This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Retirementplanning is a critical part of financial security that many women still overlook. However, remember that as a woman, you have a longer life expectancy than a man, which means retirementplanning is even more important. Consider early retirementtaxplanning. Educate yourself about finances.

I've talked about my assetallocation before being overwhelmingly in cash or cash proxies, about 25% in "normal" equity investments, my exposure to crypto these days might be 2-3% up from 1/2 of a percent from when I bought Bitcoin in late 2018 but down from 6-7% when Bitcoin was higher.

So historically, every $1 million invested would yield annual dividend income of $19,800 on average… before tax. If you own 10,000 shares, you receive $40,000 in dividend income (before taxes) and have a portfolio currently worth $2M. Over the last 30 years, the S&P 500’s average dividend yield was 1.98%.

Last year’s considerable losses and market fluctuations underscore the need for clients to assess their retirementplans to ensure it aligns with their objectives, financial situations, timelines, and attitudes toward market volatility. You can help them start the year right by conducting a retirement checkup.

Because of these differences, stocks and bonds accomplish different things in an assetallocation. Taxes, fees, expenses, trading costs, etc. As economic conditions and income needs change, so too will your assetallocation. When you own a stock, you’re buying a piece of equity ownership in the company.

Early on in my savings journey I prioritized tax-deferred retirement accounts over all else. The set-it-and-forget-it nature of a workplace retirementplan is one of my favorite features. I like the ease and simplicity of 401k contributions coming out of my paycheck before it ever even touches my checking account.

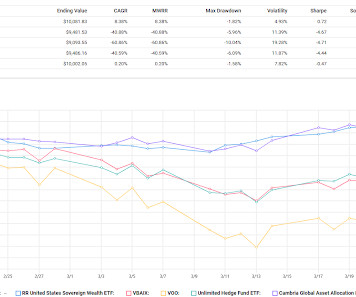

One of the pre-market Bloomberg emails gave a positive mention to the Cambria Global AssetAllocation ETF (GAA) because it is up in what of course has been a tough tape for equities this year. It is an interesting assetallocation that targets 40% in equities, 40% in fixed income and 20% in alternatives.

Published: March 21st, 2025 Reading Time: 6 minutes Written by: The Zoe Team Managing wealth involves more than just investingit requires careful planning, strategic decision-making, and a long-term vision. Tax Considerations : Identifying strategies to optimize your tax situation. Optimizing tax-efficient retirement income.

This article will discuss the key features of the Microsoft 401(k) plan, and after reading it, you should leave with a clear game plan of how to: Maximize the match (free money! ) The key benefits of any 401(k) plan (including Microsoft’s) include: Free Money : A company match on your contributions.

Unlike AUM advisors, they dont have an incentive to keep assets under management, so their recommendations are truly objective. Comprehensive Financial Planning is Included Many AUM advisors charge extra for estate planning, tax strategies, and retirementplanning.

Of course, one of the most important aspects of retirementplanning is managing retirementtaxes. Taxes can significantly impact the amount of money you’ll have for retirement. As such, you must be aware of any tax implications arising from your investments during your working years.

Of course, one of the most important aspects of retirementplanning is managing retirementtaxes. Taxes can significantly impact the amount of money you’ll have for retirement. As such, you must be aware of any tax implications arising from your investments during your working years.

Your assetallocation is the percentage of your portfolio that you distribute between different asset classes, like stocks and bonds. To rebalance your portfolio, you’ll buy and sell certain investments to realign to your accounts with your desired assetallocation.

The assetallocation was 10% to hedges, 30% to T-bills for asymmetry but that seems more like optionality to me, 9% to edges which included one broad stock picking ETF, a derivative income fund and a short volatility product. None of them were hideously wrong out of the blocks but it's too soon to declare victory with them.

An individual who learns to manage $4,000 a month after taxes will be equipped to manage $14,000 or even $40,000 a month as their earnings increase over time. Take Advantage of RetirementPlans and Matching Contributions. Employers often match a portion of this contribution to a retirementplan as an employer benefit. .

Rebalancing a 401(k) refers to adjusting the assetallocation of your investment portfolio back to its original target percentages. Your investment strategy determines the target percentages for each asset, often based on your risk tolerance, investment goals, and time horizon. Click to compare vetted advisors now.

Right or wrong, I think of endowment style investing as being a similar to the Permanent Portfolio, not so much quadrants but more like disparate asset class segments which gets us to a paper about endowment assetallocation from True North Institute.

The first example to look at they call Leverage In The Strategic AssetAllocation via this table in the paper. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation. These are easy to model. The results here are consistent with the paper.

The starting point today is the that Rational ReSolve Adaptive AssetAllocation Fund (RDMIX) has gone through a strategy change, renaming as the ReturnStacked Balanced Allocation & Systematic Macro Fund and keeping the same symbol. " balanced allocation and $1 of exposure to a systematic macro strategy."

Circling back to model ETF portfolio mentioned at the top of this post, the assetallocation was as follows. US Equity 56% Trend Following/Tactical 38% Emerging Market Equity 5% Cash 1% I don't know often that changes but that there is not a permanent allocation to fixed income is of course intriguing to me.

These professionals meticulously assess your financial situation, income level, and retirement goals to tailor personalized strategies. For instance, they can guide you on leveraging employer-sponsored retirementplans, such as a 401(k) with employer matches, to optimize your contributions and harness the full benefits of the accounts.

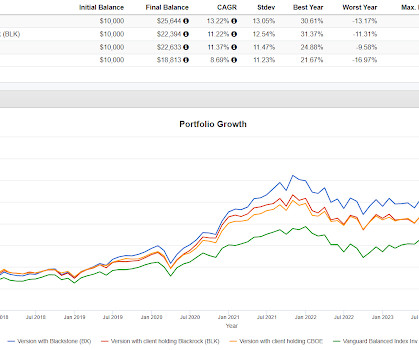

If you have a taxable portfolio of at least $1 million where selling or rebalancing would hit very hard tax-wise, you can exchange your portfolio for shares in a 351 ETF. Based on Cambria's other multi-asset funds, ENDW will probably have fixed income duration but that's a space I will continue to avoid. The results.

Barron's had an interesting article about a BofA study showing that over a period of many decades an assetallocation of 60% equities/40% commodities outperformed an allocation of 60% equities/40% fixed income by 0.80% per year.

You can also get information on your performance and assetallocation. This will help you to create an assetallocation that will get you where you need to go with your investments. It can be used to help you with your assetallocation, at least based on the investment options that your plan includes.

Edzai and Franklin will cover a wide range of essential topics including managing student debt, understanding employer-provided benefits, retirementplanning fundamentals, holistic assetallocation for tax-efficient returns, risk management, and asset protection strategies.

There's no fact sheet yet and while the holdings are available, the assetallocation is vague without calculating the spreadsheet yourself which I did (hopefully correctly). They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation.

The prompt was a mention of the Cambria Global AssetAllocation ETF (GAA) somewhere and since the market has done so poorly, I though it would be worth revisiting. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation.

I found their assetallocation and wanted to see from the top down if there's a way to mimic them to some extent and get decent results. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation. A few different things today.

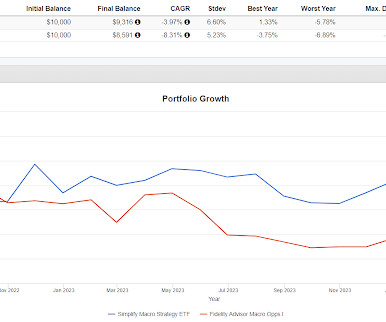

I've been critical of the actual FIG ETF, the Simplify Macro ETF, it is really struggling but I think the fund's idea for assetallocation works for the most part. We don't spend a ton of time talking about Sharpe Ratios but yikes, that is a huge difference for the same assetallocation.

A crucial point of understanding for navigating any sort of adverse market event regardless of whether there is visibility for it or if it comes out of left field is to have the proper assetallocation for your circumstance. Then it really doesn't matter at all what the stock market does over the next little bit.

Increasing the RMD age to 75 will change quite a few aspects of this part of retirementplanning. Obviously any money not put into an IRA loses the benefit of tax deferred compounding. I've mentioned several times that I was test driving Rational/Resolve Adaptive AssetAllocation Fund (RDMIX) for possible use in client accounts.

FIG is not intended to negatively correlate to markets, they want it to be "a modern take on the balanced portfolio, built to help navigate today’s toughest assetallocation challenges." They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation.

James and Pamela’s Big Dream Excerpt from The Smart Person’s Guide to Financial Planning & Investments: A Simple and Straightforward Approach to Understanding Your Personal Finances By Michael J. Their retirementplan is strong, their kids are independent, and they are debt-free.

Long-term goals typically encompass retirementplanning, wealth preservation and estate planning. Your risk tolerance will influence your investment strategy and assetallocation. Tax Considerations Be mindful of tax implications related to your goals.

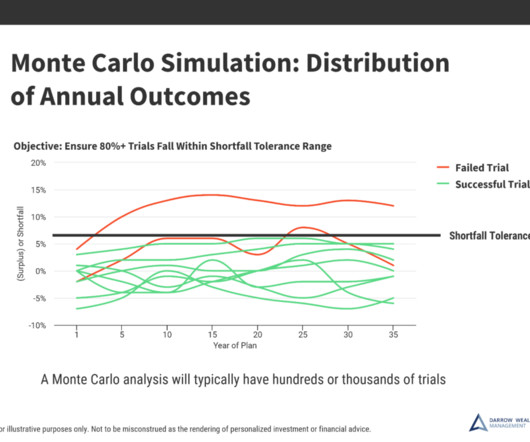

Don’t stress out about every headline, stress test your retirementplan instead.Markets move every day and the news cycle is 24-7. Even if actual average returns meet targets over time, market volatility can still derail your portfolio and retirementplans. This produces a probability of success across all trials.

Several talked about tax issues, it is important to keep tabs on how taxes might change going forward and then when they actually do change. Yes on the taxes but without earned income and living on long term capital gains from an investment portfolio, there might be no income tax.

The answer lies in smart and strategic retirementplanning. Gone are the days when retiring at 60 was a one-size-fits-all goal. It’s time to rethink when to start stashing away those savings and how to modify your plan in a world that’s constantly changing. So, how do we tackle this?

Risk Tolerance: What is your assetallocation? If you are close to retirement, and you have too much exposure to equities, a retrenchment in the stock market could delay your retirementplans by years. This concept highlights the importance of rebalancing your portfolio as you get closer to retirement.

The course covers an introduction to personal finance, credit cards, life insurance, health insurance, investment instruments, loans, income tax and planning, budgeting and building a strong portfolio. Also, you will learn how to plan your taxes, credit score importance and how to budget your income to create a portfolio.

Reacting in the middle of 2022 after learning too much was allocated to risk assets? That person will be best off waiting for some portion of the recovery that will inevitably occur and then make their decision about assetallocation when there is less emotion at play.

From retirementplanning to market volatility, equity compensation, family expenses, and major life transitions, it’s easy to feel overwhelmed with financial responsibilities. An advisor can answer questions like: When can I fully retire? Here are 5 signs it might be time to hire a financial advisor.

Blogger Nomadic Samuel posted an interview with Jay Kaeppel who has an interesting spin on assetallocation with what he describes as 30/30/30/10. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation.

Long-term goals typically encompass retirementplanning, wealth preservation and estate planning. Your risk tolerance will influence your investment strategy and assetallocation. Tax Considerations Be mindful of tax implications related to your goals.

Per an email from Unlimited the fund is trying to offer "core, liquid, uncorrelated ballast within overall assetallocation." They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation. It's only been trading since late 2022.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content