This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

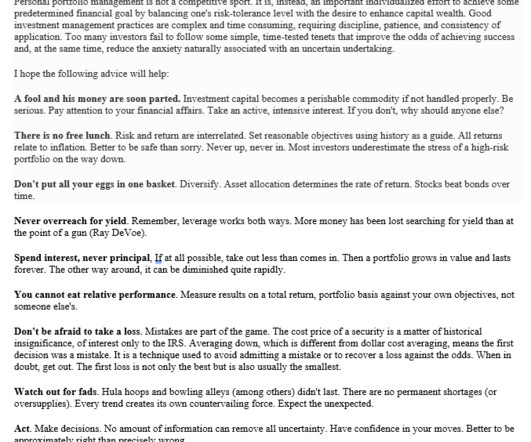

He eventually became president of Merrill Lynch AssetManagement, leading the division with a value-oriented approach and a focus on long-term fundamentals. He co-authored Investment Analysis and Portfolio Management , now in its fifth edition. Most investors underestimate the stress of a high-risk portfolio on the way down.

AssetAllocation: Developing a Long-Term Investment Strategy for Mission-Driven Organizations. When putting a plan in place, we believe it is critical for any mission-driven organization to develop an effective, long-term assetallocation strategy to manage its endowment assets. Tue, 09/06/2022 - 10:30.

If one stock makes up more than 10% of your overall assetallocation, it’s probably too much. A diversified portfolio is the cornerstone of a risk-adjusted investment strategy. Since single stocks don’t move like the broader market, you’re exposed to much greater risk.

Stocks and bonds differ in many aspects, including the risk and return investors can expect. Because of these differences, stocks and bonds accomplish different things in an assetallocation. The choice between stocks and bonds depends on their individual circumstances, such as risktolerance, time horizon, and financial goals.

A portfolio review can help you: Assess your investment objectives and confirm they align with your financial plan Evaluate your time horizon and risktolerance Ensure proper diversification and assetallocation Review tax management strategies, including capital gains and the Net Investment Income Tax (NIIT) Monitor performance beyond just returns, (..)

However, what is equally critical when it comes to creating a portfolio is assetallocation and selection. Assetallocation aims to balance risk and reward through a portfolio composition of different kinds of assets. If not allocated efficiently, you may become subject to a slew of taxes and other charges.

If you’re not working with a financial advisor , seriously consider your appetite for ongoing portfolio management, fund analysis, rebalancing, etc. In another words, if your assetallocation is 60% stocks and 40% bonds, the current weighted average yield is 2.19%. appeared first on Darrow Wealth Management.

Your lifestyle, goals, family situation, and risktolerance will give a unique signature to your retirement plan. Develop Your Personal AssetAllocation Now that have your 401(k) and IRA open and funded, how can you determine the correct assetallocation for each? How much should I be saving?

The financial advisor recommends rebalancing within the assetallocation. This is measured vs. a model specific to the client’s risktolerance. The client knows someone else (often the money manager) is driving the bus. The advisor and client work together to identify goals and work toward them.

Any investment strategy that does not incorporate your goals, time horizon, and risktolerance is flawed. Perhaps it’s time to rebalance and to rethink your ongoing assetallocation. Solid, well-managed active funds can also contribute to a well-diversified portfolio. Take stock of where you are. Costs matter.

Review risktolerance and current assetallocation strategy It’s important to ensure your clients’ portfolios align with their risktolerance because taking too much risk can negatively impact their ability to navigate market fluctuations.

He is the Chief Investment Officer of Asset and Wealth Management at Goldman Sachs. He’s a member of the management committee. He co-chairs a number of the assetmanagement investment committees. I thought this was an absolutely fascinating way to see the world of investment management.

In investments, having too high a return expectation with a lesser ability to take risks can disrupt your game. Having a very low-risktolerance can compromise achieving decent returns. This is the only way to create wealth by way of compounding in the long term.

If so, this is a good time to revisit your assetallocation and perhaps reduce your overall risk. Manage your portfolio with an eye towards downside risk. Manage your portfolio with and eye towards downside risk. Learn from the past . Maybe they’re right. Click To Tweet. Need help getting on track?

Your assetallocation is the percentage of your portfolio that you distribute between different asset classes, like stocks and bonds. To rebalance your portfolio, you’ll buy and sell certain investments to realign to your accounts with your desired assetallocation.

Donations to endowment funds are tax-deductible, giving them a place in your overall financial management and tax plan. Quasi-Endowment Also known as a board-designated endowment, this type of endowment is managed by the governing board of the organization the fund serves, rather than by the donor.

Rebalancing a 401(k) refers to adjusting the assetallocation of your investment portfolio back to its original target percentages. Your investment strategy determines the target percentages for each asset, often based on your risktolerance, investment goals, and time horizon. Click to compare vetted advisors now.

You see, financial advisors that focus primarily on wealth management can be costly to keep around. They charge either a percentage of assetsmanaged or a flat hourly rate that can run as high as several hundred dollars per hour, plus trading commissions and administrative fees. Personal Capital to the rescue.

How to Choose the Right Wealth Management Firm in Kansas City Managing your wealth is a crucial aspect of financial success and security. Let’s look at key factors to consider when selecting the ideal wealth management firm in the Kansas City metro area. But with many options available, how do you choose the right one?

Once you have your goals set, you can build your plan with any combination of the following elements: Budgeting and expense management: Create a detailed budget outlining income, expenses, and savings targets. Debt management: Develop a strategy to pay off existing debts efficiently, minimizing interest costs.

How to Choose the Right Wealth Management Firm in Kansas City Managing your wealth is a crucial aspect of financial success and security. Let’s look at key factors to consider when selecting the ideal wealth management firm in the Kansas City metro area. But with many options available, how do you choose the right one?

Individuals can choose the investment options that best suit their retirement goals and risktolerance. Investment Options : Individuals should choose a provider that offers a wide range of investment options to meet their retirement goals and risktolerance.

Managing Partner, Wealth Solutions? . An individual who learns to manage $4,000 a month after taxes will be equipped to manage $14,000 or even $40,000 a month as their earnings increase over time. All investing requires risks, past returns are not indicative of future performance.? ? . Craig Lemoine, Ph.D.,

It ensures that your portfolio aligns with your risktolerance and enables you to establish the desired equilibrium between stocks and bonds. This helps you maintain a risk profile that resonates with your financial goals. It allows you to realign your assetallocations as your financial objectives evolve.

Carbonneau is VP at Validea & Partner at Validea Capital Management. So, zooming out in investing and realizing what is and isn’t important is something we can all do more. See some of the best images the James Webb Space Telescope has taken so far in this 2-minute YouTube video.

When it comes to managing wealth and planning for a secure financial future, the services of financial professionals, such as financial advisors or wealth managers, are invaluable. Wealth managers and financial advisors offer a wide range of wealth management services designed to help clients achieve their financial goals.

Endowment and Foundation Challenges: Managing Charitable Gift Annuities ajackson Tue, 09/29/2020 - 14:00 The charitable gift annuity is one of a number of donor-friendly solutions that nonprofit institutions can offer to donors. However, the management of underlying assets in a gift annuity pool is a different matter.

Endowment and Foundation Challenges: Managing Charitable Gift Annuities. However, the management of underlying assets in a gift annuity pool is a different matter. There are numerous factors that are important in planning how to meet CGA liabilities and manage underlying gift annuity pools. Tue, 09/29/2020 - 14:00.

Financial advisors can offer insights into a diverse range of investment instruments, including stocks, bonds, real estate, and precious metals like gold, and align the recommendations with your risktolerance and long-term goals. Engaging with a skilled financial advisor can empower you to manage your taxes proactively.

However, relying on a single asset class or Investment within an Asset class can be risky and limiting. Diversifying your investment portfolio is a vital strategy for managingrisk, optimizing returns, and achieving your financial goals. They take the time to understand your goals, risktolerance, and current investments.

Last fall I fulfilled one of my bucket list items and became an Adjunct Professor at Golden Gate University teaching the Personal Investment Management course. This is where it goes into real financial advice as well as explanations on assetallocation, diversification and risktolerance.

When a rough economic patch appears on the horizon, your clients seek your guidance to help them check their emotions and stick to a strategy to help them manage market risk. For example, less than half (45%) of women polled in our recent Advisor Authority survey said they have a strategy to protect against market risk.

Remember, each strategy has its pros and cons so the best way to maximize them is working with a financial planner who’ll help your portfolio reflect the right risk with your financial goals. Diversification is a riskmanagement strategy that seeks to ensure your portfolio isn’t over- or underexposed in a certain area.

Their knowledge extends to various investment products, riskmanagement, tax implications, and financial planning. Armed with this expertise, investment advisors can comprehensively analyze clients’ financial situations and devise tailored strategies to align with their unique goals and risktolerances.

They help with assetallocationAssetallocation is an important component of successful retirement planning, and working with the best financial advisors for retirement can provide invaluable guidance in navigating this complex terrain. This can help optimize your wealth accumulation while mitigating unnecessary risks.

Volatility can highlight the importance of working with your clients to understand their own risktolerance. But volatility can also highlight the importance of investors understanding their own unique risktolerance. For example, the portfolio may consist of 50% stocks and 50% bonds, and this allocation will not change.

Your ideal investing strategy will be unique to you: your life phase, goals and risktolerance will all play a role in informing your “ideal” methodology. There are plenty of amazing financial planners who can help you set up and manage your investments, and explain the process along the way.

Understand your risk appetite The third step is to determine the level of risk you are willing to take to achieve your goals. You must consider your risktolerance and ability to tolerate market fluctuations. This will help to determine the appropriate assetallocation for the investment portfolio.

Re-examine RiskTolerance Volatile markets may cause your clients to rethink their risktolerance, especially those who are close to retirement. You can also look at cash management and debt reduction solutions.

In today’s complex financial landscape, managing your money can be challenging. They can help you analyze your current investments, optimize your assetallocation, and make necessary adjustments to ensure your retirement nest egg grows steadily. They can also be a bit complex to manage.

Of course, one of the most important aspects of retirement planning is managing retirement taxes. Focusing Too Much on Retirement Taxes Can Lead to Poor Investment Choices When your retirement planning is centered solely around managing taxes, it can lead to poor investment choices.

Of course, one of the most important aspects of retirement planning is managing retirement taxes. Focusing Too Much on Retirement Taxes Can Lead to Poor Investment Choices When your retirement planning is centered solely around managing taxes, it can lead to poor investment choices.

The key to weathering the storm is having a diversified assetallocation that’s truly aligned with your risktolerance and appetite before there’s a personal financial problem or other negative event. Assetallocation. Don’t wait for volatility to get your investments in order!

Since trying to time regime changes is very difficult in real time without the benefit of hindsight, there are reasons to consider allocating both U.S. equities to an assetallocation. equity may be able to help reduce risk in a portfolio. Currency risk and return. and ex-U.S. Source: Callan Institute. Valuations.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content