This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Following the long run-up in the US equity markets since the bottom of the 2008–2009 financial crisis, many investors with taxable investment accounts have likely found themselves with high embedded gains in their portfolios. While the gains signal portfolio growth, they also create challenges for ongoing management.

tonyisola.com) Age is just one factor when it comes to your assetallocation. ofdollarsanddata.com) Invest time in your life, not in managing your portfolio. mrmoneymustache.com) Why you need to account for your Treasury income on your state taxes.

What is in your control : Your Portfolio : You want to create something robust enough to withstand drawdowns and recessions; not necessarily the best possible set of assets but the ones you can live with day in and day out. This includes a broad AssetAllocation including full Diversification of asset classes, geographies, etc.

Though in practice, while a 1% AUM fee is a common 'starting point' in the industry, the actual fee structure can vary based on the firm's approach; for example, some firms may reduce the fee for high-net-worth clients, or charge an additional fee for separate and additional services (from deeper financial planning to add-ons like tax preparation).

Tax-loss harvesting is a powerful strategy that investors can use to reduce their taxable income. This type of strategy typically involves selling underperforming investments at a loss to offset capital gains (or ordinary income) to optimize portfolio returns. Table of Contents What is tax-loss harvesting?

So historically, every $1 million invested would yield annual dividend income of $19,800 on average… before tax. If you own 10,000 shares, you receive $40,000 in dividend income (before taxes) and have a portfolio currently worth $2M. Dividend paying stocks and funds can be a great addition to a portfolio.

When investors create an investment portfolio, they consider several factors, like risk, asset class, inflation, etc., However, what is equally critical when it comes to creating a portfolio is assetallocation and selection. If not allocated efficiently, you may become subject to a slew of taxes and other charges.

If one stock makes up more than 10% of your overall assetallocation, it’s probably too much. A diversified portfolio is the cornerstone of a risk-adjusted investment strategy. Diversifying Around It: Balancing the portfolio by investing in assets that offset the concentrated position’s risk.

For those in high-tax states, dividends can be particularly tax-inefficient. The Ancient Wisdom of AssetAllocation Interestingly, Faber draws inspiration from a 2000-year-old investment principle found in the Talmud, which suggests dividing one’s portfolio into thirds: business, land, and reserves.

Reevaluate Your AssetAllocation If watching your investment portfolio fluctuate causes anxiety, your current allocation might be too aggressive. You can reduce your stock exposure and increase investments in fixed income options, such as cash or bonds, within tax-advantaged accounts (like a 401(k), IRA, or Roth IRA).

As the year comes to a close, now is the time to review potential financial moves to help minimize your tax burden heading into 2025. Proactive year-end tax planning can lead to significant savings and set you up for financial success in the new year. Find your next tax advisor at Harness today. Starting at $2,500.

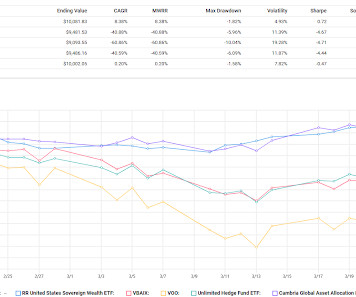

One of the pre-market Bloomberg emails gave a positive mention to the Cambria Global AssetAllocation ETF (GAA) because it is up in what of course has been a tough tape for equities this year. It is an interesting assetallocation that targets 40% in equities, 40% in fixed income and 20% in alternatives.

As you work toward your financial goals, regularly reviewing your investment portfolio is essential. Whether youre new to investing or have years of experience, taking a step back to evaluate your strategy can help ensure that your portfolio remains aligned with your objectives, especially in times of market uncertainty and volatility.

Because of these differences, stocks and bonds accomplish different things in an assetallocation. Bond Basics: How Bonds Work and Reasons to Add Bonds to Your Portfolio Stock vs bond historical returns by calendar year Investors dont hold bonds to outperform stocks over the long run. Taxes, fees, expenses, trading costs, etc.

As the tax year draws to a close, many high-income investors will look to reposition their portfolios to intentionally generate losses as a way to offset gains — an investment strategy known as tax loss harvesting. A net neutral tax position. What Is Tax Loss Harvesting? How Tax Loss Harvesting Works.

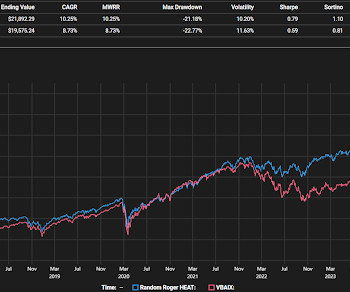

Adaptability is a great word for portfolio construction and ongoing management. I don't believe adaptability has to mean very actively trading a portfolio but there will be occasional trades that need to be made. My version of HEAT doesn't cherry pick themes from the portfolio, it's all of the holdings that I think are themes.

Early on in my savings journey I prioritized tax-deferred retirement accounts over all else. I like the ease and simplicity of 401k contributions coming out of my paycheck before it ever even touches my checking account. It’s easy to automate. The set-it-and-forget-it nature of a workplace retirement plan is one of my favorite features.

What to Do Instead: Stick to fundamentals: Learn about assetallocation, risk management, and diversification before investing. But many jump into stocks, crypto, or NFTs without understanding risk, diversification, or assetallocation.

Let’s look at a few of the starting points today for a healthy retirement savings portfolio. Set Up Another Retirement Account Individual Retirement Accounts (IRAs) may offer tax advantaged savings as well. Contributions are taxed on the way in with these accounts. A Roth IRA offers tax free withdrawals on taxable contributions.

Review risk tolerance and current assetallocation strategy It’s important to ensure your clients’ portfolios align with their risk tolerance because taking too much risk can negatively impact their ability to navigate market fluctuations. This shift would have resulted in a riskier portfolio with increased volatility.

Advisors are being asked to provide their clients with a full suite of solutions, ranging from estate and tax planning to portfolio management, and everything in between. Clients are increasingly eager to gain access to fully customizable solutions that meet their individual needs.

Lessons to learn to get better value from your wealth manager We onboarded a client with a portfolio of around INR 50 Crores, earlier managed by a big & reputed wealth management company. The portfolio was constructed for retirement purposes with 12 years of investment horizon. 40% allocation in AIFs and 20% average in debt.

Fee-Only, Flat-Fee Financial Planners: Transparent, Unbiased, and Cost-Effective A fee-only financial planner charges a fixed fee for financial planning services, regardless of the size of your portfolio. Unlike AUM advisors, they dont have an incentive to keep assets under management, so their recommendations are truly objective.

But what does this mean for your portfolio, and how can you continue to protect and grow your assets during these times? How Volatility Affects Investment Returns Volatility can send the value of your portfolio on an uncomfortable roller coaster ride. You can also further diversify within an asset class.

Tariffs are, essentially, taxes imposed on imported goods. Diversifying portfolios across asset classes, sectors, and geographies to reduce concentrated risks. Diversifying portfolios across asset classes, sectors, and geographies to reduce concentrated risks. And should we be concerned?

So how do you then go from tax and audit practice to finance and investing? But what was interesting about that was the quick need to both separate the portfolio between the old stuff and the new stuff, because there were a lot of new investment opportunities. So you’re Chief Investment officer of Asset and Wealth Management.

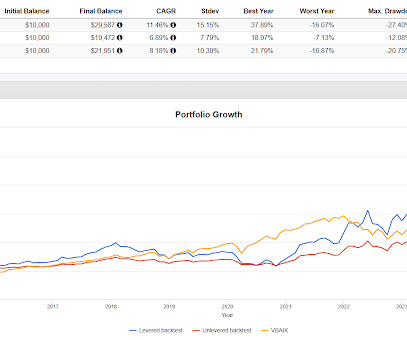

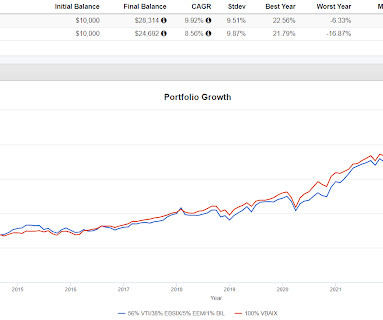

Torsten Slok blogged about how ineffective bonds have been in terms of providing any return or diversification benefits lately in the context of a 60/40 portfolio. Based on the following excerpt; I built out the following leveraged allocation, taking some liberty with shortening the duration quite a bit.

First up was a webinar about model portfolios at ETF.com. Outsourcing the work related to actually being an advisor would not feel right to me and I enjoy what I get to do including portfolio construction. I think that when investors hear about model portfolios they sort of think in terms of set and forget.

CIO Perspectives Webinar, 2022 AssetAllocation Outlook mhannan Fri, 03/18/2022 - 06:42 Markets have been unsteady at the start of 2022, driven by geopolitical tensions, inflation, and concerns about equity valuations. Brown Advisory does not render legal or tax advice. The war in Ukraine is causing even more uncertainty.

CIO Perspectives Webinar, 2022 AssetAllocation Outlook. Our CIOs recently discussed current market conditions, how we are positioning portfolios, and an array of other topics such as major trends in technology across public and private markets, inflationary dynamics, sustainable investing, the outlook for China, and more.

The Roth Man himself, Bill Sweet, joined me on the show this week to discuss questions about taxes in marriage, retirement withdrawal strategies, the tax implications of selling farmland and how to manage tax rates in early retirement.

Consequently, the portfolioallocation should reflect these probabilities depending on the risk profiles. Therefore, we maintain our underweight position to equity (check the Model Portfolio Current assetallocation below). One can consider debt portfolios with floating rate instruments for long-term allocation.

Today, we’re excited to announce we’re releasing updated assetallocations for all of our Automated […] The post Wealthfront’s Portfolios Are Now Even More Tax-Optimized appeared first on Wealthfront Blog. As part of that commitment, we are always looking for opportunities to help you earn more and keep more.

Rebalancing your 401(k) and investment portfolio is an important part of a successful investment strategy. Your assetallocation is the percentage of your portfolio that you distribute between different asset classes, like stocks and bonds. Why do you need to rebalance your portfolio? Why does this matter?

An endowment is a portfolio of assets that is invested to provide support for a cause. Donations to endowment funds are tax-deductible, giving them a place in your overall financial management and tax plan. An endowment offers benefits that can extend beyond tax deductions and financial efficiency.

A financial advisor can help navigate the complexities of wealth management, from tax considerations to estate planning and retirement strategies. Their role extends beyond investment managementthey can help with: Retirement Planning : Structuring your assets to support your desired lifestyle. Ready to Grow Your Wealth?

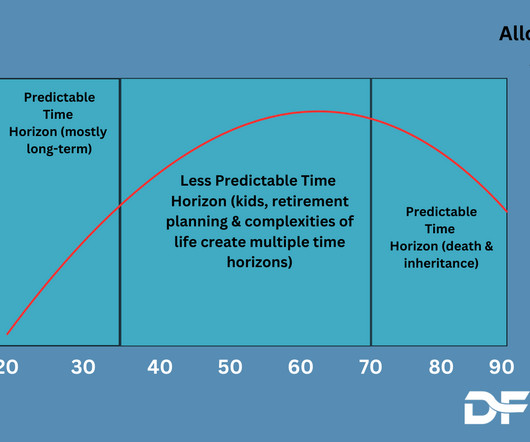

When it comes to assetallocation the old rule of thumb is roughly “your age in bonds” The basic thinking is that you should get more conservative as you get older. I am a big fan of boring ETFs because I think assetallocation should be boring. Assetallocation should be mostly boring.

I would describe the paper as seeking how to use low volatility equities in various ways to replace some or all of a traditional 60% equities/40% bonds portfolio. The first example to look at they call Leverage In The Strategic AssetAllocation via this table in the paper. The results here are consistent with the paper.

FINANCIAL PLANNING What is Portfolio Rebalancing? Investments can be risky since markets constantly fluctuate, but strategies are available to help you maintain a well-balanced portfolio. When people buy and sell sections of their portfolio to maintain a consistent assetallocation, they are rebalancing their investments.

When investing in a 401(k), one of the most important decisions you can make is how often to rebalance your portfolio. Rebalancing involves adjusting the mix of assets in your 401(k) portfolio to maintain a desired level of risk and return. This article will explore how often to rebalance your 401(k). Need a financial advisor?

A portfolio with an enormous weighting to one or two broad based factors is not really what I do but it clearly can work but just like any other strategy you can find, it won't always be optimal. Speaking of AI, Grok seems to like the portfolio. Its 10% SHRIX allocation adds high-yield, low-correlation income, but event risk looms.

The starting point today is the that Rational ReSolve Adaptive AssetAllocation Fund (RDMIX) has gone through a strategy change, renaming as the ReturnStacked Balanced Allocation & Systematic Macro Fund and keeping the same symbol. " balanced allocation and $1 of exposure to a systematic macro strategy."

I stumbled into some content about model ETF portfolios including one interesting portfolio that was comprised of ETFs that I'd mostly never heard of. It was impressive that the portfolio was not just a collection of the largest Vanguard, iShares or Schwab ETFs. The above goes back to GHTA's inception.

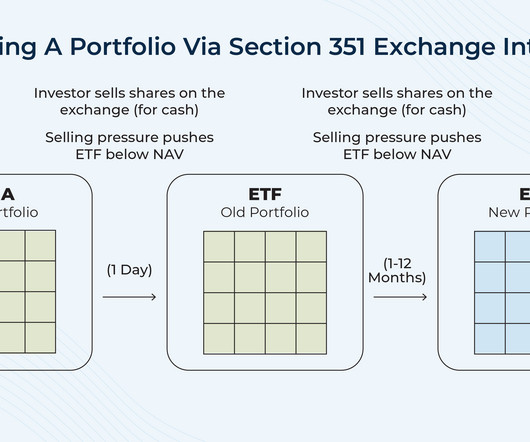

If you have a taxable portfolio of at least $1 million where selling or rebalancing would hit very hard tax-wise, you can exchange your portfolio for shares in a 351 ETF. Based on Cambria's other multi-asset funds, ENDW will probably have fixed income duration but that's a space I will continue to avoid. The results.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content