successful investment strategy. Your assetallocation is the percentage of your portfolio that you distribute between different asset classes, like stocks and bonds. There are a couple main reasons to rebalance your investment portfolio.

Making investment decisions based on the outcome of elections, or how investors think they might unfold, is unlikely to result in reliable excess returns. On the contrary, it may lead to costly mistakes. The firm only transacts business in states where it is properly registered or is excluded or exempted from registration requirements.

Developing an assetallocation and investmentplan that suits you , which may be different than who left you the inheritance. Concentrated holdings with an emotional attachment (often blue-chip stocks) can derail an investmentplan. Shoring up college funds. Topping off an emergency fund. What not to do?

As the tax year draws to a close, many high-income investors will look to reposition their portfolios to intentionally generate losses as a way to offset gains — an investment strategy known as tax loss harvesting. I sort of think of tax loss harvesting as the eharmony of investmentplanning. A net neutral tax position.

Rebalancing a 401(k) refers to adjusting the assetallocation of your investment portfolio back to its original target percentages. Your investment strategy determines the target percentages for each asset, often based on your risk tolerance, investment goals, and time horizon. What is 401(k) rebalancing?

Different cycles of growth and inflation over time tend to favor other asset classes. Maintaining an appropriate assetallocation for an investor’s specific goals and risk tolerance is critical for long-term success. Retirement planning is a long-term process with many risks and challenges for investors.

Earning the CFP designation requires a rigorous course of study covering investmentplanning, income taxation, retirement planning and risk management. A Person who completes the CFP course is qualified to provide financial planning services to those with a high degree of financial responsibility.

About Rebalancing Investments. When people buy and sell sections of their portfolio to maintain a consistent assetallocation, they are rebalancing their investments. Individuals may also readjust their portfolios if their risk level changes and they need to develop a new assetallocation strategy.

AssetAllocation. Building on diversification, assetallocation is an investment strategy that builds your portfolio by weighing an adequate amount of risk for your goals. Assetallocation evaluates how your portfolio is created and the specific securities you are investing in.

The topics covered are personal finance & investmentplanning, risk, return & assetallocation, equity markets, analysis, investing, mutual funds and strategies for wealth creation. The Introduction to Wealth Management is a beginner-level course of 12 hours duration with 6 sections of 2 hours each.

A goal-based investing approach is one such strategy. It stands out as it focuses directly on your goals, determining the amount of money you need to achieve your financial goals, and then developing an investmentplan designed to achieve those goals within a specific timeframe. 5 steps involved in goal-based investing 1.

One can prepare a customized plan depending upon their investment liking and understanding of different asset classes, sub-categories, and their own risk profile. Having a sense of market/asset class cycles and at which stage we could be in that cycle helps tremendously.

Investment advisors take the time to understand their client’s objectives, time horizons, and risk appetites before crafting customized investmentplans. Building a Diversified Portfolio: Diversification is a fundamental principle of sound investing.

Younger investors have a much longer time frame before they need investment proceeds. Talking with a qualified investment advisor can help you develop an assetallocation appropriate for meeting your financial goals. Determine an Appropriate Risk Tolerance for a Longer Time Horizon .

With these elements in mind, the advisor can develop a customized investmentplan that aligns with your risk tolerance and helps accumulate sufficient funds to turn your dream of travel into a tangible reality. A financial advisor can actively monitor your investments.

The CFP Program Structure Comprehensive Curriculum Design The CFP program offers a unique 4-in-1 certification structure that covers all essential areas of financial planning: InvestmentPlanning: Understanding market dynamics, portfolio management, and assetallocation strategies Retirement and Tax Planning: Mastering retirement solutions and tax-efficient (..)

However, you may not understand what is the purpose of tax-deferred retirement accounts or understand that these accounts may not necessarily provide the best investment options for your situation. You also have to consider factors such as risk tolerance, investment goals, and assetallocation when making investment decisions for retirement.

However, you may not understand what is the purpose of tax-deferred retirement accounts or understand that these accounts may not necessarily provide the best investment options for your situation. You also have to consider factors such as risk tolerance, investment goals, and assetallocation when making investment decisions for retirement.

Staying committed to my investmentplan, even during market downturns, has been crucial. Instead of panicking and selling my investments, I maintained my course, knowing that markets eventually rebound. So consider investing in exchange-traded funds (ETFs), index funds , bonds etc that cover various sectors (e.g.

Make sure that the investments in your account reflect what you are trying to accomplish, both short and long term. Finding Your Best Investing Strategy Tip #2: Understand and Diversify Your AssetAllocation In addition to your goals, the asset mix in your portfolio should reflect your time horizon and risk tolerance.

This can help you establish a strong foundation and craft your investment strategy. Checking your retirement account balance early on is essential to confirm that your assetallocation matches your risk tolerance and long-term goals. You can use this time to adjust your assetallocation to prioritize capital preservation.

We have found that clients who clarify their values and reflect them in their portfolios view that process as a cornerstone of their investmentplan, and they tend to successfully stick to that plan for the long term. Meanwhile, four out of five financial advisors wait for investors to begin the conversation, Calvert says.

We have found that clients who clarify their values and reflect them in their portfolios view that process as a cornerstone of their investmentplan, and they tend to successfully stick to that plan for the long term. Meanwhile, four out of five financial advisors wait for investors to begin the conversation, Calvert says.

Whether you are hoping to start investing small amounts of money or you have a lump sum of cash to get started, you should know that investing isn’t necessarily a “set it and forget it” activity. Also remember that, like it or not, there is a real risk of losing some of your investment over the short-term.

Services: I offer investment management as an add-on to financial planning. If just doing investment management alone – it would be the usual balancing, tax-loss harvesting (If warranted), assetallocation etc., pretty much everything, that goes into this.

While the prudent investment standard should apply here as with all fiduciary investment decisions, the range of options is fairly wide depending on the situation—from a model that resembles a pension portfolio to one that is closer to the Yale Endowment Model. Other factors to consider include: The targeted residuum (i.e.,

While the prudent investment standard should apply here as with all fiduciary investment decisions, the range of options is fairly wide depending on the situation—from a model that resembles a pension portfolio to one that is closer to the Yale Endowment Model. CHOOSING THE RIGHT INVESTMENT APPROACH.

And also, the majority of us lack the patience to implement logical investmentplans with discipline. Without patience and discipline, long-term investment success is just a mirage. Truemind Capital Services is a SEBI Registered Investment Management & Personal Finance Advisory platform.

Similarly, you can invest in various sectors, such as technology, pharmaceuticals, tourism, and others. No matter the assetallocation, keeping a healthy mix of stocks is always advised, especially if you are not nearing retirement anytime soon. This removes the burden off your shoulders and delivers similar growth.

However, there are some ways to lower risk, amplify the chances of earning more returns, and above all, understand the market so you can make sound investment decisions. You can use the following process to invest your money safely: 1. Know your financial goals: Your goals are the foundation of your investmentplan.

Dear Mr. Market: Finally. It’s here… a bonafide stock market correction. What’s also almost here is Groundhog Day…but more on that in a minute. For those of us with short memories we’ll have to do the necessary preamble and small talk refresher on what this is.

This will help you decide if you should continue investing in them or shift your money to a different financial asset. If your assetallocation has changed from the original ratio, you can consider rebalancing it to suit your present financial goals and objectives. Make sure your investment portfolio is well-diversified.

Liquidity, like many concepts in the investment world, is simple on the surface but becomes far more complex when one examines it more deeply. Essentially, liquidity refers to how quickly an investment can be turned into cash. Both forms of liquidity are important to keep in mind when building a long-term investmentplan.

Liquidity, like many concepts in the investment world, is simple on the surface but becomes far more complex when one examines it more deeply. Essentially, liquidity refers to how quickly an investment can be turned into cash. Both forms of liquidity are important to keep in mind when building a long-term investmentplan.

Assetallocation is the primary building block of any investment strategy. It is the process of spreading investments across various asset classes to optimize the balance between risk and potential returns. As discussed above, it varies according to individual investment goals, time horizons, and risk tolerance.

Each of these decisions are critical and at least as important as your assetallocation. When I say that everyone needs a plan, I don't necessarily mean that everyone needs a detailed financial plan. What I mean is that you need an investmentplan. What other retirement accounts should I be funding and how?

Established in the year 2016 backed by a strong full-service broker India Infoline (IIFL), 5 paisa is looking to revolutionize the idea of broking service as it is majorly focused upon investmentplanning and guides what should be the assetallocation which makes it even more unique amongst the competitors.

And so the institutional space, or most asset selectors, assetallocators are gonna look for managers that are trying to add value. The problem is how do you get into hold those securities and how do you get out when the time comes to sell them? 00:22:59 [Speaker Changed] So you and I are not disagreeing at all.

Unlike the average investor or other financial professionals, a CFP is a licensed expert in areas like estate planning, taxes, retirement, insurance, and investmentplanning. Retirement planning, estate planning, tax planning. Developing a diversified investment portfolio.

Fisher, 1958 The Money Game - George Goodman, 1967 A Random Walk Down Wall Street - Burton Malkiel, 1973 Manias, Panics, and Crashes: A History of Financial Crises - Charles Kindleberger, 1978 The Alchemy of Finance - George Soros, 1987 Market Wizards - Jack Schwager, 1989 Liar's Poker - Michael Lewis, 1989 101 Years on Wall Street, An Investor's Almanac (..)

Assetallocation is more important than the selection of a portfolio’s component parts. An otherwise great investmentplan can readily become a disaster if it doesn’t line up with our understanding, goals, objectives, risk tolerances, and risk capacities. Simple generally beats complex.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content