This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

By Jake Anderson, CFP ® , Wealth Planner When helping clients begin retirementplanning, the same questions often arise: What should my retirementplan look like? Your lifestyle, goals, family situation, and risk tolerance will give a unique signature to your retirementplan. How much should I be saving?

Retirementplanning is a critical part of financial security that many women still overlook. However, remember that as a woman, you have a longer life expectancy than a man, which means retirementplanning is even more important. Plan your investments. Consider early retirement tax planning.

Also in industry news this week: While an infusion of Private Equity (PE) capital has shaken up the RIA M&A market, the ultimate implications for advisors, their clients, and the PE firms themselves remain unclear A recent study has found that a significant portion of 'DIY' investors are open to working with a human advisor (and paying for the (..)

I've talked about my assetallocation before being overwhelmingly in cash or cash proxies, about 25% in "normal" equity investments, my exposure to crypto these days might be 2-3% up from 1/2 of a percent from when I bought Bitcoin in late 2018 but down from 6-7% when Bitcoin was higher.

Financial advisors have a wide range of strategies at their disposal to create financial plans for their clients. And when it comes to retirementplanning, one popular technique is the use of ‘guardrails’, which set an initial monthly withdrawal rate that can be later adjusted as the size of the client’s portfolio changes.

Assuming that you have a financial plan with an investment strategy in place there is really nothing to do at this point. Ideally you’ve been rebalancing your portfolio along the way and your assetallocation is largely in line with your plan and your risk tolerance. Do nothing. Focus on risk. Look for bargains.

Allocatingretirementplanning I introduce assetallocation with clients by dividing retirement life into two parts: basic life and high-quality life. These basic things must be planned with a certain income. After showing them that breakdown, I discuss the details of assetallocation.

I n our Countercyclical Indexing strategy I like to use a 10 year target duration for the multi-asset index, but the application of that depends on personal preference and planning needs. This is also what makes retirementplanning so difficult – you effectively lose an asset in your portfolio when your income stops or declines.

Last year’s considerable losses and market fluctuations underscore the need for clients to assess their retirementplans to ensure it aligns with their objectives, financial situations, timelines, and attitudes toward market volatility. You can help them start the year right by conducting a retirement checkup.

There are some things in life you just can’t plan for: an unexpected illness, job loss, death of spouse, disability. And while experiencing one of these major events can drastically impact your life, having an effective financial plan can help ensure that it doesn’t ruin your financial well-being. Let’s break each one down.

Before you can evaluate stocks or bonds to invest in, you’ll need to develop the metrics you plan to use in the analysis. Generally, investors don’t increase their risk profile as they move through retirement. Assetallocation Generally, dividend stocks tend to be older, more mature companies.

This is the time to review your portfolio allocation and rebalance if needed. For example, your plan might call for a 60% allocation to stocks but with the gains that stocks have experienced you might now be at 70% or more. Financial Planning is vital. Learn from the past . Photo credit: Phillip Taylor PT.

Because of these differences, stocks and bonds accomplish different things in an assetallocation. Why stocks and bonds belong in a diversified portfolio Investors have different needs, risk tolerances, time horizons, and financial situations which should be considered in an assetallocation.

This article will discuss the key features of the Microsoft 401(k) plan, and after reading it, you should leave with a clear game plan of how to: Maximize the match (free money! ) The key benefits of any 401(k) plan (including Microsoft’s) include: Free Money : A company match on your contributions.

Rather I suggest an investment strategy that incorporates some basic blocking and tackling: A financial plan should be the basis of your strategy. Perhaps it’s time to rebalance and to rethink your ongoing assetallocation. Take stock of where you are. Take stock of where you are. Costs matter. Photo credit: Flickr.

If youre searching for a fiduciary financial planner, flat-fee financial planning, or the best alternative to AUM-based advisors, this article will help you decide which model is right for you. Unlike AUM advisors, they dont have an incentive to keep assets under management, so their recommendations are truly objective.

Planning for retirement can seem premature when you have only been in the workforce for a decade or so. But as the oldest Millennials begin to hit middle age, retirement suddenly does not seem so far away. Here are five things Millennials should consider when planning for retirement. Footnotes.

The set-it-and-forget-it nature of a workplace retirementplan is one of my favorite features. I like the ease and simplicity of 401k contributions coming out of my paycheck before it ever even touches my checking account. It’s easy to automate. Plus, I like the fact that it’s difficult to get the money out of these ac.

Learn how our industry-leading assetallocation expertise can help participants make investment choices with more confidence and help employers reach their plan goals. Advice boosts workers’ confidence in choosing investments—from 35% to 65%.

The end of the year is an ideal time to start planning for the year ahead and make sure you’re on target to achieve those goals. Asset and Liability Matching. Good financial planning is all about asset and liability matching across time. A financial plan with an asset liability mismatch is likely to fail over time.

Published: March 21st, 2025 Reading Time: 6 minutes Written by: The Zoe Team Managing wealth involves more than just investingit requires careful planning, strategic decision-making, and a long-term vision. Estate Planning : Ensuring your wealth is passed on according to your wishes. Optimizing tax-efficient retirement income.

Offer more ways clients may achieve their retirementplan goals while helping address the diverse investment needs of participants. Learn about our industry-leading investments and expertise—featuring more default options and more personalized assetallocation.

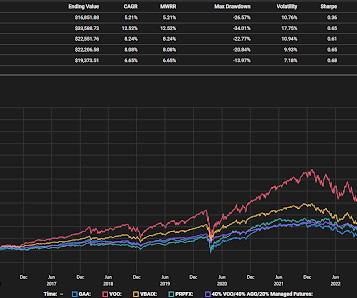

One of the pre-market Bloomberg emails gave a positive mention to the Cambria Global AssetAllocation ETF (GAA) because it is up in what of course has been a tough tape for equities this year. It is an interesting assetallocation that targets 40% in equities, 40% in fixed income and 20% in alternatives.

Don’t stress out about every headline, stress test your retirementplan instead.Markets move every day and the news cycle is 24-7. Stress testing a financial plan or retirement income goals is crucial to help ensure retirees wont run out of money under different conditions in the financial markets.

just upended retirementplanning…again. The age when retirees must begin drawing from non-Roth retirement accounts increases to 73 in 2023, then 75 in 2033. Raising the age when withdrawals must begin is great as it gives investors more planning opportunities. The Secure Act 2.0

We are thrilled to announce that our Wealth Advisors, Edzai Chimedza, CFP® and Franklin Gay , CFP®, EA will be leading two Financial Planning Seminars at Nova Southeastern University. The post Wealth Advisors Edzai Chimedza and Franklin Gay lead Financial Planning Seminars at Nova Southeastern University – April 12th and May 3rd at 11 a.m.

Your assetallocation is the percentage of your portfolio that you distribute between different asset classes, like stocks and bonds. To rebalance your portfolio, you’ll buy and sell certain investments to realign to your accounts with your desired assetallocation. Why does this matter?

Meeting with a qualified financial planning professional can help you begin building positive and lasting behaviors.?? . Take Advantage of RetirementPlans and Matching Contributions. Employers often match a portion of this contribution to a retirementplan as an employer benefit. . Million after 40 years!

It may seem unattainable, but you should probably plan for it – just in case. 1 With ever-increasing life expectancies, it’s no wonder 63% of American adults say they’re more afraid of running out of money in retirement than they are of death. As you get closer to retirement your assetallocation should change.

The simple answer is that the short-term movements of the stock market should be irrelevant to your financial plan assuming you have a well constructed temporally diversified portfolio. Insurance is largely optional and plan dependent, but I think of the other 4 time horizons as essential. Infinite or indefinite: Insurance planning.

A point we've been making here for ages is that with an adequate savings rate, appropriate assetallocation and the ability to avoid succumbing to panic, an investor should be able to have retirementplan success as defined above. If you're 60, think you want to retire at 65 and need $1.4 I'd argue not much.

We talk both retirementplanning and factor investing with Dimensional Fund Advisors Senior Researcher Mathieu Pellerin. The post Factor Investing for Retirement with DFA’s Mathieu Pellerin appeared first on Validea's Guru Investor Blog. In this episode, we combine two of the topics we often cover on the podcast.

We talk both retirementplanning and factor investing with Dimensional Fund Advisors Senior Researcher Mathieu Pellerin. The post Factor Investing for Retirement with DFA’s Mathieu Pellerin appeared first on Validea's Guru Investor Blog. In this episode, we combine two of the topics we often cover on the podcast.

The contributions made to the account may be tax-deductible or non-deductible, depending on the individual’s income level and participation in an employer-sponsored retirementplan. The deductibility of contributions depends on the individual’s income level and participation in an employer-sponsored retirementplan.

The assetallocation was 10% to hedges, 30% to T-bills for asymmetry but that seems more like optionality to me, 9% to edges which included one broad stock picking ETF, a derivative income fund and a short volatility product. None of them were hideously wrong out of the blocks but it's too soon to declare victory with them.

Earning the CFP designation requires a rigorous course of study covering investment planning, income taxation, retirementplanning and risk management. A Person who completes the CFP course is qualified to provide financial planning services to those with a high degree of financial responsibility.

The Wall Street Journal took what might be a sympathetic approach to 401k investors who might be feeling disillusioned by generally poor performance with the focus being on target date funds which have of course become a major staple of 401k plans. First, it's your retirement, how do you not care enough to engage just a little?

ESTATES Family Estate Planning: The 6 Essentials Schedule a Complimentary Financial Review CLICK HERE TO SCHEDULE. According to one survey, 67% of Americans have no estate plan, which may reflect an aversion to thinking about dying or getting gravely ill. Navigate Family Estate Planning with Park Place Financial . Related Posts.

Maintaining an appropriate assetallocation for an investor’s specific goals and risk tolerance is critical for long-term success. There’s value in staying invested in that assetallocation and not trying to time the market’s ups and downs or succumbing to fear when markets turn tumultuous.

We all know retirement is an important milestone that requires careful planning. Of course, one of the most important aspects of retirementplanning is managing retirement taxes. Taxes can significantly impact the amount of money you’ll have for retirement.

We all know retirement is an important milestone that requires careful planning. Of course, one of the most important aspects of retirementplanning is managing retirement taxes. Taxes can significantly impact the amount of money you’ll have for retirement.

By using a wealth accumulation plan! Why is a wealth accumulation plan important? The more wealth and financial assets you’ve accumulated, the easier it is to plan for bigger things in life. If you want to know how to build up your wealth from scratch, this wealth accumulation plan will help. Create a budget.

ESTATES The 5 Most Common Estate Planning Myths Schedule a Complimentary Financial Review CLICK HERE TO SCHEDULE. Estate planning is a crucial component of financial preparation for many individuals, as it enables their wealth to have a lasting and meaningful impact on their loved ones. 2) You Only Need to Plan Your Estate for Death .

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content