This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

(tonyisola.com) Age is just one factor when it comes to your assetallocation. ofdollarsanddata.com) Invest time in your life, not in managing your portfolio. aptuscapitaladvisors.com) Retirement There are different levels of retirement readiness. theretirementmanifesto.com) Gen X is next up for senior living.

And when it comes to retirement planning, one popular technique is the use of ‘guardrails’, which set an initial monthly withdrawal rate that can be later adjusted as the size of the client’s portfolio changes. If the portfolio balance declines due to excess distributions (e.g., annual withdrawal rate).

The idea of living off dividends in retirement sounds nice, but investors often don’t realize how much money they’ll need invested to generate enough income from dividends to cover lifestyle expenses. If you own 10,000 shares, you receive $40,000 in dividend income (before taxes) and have a portfolio currently worth $2M.

morningstar.com) Steve Chen talks with Andrew Biggs about whether there really is a retirement crisis brewing in the U.S. podcasts.apple.com) Katie Gatti Tassin on whether you are saving too much for retirement. humbledollar.com) Why age is not the be-all-end-all for assetallocation decisions.

She advises institutional clients on investment strategies and portfolio objectives, working alongside global client advisers and product strategists across public and private markets. We discuss how the traditional “bucketing” approach of crisply defining asset classes can limit opportunities for assetallocators.

What's unique about Mark, though, is how he uses a liability-driven-investing approach to build retirementportfolios and manage sequence of return risk, with a particular focus on using closed end bond funds to generate income needed to cover his client's expenses during the early (and most financially dangerous) years of retirement.

Also in industry news this week: While an infusion of Private Equity (PE) capital has shaken up the RIA M&A market, the ultimate implications for advisors, their clients, and the PE firms themselves remain unclear A recent study has found that a significant portion of 'DIY' investors are open to working with a human advisor (and paying for the (..)

However, over the years, the 1% AUM fee has faced criticism from those who argue that it reduces the value of a portfolio by more than the advisor's guidance adds. One key starting point is to acknowledge that technically, all spending reduces the total amount that a person could have saved and had available for retirement.

As someone saving for retirement , what should you do now? The PBS Frontline special The Retirement Gamble put much of the blame on Wall Street and they are right to an extent, especially as it pertains to the overall market drop. This is the time to review your portfolioallocation and rebalance if needed.

Investors who are well-diversified may be hurt but generally not to the extent of those who are highly allocated to stocks. Review your assetallocation . If you haven’t done so recently, perhaps it is time to review your assetallocation and make some adjustments. Go shopping . Click To Tweet.

The Roth Man himself, Bill Sweet, joined me on the show this week to discuss questions about taxes in marriage, retirement withdrawal strategies, the tax implications of selling farmland and how to manage tax rates in early retirement.

When investors create an investment portfolio, they consider several factors, like risk, asset class, inflation, etc., However, what is equally critical when it comes to creating a portfolio is assetallocation and selection. If not allocated efficiently, you may become subject to a slew of taxes and other charges.

Ideally you’ve been rebalancing your portfolio along the way and your assetallocation is largely in line with your plan and your risk tolerance. You should continue to monitor your portfolio and make these types of adjustments as needed. Assess whether your portfolio has held up in line with your expectations.

There are many steps in building an investment portfolio, in this article, I’ll discuss how assetallocation and risk tolerance are important considerations when investing. In simple terms, assetallocation is the mix of all the different types of investments you have in your portfolio.

Callie Cox, our new Chief Market Strategist at Ritholtz Wealth, joined me on the show this week to discuss questions about the potential for a recession, what the Fed should do now, going all in on the Nasdaq 100 in your retirement accounts and how markets move in off hours. Further Reading: What’s the Worst Long-Term Return For U.S.

Because of these differences, stocks and bonds accomplish different things in an assetallocation. Bond Basics: How Bonds Work and Reasons to Add Bonds to Your Portfolio Stock vs bond historical returns by calendar year Investors dont hold bonds to outperform stocks over the long run. Thats not their job.

It’s a long-term instrument that exacerbates that asset-liability mismatch in our lives. The investor who buys a 60/40 stock/bond portfolio isn’t just diversifying across assets. Of course, you can build multi-assetportfolios many different ways. You’re temporally diversified by your income.

What impact have the solid stock market gains of the past three years had on your portfolio? Perhaps it’s time to rebalance and to rethink your ongoing assetallocation. Solid, well-managed active funds can also contribute to a well-diversified portfolio. View all accounts as part of a total portfolio.

Retirement planning is a critical part of financial security that many women still overlook. However, remember that as a woman, you have a longer life expectancy than a man, which means retirement planning is even more important. That means you should plan for your retirement savings to last at least 18 years, if not more.

A reader asks: Is it crazy to be 100% in stocks from age 32 to sometime in my 50s for my retirement accounts? And another reader asks a similar question: I don’t get why people work a 30+ year career while investing in stocks only to glide path into a heavier bond allocation around retirement.

Early on in my savings journey I prioritized tax-deferred retirement accounts over all else. The set-it-and-forget-it nature of a workplace retirement plan is one of my favorite features. I like the ease and simplicity of 401k contributions coming out of my paycheck before it ever even touches my checking account.

One of the pre-market Bloomberg emails gave a positive mention to the Cambria Global AssetAllocation ETF (GAA) because it is up in what of course has been a tough tape for equities this year. It is an interesting assetallocation that targets 40% in equities, 40% in fixed income and 20% in alternatives.

Last year’s considerable losses and market fluctuations underscore the need for clients to assess their retirement plans to ensure it aligns with their objectives, financial situations, timelines, and attitudes toward market volatility. Clients should not get discouraged by their portfolio’s past performance.

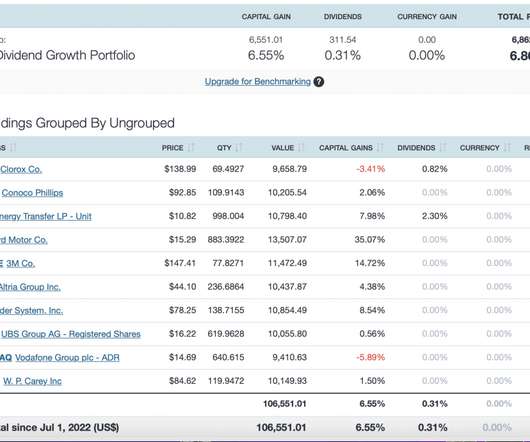

A few other tailwinds that bode well for dividend-paying stocks include historically high levels of corporate cash, low bond yields, and a demographic of baby boomers needing income to last throughout retirement. The Top 10 Dividend Growth Portfolio strategy is a concentrated portfolio.

Lessons to learn to get better value from your wealth manager We onboarded a client with a portfolio of around INR 50 Crores, earlier managed by a big & reputed wealth management company. The portfolio was constructed for retirement purposes with 12 years of investment horizon. 40% allocation in AIFs and 20% average in debt.

Saving money is an important task at any age, but as you hit your 40s, the need to save for retirement grows. While savers in their 40s and 50s typically have a decade or two left to save for retirement given the traditional age of 65, emphasizing saving now can set you up for a dream-worthy retirement.

Barron's had a roundup of advisor advice for people who want to retire early. Yes on the taxes but without earned income and living on long term capital gains from an investment portfolio, there might be no income tax. That might not sound like much income but the context here is being retired at a young age.

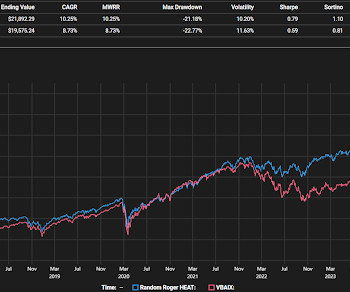

Adaptability is a great word for portfolio construction and ongoing management. I don't believe adaptability has to mean very actively trading a portfolio but there will be occasional trades that need to be made. My version of HEAT doesn't cherry pick themes from the portfolio, it's all of the holdings that I think are themes.

But what does this mean for your portfolio, and how can you continue to protect and grow your assets during these times? How Volatility Affects Investment Returns Volatility can send the value of your portfolio on an uncomfortable roller coaster ride. You can also further diversify within an asset class.

Fee-Only, Flat-Fee Financial Planners: Transparent, Unbiased, and Cost-Effective A fee-only financial planner charges a fixed fee for financial planning services, regardless of the size of your portfolio. Unlike AUM advisors, they dont have an incentive to keep assets under management, so their recommendations are truly objective.

Rebalancing your 401(k) and investment portfolio is an important part of a successful investment strategy. Your assetallocation is the percentage of your portfolio that you distribute between different asset classes, like stocks and bonds. Why do you need to rebalance your portfolio? Why does this matter?

For people nearing retirement, these challenges can be even more daunting. A market downturn at the start of retirement, hitting portfolio values when retirees begin to take account withdrawals, can be unsettling, even for seasoned investors. Many near-retirees see their highest portfolio values just before retirement.

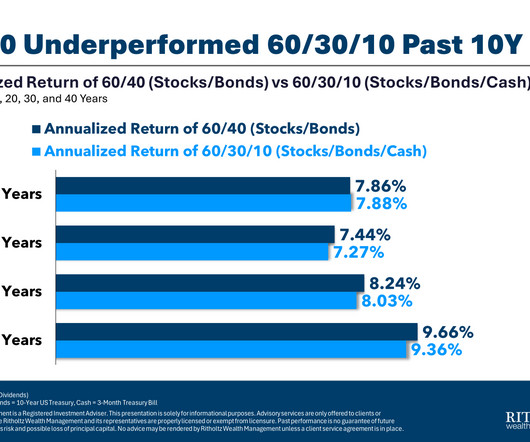

I know past is not predictive, blah, blah, blah but am well aware that cash has the lowest prospective returns of the main asset classes. Knowing this full well, I still want to keep 10% of my portfolio in cash in retirement so I can sleep at night. Would a 60/30/10 portfolio really be that much worse t.

What to Do Instead: Stick to fundamentals: Learn about assetallocation, risk management, and diversification before investing. But many jump into stocks, crypto, or NFTs without understanding risk, diversification, or assetallocation.

A financial advisor can help navigate the complexities of wealth management, from tax considerations to estate planning and retirement strategies. Their role extends beyond investment managementthey can help with: Retirement Planning : Structuring your assets to support your desired lifestyle. What Does a Financial Advisor Do?

First up was a webinar about model portfolios at ETF.com. Outsourcing the work related to actually being an advisor would not feel right to me and I enjoy what I get to do including portfolio construction. I think that when investors hear about model portfolios they sort of think in terms of set and forget.

Market performance in the early years of retirement can greatly affect how long retirement funds will last, as losses can take a larger chunk out of a portfolio when it’s more flush. The first five years of retirement are crucial for figuring out a lifestyle that can sustain you for years to come. Handle market turmoil.

According to a survey, a significant majority of Americans, approximately 80%, share the common notion that the point of working hard in your adult life is so you can enjoy a nice retirement. After years of dedicated labor and hard work, the prospect of a peaceful retirement appeals to everyone.

Don’t stress out about every headline, stress test your retirement plan instead.Markets move every day and the news cycle is 24-7. Unfortunately, headlines often leave investors wondering what the news means for their portfolio and financial outlook. How much do I need to retire? Average returns only.

Torsten Slok blogged about how ineffective bonds have been in terms of providing any return or diversification benefits lately in the context of a 60/40 portfolio. Based on the following excerpt; I built out the following leveraged allocation, taking some liberty with shortening the duration quite a bit.

I found their assetallocation and wanted to see from the top down if there's a way to mimic them to some extent and get decent results. Here's how I built the portfolio. For Portfolios 1, 2 and 3 the kurtosis readings are 0.46, 0.44 and for some reason, Portfolio 3 was 1.42. The kurtosis numbers are odd.

Whether saving for retirement, buying a home, or building an emergency fund, investing grows your wealth over time. However, relying on a single asset class or Investment within an Asset class can be risky and limiting. This is where diversifying your investment portfolio comes into play.

However, if you are nearing retirement, your risk appetite would ideally drop. This is why portfolio risk management can be very critical. However, it is crucial to understand how to manage portfolio risk and what can trigger it. What is portfolio risk? In fact, it can be good for your portfolio.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content