This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

By Jake Anderson, CFP ® , Wealth Planner When helping clients begin retirementplanning, the same questions often arise: What should my retirementplan look like? Your lifestyle, goals, family situation, and risk tolerance will give a unique signature to your retirementplan. How much should I be saving?

Also in industry news this week: While an infusion of Private Equity (PE) capital has shaken up the RIA M&A market, the ultimate implications for advisors, their clients, and the PE firms themselves remain unclear A recent study has found that a significant portion of 'DIY' investors are open to working with a human advisor (and paying for the (..)

Retirementplanning is a critical part of financial security that many women still overlook. However, remember that as a woman, you have a longer life expectancy than a man, which means retirementplanning is even more important. Retirementplanning is an important part of financial security for women.

Financial advisors have a wide range of strategies at their disposal to create financial plans for their clients. And when it comes to retirementplanning, one popular technique is the use of ‘guardrails’, which set an initial monthly withdrawal rate that can be later adjusted as the size of the client’s portfolio changes.

I've talked about my assetallocation before being overwhelmingly in cash or cash proxies, about 25% in "normal" equity investments, my exposure to crypto these days might be 2-3% up from 1/2 of a percent from when I bought Bitcoin in late 2018 but down from 6-7% when Bitcoin was higher.

Allocatingretirementplanning I introduce assetallocation with clients by dividing retirement life into two parts: basic life and high-quality life. After showing them that breakdown, I discuss the details of assetallocation. Chin-Lung Wang , Taipei City, Taiwan Area, 21-year MDRT member

Assuming that you have a financial plan with an investment strategy in place there is really nothing to do at this point. Ideally you’ve been rebalancing your portfolio along the way and your assetallocation is largely in line with your plan and your risk tolerance.

This is also what makes retirementplanning so difficult – you effectively lose an asset in your portfolio when your income stops or declines. And this is why I’ve become such a big advocate of defining our durations within our financial plans. You’re temporally diversified by your income.

Because of these differences, stocks and bonds accomplish different things in an assetallocation. Why stocks and bonds belong in a diversified portfolio Investors have different needs, risk tolerances, time horizons, and financial situations which should be considered in an assetallocation.

Last year’s considerable losses and market fluctuations underscore the need for clients to assess their retirementplans to ensure it aligns with their objectives, financial situations, timelines, and attitudes toward market volatility. You can help them start the year right by conducting a retirement checkup.

Living off dividends in retirement: hypothetical income today for portfolios between $2M and $15M Investors may wonder how much money they could expect in dividend income annually given today’s market. In another words, if your assetallocation is 60% stocks and 40% bonds, the current weighted average yield is 2.19%.

We emptied the inbox this week covering other questions about getting your CFA designation, the types of bonds you should own in retirement, how pensions fit into a retirementplan, how to spend more money, teaching your kids about money, becoming a landlord, using a HELOC as an emergency fund, how analysts rate stocks and adding international exposure (..)

Perhaps it’s time to rebalance and to rethink your ongoing assetallocation. Related Posts: Five Things to do During a Stock Market Correction Is a $100,000 Per Year Retirement Doable? Take stock of where you are. What impact have the solid stock market gains of the past three years had on your portfolio? Costs matter.

Has the market rally accelerated the amount you’ve accumulated for retirement relative to where you had thought you’d be at this point? If so, this is a good time to revisit your assetallocation and perhaps reduce your overall risk. Learn from the past . Photo credit: Phillip Taylor PT.

The set-it-and-forget-it nature of a workplace retirementplan is one of my favorite features. I like the ease and simplicity of 401k contributions coming out of my paycheck before it ever even touches my checking account. It’s easy to automate. Plus, I like the fact that it’s difficult to get the money out of these ac.

Unlike AUM advisors, they dont have an incentive to keep assets under management, so their recommendations are truly objective. Comprehensive Financial Planning is Included Many AUM advisors charge extra for estate planning, tax strategies, and retirementplanning. Are There Any Benefits to AUM-Based Advisors?

But volatile markets aren’t necessarily a negative thing, especially when it comes to retirementplanning. When you are planning for retirement, a lost decade can mean stagnated savings and loss of buying power to inflation. Target Date Funds Can Help AssetAllocation.

Decide upon your assetallocation The first step in investing your 401(k) is determining your “assetallocation,” which is simply the mix of stocks, bonds and cash you’ll hold. This mix of assets is the main building block of your portfolio and will primarily determine the risk and return in the account.

Learn how our industry-leading assetallocation expertise can help participants make investment choices with more confidence and help employers reach their plan goals. Advice boosts workers’ confidence in choosing investments—from 35% to 65%.

Your assetallocation is the percentage of your portfolio that you distribute between different asset classes, like stocks and bonds. To rebalance your portfolio, you’ll buy and sell certain investments to realign to your accounts with your desired assetallocation.

Offer more ways clients may achieve their retirementplan goals while helping address the diverse investment needs of participants. Learn about our industry-leading investments and expertise—featuring more default options and more personalized assetallocation.

Circling back to model ETF portfolio mentioned at the top of this post, the assetallocation was as follows. US Equity 56% Trend Following/Tactical 38% Emerging Market Equity 5% Cash 1% I don't know often that changes but that there is not a permanent allocation to fixed income is of course intriguing to me.

We talk both retirementplanning and factor investing with Dimensional Fund Advisors Senior Researcher Mathieu Pellerin. The post Factor Investing for Retirement with DFA’s Mathieu Pellerin appeared first on Validea's Guru Investor Blog. In this episode, we combine two of the topics we often cover on the podcast.

We talk both retirementplanning and factor investing with Dimensional Fund Advisors Senior Researcher Mathieu Pellerin. The post Factor Investing for Retirement with DFA’s Mathieu Pellerin appeared first on Validea's Guru Investor Blog. In this episode, we combine two of the topics we often cover on the podcast.

just upended retirementplanning…again. The age when retirees must begin drawing from non-Roth retirement accounts increases to 73 in 2023, then 75 in 2033. Raising the age when withdrawals must begin is great as it gives investors more planning opportunities. The Secure Act 2.0

A point we've been making here for ages is that with an adequate savings rate, appropriate assetallocation and the ability to avoid succumbing to panic, an investor should be able to have retirementplan success as defined above.

Take Advantage of RetirementPlans and Matching Contributions. Most employer retirementplans allow you to save on a tax-deferred basis, meaning that contributions into these types of accounts are not considered in calculating your taxable income. . Determine an Appropriate Risk Tolerance for a Longer Time Horizon .

Edzai and Franklin will cover a wide range of essential topics including managing student debt, understanding employer-provided benefits, retirementplanning fundamentals, holistic assetallocation for tax-efficient returns, risk management, and asset protection strategies.

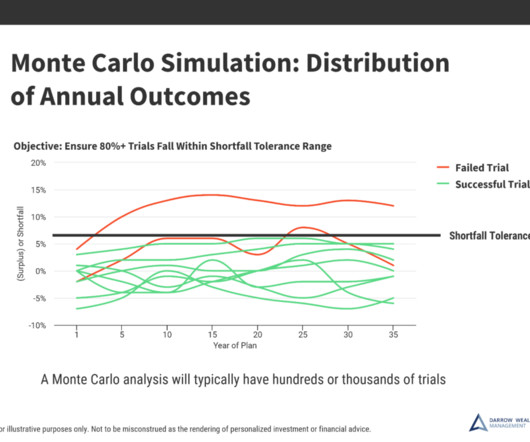

Don’t stress out about every headline, stress test your retirementplan instead.Markets move every day and the news cycle is 24-7. Even if actual average returns meet targets over time, market volatility can still derail your portfolio and retirementplans. This produces a probability of success across all trials.

AssetAllocation and Goals. We are big advocates of time based assetallocation. This means you should try to create specific buckets for your portfolio where you’re matching future expenses and liabilities to specific corresponding assets. RetirementPlanning Review your retirement goals and objectives.

As you get closer to retirement your assetallocation should change. Additionally, be sure to account for the tax confusions of different investments in taxable brokerage accounts and retirement accounts. Maximize Social Security Benefits Social Security is a major part of your retirementplan.

Investment strategy: Determine assetallocation and investment vehicles aligned with risk tolerance and financial goals. Retirementplanning: Calculate retirement needs and contribute regularly to retirement accounts.

Maintaining an appropriate assetallocation for an investor’s specific goals and risk tolerance is critical for long-term success. There’s value in staying invested in that assetallocation and not trying to time the market’s ups and downs or succumbing to fear when markets turn tumultuous.

The first example to look at they call Leverage In The Strategic AssetAllocation via this table in the paper. The paper introduces the idea of mixing momentum and value in some combo that they never quantified as a possible substitute for low volatility before digging in more deeply into different examples or cases.

Right or wrong, I think of endowment style investing as being a similar to the Permanent Portfolio, not so much quadrants but more like disparate asset class segments which gets us to a paper about endowment assetallocation from True North Institute.

The starting point today is the that Rational ReSolve Adaptive AssetAllocation Fund (RDMIX) has gone through a strategy change, renaming as the ReturnStacked Balanced Allocation & Systematic Macro Fund and keeping the same symbol. " balanced allocation and $1 of exposure to a systematic macro strategy."

If all you use is a broad index fund then it will either be a good year or not so good, but assuming the proper assetallocation, who cares? That's enough to get it done assuming an adequate savings rate, appropriate assetallocation and no panicking.

Earning the CFP designation requires a rigorous course of study covering investment planning, income taxation, retirementplanning and risk management. A Person who completes the CFP course is qualified to provide financial planning services to those with a high degree of financial responsibility.

The simple answer is that the short-term movements of the stock market should be irrelevant to your financial plan assuming you have a well constructed temporally diversified portfolio. 5-15 years: moderately long-term needs like near retirementplanning, a child’s college tuition, etc. 2) Stock market gambling.

The contributions made to the account may be tax-deductible or non-deductible, depending on the individual’s income level and participation in an employer-sponsored retirementplan. The deductibility of contributions depends on the individual’s income level and participation in an employer-sponsored retirementplan.

Of course, one of the most important aspects of retirementplanning is managing retirement taxes. Taxes can significantly impact the amount of money you’ll have for retirement. These factors, of course, can also impact the taxes due in retirement. Income levels, tax deductions, and credits can change yearly.

Of course, one of the most important aspects of retirementplanning is managing retirement taxes. Taxes can significantly impact the amount of money you’ll have for retirement. These factors, of course, can also impact the taxes due in retirement. Income levels, tax deductions, and credits can change yearly.

The Wall Street Journal took what might be a sympathetic approach to 401k investors who might be feeling disillusioned by generally poor performance with the focus being on target date funds which have of course become a major staple of 401k plans. First, it's your retirement, how do you not care enough to engage just a little?

I've been critical of the actual FIG ETF, the Simplify Macro ETF, it is really struggling but I think the fund's idea for assetallocation works for the most part. We don't spend a ton of time talking about Sharpe Ratios but yikes, that is a huge difference for the same assetallocation.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content