This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

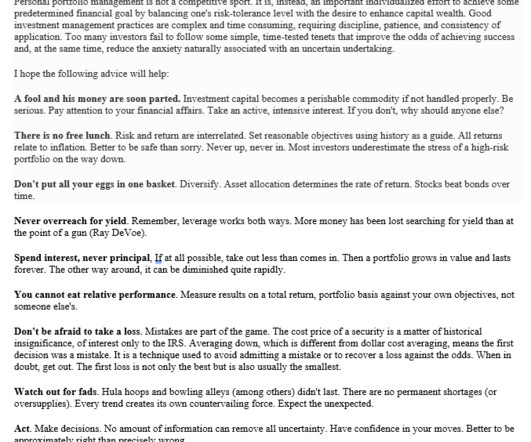

It is, instead, an important individualized effort to achieve some predetermined financial goal by balancing ones risk-tolerance level with the desire to enhance capital wealth. Most investors underestimate the stress of a high-risk portfolio on the way down. Assetallocation determines the rate of return.

By Jake Anderson, CFP ® , Wealth Planner When helping clients begin retirement planning, the same questions often arise: What should my retirement plan look like? Your lifestyle, goals, family situation, and risktolerance will give a unique signature to your retirement plan. How much should I be saving?

AssetAllocation: Developing a Long-Term Investment Strategy for Mission-Driven Organizations. When putting a plan in place, we believe it is critical for any mission-driven organization to develop an effective, long-term assetallocation strategy to manage its endowment assets. Tue, 09/06/2022 - 10:30.

Assuming that you have a financial plan with an investment strategy in place there is really nothing to do at this point. Ideally you’ve been rebalancing your portfolio along the way and your assetallocation is largely in line with your plan and your risktolerance. Focus on risk. Do nothing.

There are many steps in building an investment portfolio, in this article, I’ll discuss how assetallocation and risktolerance are important considerations when investing. In simple terms, assetallocation is the mix of all the different types of investments you have in your portfolio.

Stocks and bonds differ in many aspects, including the risk and return investors can expect. Because of these differences, stocks and bonds accomplish different things in an assetallocation. The choice between stocks and bonds depends on their individual circumstances, such as risktolerance, time horizon, and financial goals.

It is for information and planning purposes only. Whether youre new to investing or have years of experience, taking a step back to evaluate your strategy can help ensure that your portfolio remains aligned with your objectives, especially in times of market uncertainty and volatility.

High yields can be a sign of underlying issues with the company that puts principal at risk and endangers the dividend income if the company’s financials cannot support it. Before you can evaluate stocks or bonds to invest in, you’ll need to develop the metrics you plan to use in the analysis.

However, what is equally critical when it comes to creating a portfolio is assetallocation and selection. Assetallocation aims to balance risk and reward through a portfolio composition of different kinds of assets. If not allocated efficiently, you may become subject to a slew of taxes and other charges.

For more years than I’d care to name, I’ve been trying to put my finger on exactly why I have a such a huge problem with the traditional (Think: Riskalyze, now Nitrogen) risktolerance assessments in the financial planning profession. You can actually test various bear markets and adjust accordingly.)

Last year’s considerable losses and market fluctuations underscore the need for clients to assess their retirement plans to ensure it aligns with their objectives, financial situations, timelines, and attitudes toward market volatility. Here are some key points to use with clients as you help them assess their retirement plans.

Rather I suggest an investment strategy that incorporates some basic blocking and tackling: A financial plan should be the basis of your strategy. Any investment strategy that does not incorporate your goals, time horizon, and risktolerance is flawed. Take stock of where you are. Costs matter. Photo credit: Flickr.

There are some things in life you just can’t plan for: an unexpected illness, job loss, death of spouse, disability. And while experiencing one of these major events can drastically impact your life, having an effective financial plan can help ensure that it doesn’t ruin your financial well-being. Let’s break each one down.

This is the time to review your portfolio allocation and rebalance if needed. For example, your plan might call for a 60% allocation to stocks but with the gains that stocks have experienced you might now be at 70% or more. Financial Planning is vital. Manage your portfolio with and eye towards downside risk.

If one stock makes up more than 10% of your overall assetallocation, it’s probably too much. A diversified portfolio is the cornerstone of a risk-adjusted investment strategy. Since single stocks don’t move like the broader market, you’re exposed to much greater risk.

One area that often gets overlooked in the midst of planning is reviewing your financial habits and goals, so I’ve put together a short list of 3 areas to review before January. If you are unsure if your portfolio aligns with your risktolerance, time horizon and goals, reach out to us at Mainstreet and we would be happy to help!

Rebalancing a 401(k) refers to adjusting the assetallocation of your investment portfolio back to its original target percentages. Your investment strategy determines the target percentages for each asset, often based on your risktolerance, investment goals, and time horizon. Click to compare vetted advisors now.

Historically, staying the course and following a financial plan has outperformed rash investment decisions when there are times of uncertainty in the financial market. But it takes a strong plan—and no small amount of willpower—to do this. You can also look at cash management and debt reduction solutions.

Your assetallocation is the percentage of your portfolio that you distribute between different asset classes, like stocks and bonds. To rebalance your portfolio, you’ll buy and sell certain investments to realign to your accounts with your desired assetallocation. Why does this matter?

It may seem unattainable, but you should probably plan for it – just in case. 2 That’s why it’s vitally important to consider longevity risk when you’re planning for your financial needs in retirement. 2 That’s why it’s vitally important to consider longevity risk when you’re planning for your financial needs in retirement.

But you might consider increasing your impact by setting up a structured , long-term philanthropic plan such as an endowment. An endowment is a portfolio of assets that is invested to provide support for a cause. Donations to endowment funds are tax-deductible, giving them a place in your overall financial management and tax plan.

What was the original career plan? SALISBURY: Honestly, I didn’t really have a long-term plan. SALISBURY: Yes, I’d love to tell you there was some great master plan. They have a different liability structure, different investment goals, different investment risktolerances, and we have different teams.

The contributions made to the account may be tax-deductible or non-deductible, depending on the individual’s income level and participation in an employer-sponsored retirement plan. The contribution limit may be reduced or eliminated for individuals who have high incomes or who participate in an employer-sponsored retirement plan.

Meeting with a qualified financial planning professional can help you begin building positive and lasting behaviors.?? . Take Advantage of Retirement Plans and Matching Contributions. Retirement plans, such as 401(k) and 403(b) plans, allow employees to contribute a portion of their salary up to a federal limit ($20,500 in 2022).

By using a wealth accumulation plan! Why is a wealth accumulation plan important? The more wealth and financial assets you’ve accumulated, the easier it is to plan for bigger things in life. If you want to know how to build up your wealth from scratch, this wealth accumulation plan will help. Create a budget.

Maintaining an appropriate assetallocation for an investor’s specific goals and risktolerance is critical for long-term success. There’s value in staying invested in that assetallocation and not trying to time the market’s ups and downs or succumbing to fear when markets turn tumultuous.

For instance, they can guide you on leveraging employer-sponsored retirement plans, such as a 401(k) with employer matches, to optimize your contributions and harness the full benefits of the accounts. IRAs offer you the flexibility to contribute to your retirement savings independently, outside of employer-sponsored plans.

Whether planning for retirement, saving for your children’s education or simply looking to grow your investments, finding the right wealth management services in Kansas City can make all the difference. Long-term goals typically encompass retirement planning, wealth preservation and estate planning.

One popular option for college savings is a 529 plan , a tax-advantaged investment account designed specifically for education savings which can be used for qualified education expenses. Volatility can highlight the importance of working with your clients to understand their own risktolerance.

Understanding the importance of assetallocation is like building a strong financial foundation. It’s all about spreading your investments across different asset classes, like stocks, bonds, and real estate, to manage risk and maximize returns. This helps manage risk and maintain your desired balance of returns.

Their knowledge extends to various investment products, risk management, tax implications, and financial planning. Armed with this expertise, investment advisors can comprehensively analyze clients’ financial situations and devise tailored strategies to align with their unique goals and risktolerances.

It ensures that your portfolio aligns with your risktolerance and enables you to establish the desired equilibrium between stocks and bonds. This helps you maintain a risk profile that resonates with your financial goals. It allows you to realign your assetallocations as your financial objectives evolve.

AssetAllocation. Building on diversification, assetallocation is an investment strategy that builds your portfolio by weighing an adequate amount of risk for your goals. Assetallocation evaluates how your portfolio is created and the specific securities you are investing in. Dollar-Cost Averaging.

Staying committed to my investment plan, even during market downturns, has been crucial. Understand your risktolerance Assess your age, income, and goals to determine your risk appetite. Caveat: Take advantage of employer contributions Now, if your employer offers a 401(k) matching plan , don’t sleep on it.

They help with assetallocationAssetallocation is an important component of successful retirement planning, and working with the best financial advisors for retirement can provide invaluable guidance in navigating this complex terrain.

This is where it goes into real financial advice as well as explanations on assetallocation, diversification and risktolerance. There is a significant focus on the relationship between risk and reward, and the importance of deciding upon the degree of risk you’re willing to take.

Whether planning for retirement, saving for your children’s education or simply looking to grow your investments, finding the right wealth management services in Kansas City can make all the difference. Long-term goals typically encompass retirement planning, wealth preservation and estate planning.

FINANCIAL PLANNING What is Portfolio Rebalancing? For example, you can shift money between asset classes to reflect market changes and work with your financial adviser to create a diversified strategy. When people buy and sell sections of their portfolio to maintain a consistent assetallocation, they are rebalancing their investments.

You can also get information on your performance and assetallocation. Like other similar products, they first determine your risktolerance, personal preferences, and investment goals. This will help you to create an assetallocation that will get you where you need to go with your investments.

It stands out as it focuses directly on your goals, determining the amount of money you need to achieve your financial goals, and then developing an investment plan designed to achieve those goals within a specific timeframe. You must consider your risktolerance and ability to tolerate market fluctuations.

From retirement planning to market volatility, equity compensation, family expenses, and major life transitions, it’s easy to feel overwhelmed with financial responsibilities. Planning for retirement is a significant financial milestone, and you should do everything in your power to make it exactly how you envision it.

Your ideal investing strategy will be unique to you: your life phase, goals and risktolerance will all play a role in informing your “ideal” methodology. Or, if you plan to buy a house within the year and your down payment is sitting in the stock market, you might run the risk of losing that money in a down market before you buy.

Even with diligent financial planning, relying on a single source of income may expose a client to heightened financial risk during an economic downturn. Align client portfolios with their risktolerance and time horizon. Diversify your client’s income sources.

We all know retirement is an important milestone that requires careful planning. Of course, one of the most important aspects of retirement planning is managing retirement taxes. Retirement Taxes are Usually Lower than Working-Years Taxes Remember that taxes are usually lower during retirement years when planning for retirement.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content