This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Following the long run-up in the US equity markets since the bottom of the 2008–2009 financial crisis, many investors with taxable investment accounts have likely found themselves with high embedded gains in their portfolios. While the gains signal portfolio growth, they also create challenges for ongoing management.

The new platform is meant to help advisors achieve portfolio personalization at scale, and bridge an industry gap between financial planning and assetallocation.

He co-authored Investment Analysis and Portfolio Management , now in its fifth edition. Zeikel famously shared his investing insights in a 1994 letter to his daughter: “Personal portfolio management is not a competitive sport. Most investors underestimate the stress of a high-risk portfolio on the way down.

tonyisola.com) Age is just one factor when it comes to your assetallocation. ofdollarsanddata.com) Invest time in your life, not in managing your portfolio. humbledollar.com) Personal finance Two questions to ask if you need to re-prioritize your financial plan. awealthofcommonsense.com) Life is fulled with speed bumps.

What is in your control : Your Portfolio : You want to create something robust enough to withstand drawdowns and recessions; not necessarily the best possible set of assets but the ones you can live with day in and day out. This includes a broad AssetAllocation including full Diversification of asset classes, geographies, etc.

(humbledollar.com) Why age is not the be-all-end-all for assetallocation decisions. obliviousinvestor.com) How to rebalance your portfolio. Plan ahead. humbledollar.com) Retirement How much you need in retirement can differ, a lot. contessacapitaladvisors.com) How does inflation affect retirement?

Also in industry news this week: While an infusion of Private Equity (PE) capital has shaken up the RIA M&A market, the ultimate implications for advisors, their clients, and the PE firms themselves remain unclear A recent study has found that a significant portion of 'DIY' investors are open to working with a human advisor (and paying for the (..)

Though in practice, while a 1% AUM fee is a common 'starting point' in the industry, the actual fee structure can vary based on the firm's approach; for example, some firms may reduce the fee for high-net-worth clients, or charge an additional fee for separate and additional services (from deeper financial planning to add-ons like tax preparation).

Every document that considers the facts around any particular asset class will invariably include that disclaimer, but constructing a portfolio consisting of a mix of equities, fixed income, and other assets requires investors and advicers to make some fundamental assumptions around long-term expected returns and correlations between assets.

AssetAllocation: Developing a Long-Term Investment Strategy for Mission-Driven Organizations. When putting a plan in place, we believe it is critical for any mission-driven organization to develop an effective, long-term assetallocation strategy to manage its endowment assets. Tue, 09/06/2022 - 10:30.

Financial advisors have a wide range of strategies at their disposal to create financial plans for their clients. And when it comes to retirement planning, one popular technique is the use of ‘guardrails’, which set an initial monthly withdrawal rate that can be later adjusted as the size of the client’s portfolio changes.

Investors who are well-diversified may be hurt but generally not to the extent of those who are highly allocated to stocks. Review your assetallocation . If you haven’t done so recently, perhaps it is time to review your assetallocation and make some adjustments. Go shopping . The Bottom Line .

Heres how to avoid them (without giving up your weekend plans or your love for good coffee). Why This Is a Problem: Future youwho needs a house, financial security, and maybe even early retirementmight resent past you for not planning ahead. Why This Is a Problem: Many BNPL plans dont feel like debt but they are.

This ensures you wont need to sell investments when markets are down, protecting your long-term financial plan and providing peace of mind during turbulent times. Reevaluate Your AssetAllocation If watching your investment portfolio fluctuate causes anxiety, your current allocation might be too aggressive.

It’s a long-term instrument that exacerbates that asset-liability mismatch in our lives. The investor who buys a 60/40 stock/bond portfolio isn’t just diversifying across assets. Of course, you can build multi-assetportfolios many different ways. You’re temporally diversified by your income.

If you own 10,000 shares, you receive $40,000 in dividend income (before taxes) and have a portfolio currently worth $2M. You’ll receive the same $40,000 in dividend income and the value of your portfolio drops to $1.5M. Dividend paying stocks and funds can be a great addition to a portfolio.

Assuming that you have a financial plan with an investment strategy in place there is really nothing to do at this point. Ideally you’ve been rebalancing your portfolio along the way and your assetallocation is largely in line with your plan and your risk tolerance. Do nothing. Review your mutual fund holdings.

When investors create an investment portfolio, they consider several factors, like risk, asset class, inflation, etc., However, what is equally critical when it comes to creating a portfolio is assetallocation and selection. If not allocated efficiently, you may become subject to a slew of taxes and other charges.

She explains what she is concerned about: “The areas that I worry about are that bottomless pit of “unmarked” assets that have doubled or quadrupled in size and assetallocation… Think about the average teacher or firefighter pension plan – it’s 30% illiquid today versus 5% back in the 2000s.

There are many steps in building an investment portfolio, in this article, I’ll discuss how assetallocation and risk tolerance are important considerations when investing. In simple terms, assetallocation is the mix of all the different types of investments you have in your portfolio.

Sherman oversees and administers DoubleLine’s investment management subcommittee; serves as lead portfolio manager for multisector and derivative-based strategies; and is a member of the firm’s executive management and fixed-income assetallocation committees.

Imagine you have invested 50% of your money in the Nifty Index Fund portfolio. And another 50% in a mutual fund portfolio with an average of 50% debt allocation and 50% in equity allocation. And the best part is that the ICICI BAF could do this by keeping a 53% average debt allocation. How could ICICI BAF do it?

Because of these differences, stocks and bonds accomplish different things in an assetallocation. Bond Basics: How Bonds Work and Reasons to Add Bonds to Your Portfolio Stock vs bond historical returns by calendar year Investors dont hold bonds to outperform stocks over the long run. Thats not their job.

Mark is the Chief Investment Officer of Noble Wealth Management, an RIA based in Greenwood Village, Colorado, that oversees $320 million in assets under management for 160 client households. Read More.

People get conditioned to this pattern and over-allocate in the asset class out of greed and by overlooking/undermining the risk factors. One of the biggest mistakes people commit is ignoring their risk profile and suitable assetallocation, especially during runaway prices in one asset class.

As you work toward your financial goals, regularly reviewing your investment portfolio is essential. Whether youre new to investing or have years of experience, taking a step back to evaluate your strategy can help ensure that your portfolio remains aligned with your objectives, especially in times of market uncertainty and volatility.

If one stock makes up more than 10% of your overall assetallocation, it’s probably too much. A diversified portfolio is the cornerstone of a risk-adjusted investment strategy. Diversifying Around It: Balancing the portfolio by investing in assets that offset the concentrated position’s risk.

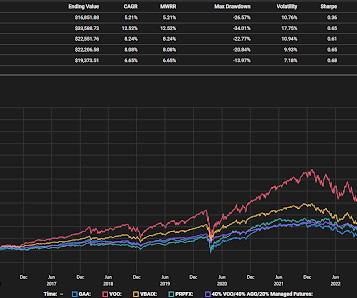

One of the pre-market Bloomberg emails gave a positive mention to the Cambria Global AssetAllocation ETF (GAA) because it is up in what of course has been a tough tape for equities this year. It is an interesting assetallocation that targets 40% in equities, 40% in fixed income and 20% in alternatives.

Further Reading: How Much Money You Need For Retirement 1We’ve talked about JEPI on Animal Spirits in a past Talk Your Book episode with the portfolio manager of the strategy —

Rather I suggest an investment strategy that incorporates some basic blocking and tackling: A financial plan should be the basis of your strategy. What impact have the solid stock market gains of the past three years had on your portfolio? Perhaps it’s time to rebalance and to rethink your ongoing assetallocation.

Lessons to learn to get better value from your wealth manager We onboarded a client with a portfolio of around INR 50 Crores, earlier managed by a big & reputed wealth management company. The portfolio was constructed for retirement purposes with 12 years of investment horizon. 40% allocation in AIFs and 20% average in debt.

Proactive year-end tax planning can lead to significant savings and set you up for financial success in the new year. Checklist: Year-end Tax Planning Strategies Review the following tax strategies with your tax advisor and/or financial advisor before the end of the year.

Retirement planning is a critical part of financial security that many women still overlook. However, remember that as a woman, you have a longer life expectancy than a man, which means retirement planning is even more important. That means you should plan for your retirement savings to last at least 18 years, if not more.

If youre searching for a fiduciary financial planner, flat-fee financial planning, or the best alternative to AUM-based advisors, this article will help you decide which model is right for you. Unlike AUM advisors, they dont have an incentive to keep assets under management, so their recommendations are truly objective.

Advisors are being asked to provide their clients with a full suite of solutions, ranging from estate and tax planning to portfolio management, and everything in between. Clients are increasingly eager to gain access to fully customizable solutions that meet their individual needs.

However, some of the folks who experienced losses well in excess of the market averages were victims of their own over-allocation to stocks. This is the time to review your portfolioallocation and rebalance if needed. Financial Planning is vital. Manage your portfolio with an eye towards downside risk.

2021 AssetAllocation Perspectives and Outlook. Each year, our Investment Solutions Group (ISG) assess the current investment landscape and discuss how we are positioning client portfolios. Each year, the Annual Outlook report assesses the current investment landscape and discusses how we are positioning client portfolios.

The set-it-and-forget-it nature of a workplace retirement plan is one of my favorite features. I like the ease and simplicity of 401k contributions coming out of my paycheck before it ever even touches my checking account. It’s easy to automate. Plus, I like the fact that it’s difficult to get the money out of these ac.

Last year’s considerable losses and market fluctuations underscore the need for clients to assess their retirement plans to ensure it aligns with their objectives, financial situations, timelines, and attitudes toward market volatility. Clients should not get discouraged by their portfolio’s past performance.

This included: 2:44 Defined Duration Investing – my new assetallocation process by which I focus on quantifying the time horizons over which to use certain instruments and help match them to a financial plan. 39:58 Saving vs Investing – We call our investment portfolios the wrong thing.

The adoption of the fee-for-service financial planning model is changing the dynamics of business operations inside wealth management firms. But without a well-defined service model to deliver financial planning services, advisors soon discover that unstructured, ad-hoc service offerings don’t scale very well.

As we move through the first quarter of 2025, weve had several clients, colleagues, and friends reach out with questions about recent market movements and the impact of tariff discussions on their personal financial plan. Diversifying portfolios across asset classes, sectors, and geographies to reduce concentrated risks.

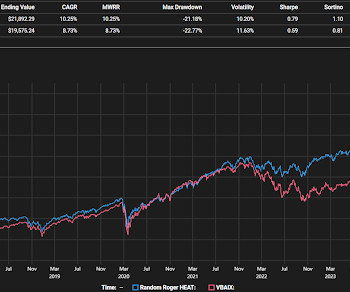

Adaptability is a great word for portfolio construction and ongoing management. I don't believe adaptability has to mean very actively trading a portfolio but there will be occasional trades that need to be made. My version of HEAT doesn't cherry pick themes from the portfolio, it's all of the holdings that I think are themes.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content