This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

By Jake Anderson, CFP ® , Wealth Planner When helping clients begin retirementplanning, the same questions often arise: What should my retirementplan look like? Your lifestyle, goals, family situation, and risk tolerance will give a unique signature to your retirementplan. How much should I be saving?

Financial advisors have a wide range of strategies at their disposal to create financial plans for their clients. And when it comes to retirementplanning, one popular technique is the use of ‘guardrails’, which set an initial monthly withdrawal rate that can be later adjusted as the size of the client’s portfolio changes.

Retirementplanning is a critical part of financial security that many women still overlook. However, remember that as a woman, you have a longer life expectancy than a man, which means retirementplanning is even more important. Suppose you significantly reduce your stock investments close to or after retirement.

The idea of living off dividends in retirement sounds nice, but investors often don’t realize how much money they’ll need invested to generate enough income from dividends to cover lifestyle expenses. You may need more money than you think to retire on dividends. Retire on dividends?

Also in industry news this week: While an infusion of Private Equity (PE) capital has shaken up the RIA M&A market, the ultimate implications for advisors, their clients, and the PE firms themselves remain unclear A recent study has found that a significant portion of 'DIY' investors are open to working with a human advisor (and paying for the (..)

At 50 though, you do need to have some context for how viable your idea of retirement is. My reasoning is as it has always been, my income is levered to the ups and downs of the stock market, I don't ever want to retire, we have been living below our means for ages and now all the more so having just paid off our mortgage.

As someone saving for retirement , what should you do now? The PBS Frontline special The Retirement Gamble put much of the blame on Wall Street and they are right to an extent, especially as it pertains to the overall market drop. If so, this is a good time to revisit your assetallocation and perhaps reduce your overall risk.

Assuming that you have a financial plan with an investment strategy in place there is really nothing to do at this point. Ideally you’ve been rebalancing your portfolio along the way and your assetallocation is largely in line with your plan and your risk tolerance. Markets will always correct at some point.

Allocatingretirementplanning I introduce assetallocation with clients by dividing retirement life into two parts: basic life and high-quality life. After showing them that breakdown, I discuss the details of assetallocation. Chin-Lung Wang , Taipei City, Taiwan Area, 21-year MDRT member

Last year’s considerable losses and market fluctuations underscore the need for clients to assess their retirementplans to ensure it aligns with their objectives, financial situations, timelines, and attitudes toward market volatility. You can help them start the year right by conducting a retirement checkup.

Perhaps it’s time to rebalance and to rethink your ongoing assetallocation. Approaching retirement and want another opinion on where you stand? Financial coaching focuses on providing education and mentoring on the financial transition to retirement. Take stock of where you are. Costs matter. FINANCIAL WRITING.

1 With ever-increasing life expectancies, it’s no wonder 63% of American adults say they’re more afraid of running out of money in retirement than they are of death. 2 That’s why it’s vitally important to consider longevity risk when you’re planning for your financial needs in retirement. What Is Longevity Risk?

Because of these differences, stocks and bonds accomplish different things in an assetallocation. While an investor’s timeline affects their risk tolerance and allocation decisions between stocks and bonds, it’s important to remember how long a retirement time horizon can truly be.

This is also what makes retirementplanning so difficult – you effectively lose an asset in your portfolio when your income stops or declines. And this is why I’ve become such a big advocate of defining our durations within our financial plans. You’re temporally diversified by your income.

Early on in my savings journey I prioritized tax-deferred retirement accounts over all else. The set-it-and-forget-it nature of a workplace retirementplan is one of my favorite features. I like the ease and simplicity of 401k contributions coming out of my paycheck before it ever even touches my checking account.

Planning for retirement can seem premature when you have only been in the workforce for a decade or so. But as the oldest Millennials begin to hit middle age, retirement suddenly does not seem so far away. Here are five things Millennials should consider when planning for retirement. Free Money May Be Available.

As you would expect from an outstanding organization like Microsoft, it offers a very robust 401(k) to help employees save for retirement. This article will discuss the key features of the Microsoft 401(k) plan, and after reading it, you should leave with a clear game plan of how to: Maximize the match (free money! )

Unlike AUM advisors, they dont have an incentive to keep assets under management, so their recommendations are truly objective. Comprehensive Financial Planning is Included Many AUM advisors charge extra for estate planning, tax strategies, and retirementplanning. Are There Any Benefits to AUM-Based Advisors?

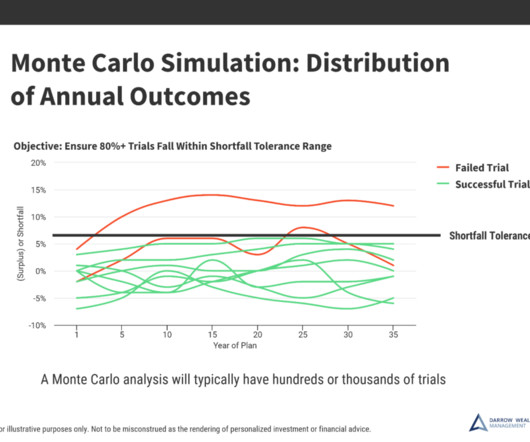

Don’t stress out about every headline, stress test your retirementplan instead.Markets move every day and the news cycle is 24-7. Stress testing a financial plan or retirement income goals is crucial to help ensure retirees wont run out of money under different conditions in the financial markets.

We talk both retirementplanning and factor investing with Dimensional Fund Advisors Senior Researcher Mathieu Pellerin. The post Factor Investing for Retirement with DFA’s Mathieu Pellerin appeared first on Validea's Guru Investor Blog. In this episode, we combine two of the topics we often cover on the podcast.

We talk both retirementplanning and factor investing with Dimensional Fund Advisors Senior Researcher Mathieu Pellerin. The post Factor Investing for Retirement with DFA’s Mathieu Pellerin appeared first on Validea's Guru Investor Blog. In this episode, we combine two of the topics we often cover on the podcast.

For people nearing retirement, these challenges can be even more daunting. A market downturn at the start of retirement, hitting portfolio values when retirees begin to take account withdrawals, can be unsettling, even for seasoned investors. Many near-retirees see their highest portfolio values just before retirement.

Learn how our industry-leading assetallocation expertise can help participants make investment choices with more confidence and help employers reach their plan goals. Advice boosts workers’ confidence in choosing investments—from 35% to 65%.

Barron's had a roundup of advisor advice for people who want to retire early. That might not sound like much income but the context here is being retired at a young age. This really is about having the right assetallocation. That much income, without Social Security or active income seems pretty good to me.

According to a survey, a significant majority of Americans, approximately 80%, share the common notion that the point of working hard in your adult life is so you can enjoy a nice retirement. After years of dedicated labor and hard work, the prospect of a peaceful retirement appeals to everyone.

We all know retirement is an important milestone that requires careful planning. Of course, one of the most important aspects of retirementplanning is managing retirement taxes. Taxes can significantly impact the amount of money you’ll have for retirement. This can be a mistake.

We all know retirement is an important milestone that requires careful planning. Of course, one of the most important aspects of retirementplanning is managing retirement taxes. Taxes can significantly impact the amount of money you’ll have for retirement. This can be a mistake.

Investment strategy: Determine assetallocation and investment vehicles aligned with risk tolerance and financial goals. Retirementplanning: Calculate retirement needs and contribute regularly to retirement accounts. What Could Happen if You Don’t Have a Financial Plan? Outliving their money.

Saving money is an important task at any age, but as you hit your 40s, the need to save for retirement grows. While savers in their 40s and 50s typically have a decade or two left to save for retirement given the traditional age of 65, emphasizing saving now can set you up for a dream-worthy retirement.

Market performance in the early years of retirement can greatly affect how long retirement funds will last, as losses can take a larger chunk out of a portfolio when it’s more flush. The first five years of retirement are crucial for figuring out a lifestyle that can sustain you for years to come. Utilize different assets.

just upended retirementplanning…again. The age when retirees must begin drawing from non-Roth retirement accounts increases to 73 in 2023, then 75 in 2033. Raising the age when withdrawals must begin is great as it gives investors more planning opportunities. The Secure Act 2.0

These are all interesting and important questions, but preparation for retirement is much more important than panicking over issues you have no control over. For many investors, however, the more important questions to ask and answer relate to your retirement strategy. Risk Tolerance: What is your assetallocation?

In our planning with clients, we like to employ a “pay yourself first” approach, especially as it relates to retirementplanning. This cycle can repeat itself over multiple years, resulting in minimal or no retirement savings. Planning for retirement is a multi-step process with continuous updates and monitoring.

Your assetallocation is the percentage of your portfolio that you distribute between different asset classes, like stocks and bonds. To rebalance your portfolio, you’ll buy and sell certain investments to realign to your accounts with your desired assetallocation.

Take Advantage of RetirementPlans and Matching Contributions. Most employer retirementplans allow you to save on a tax-deferred basis, meaning that contributions into these types of accounts are not considered in calculating your taxable income. . Consider the following example below:?? .

This conversation drifts into the academic realm a little but raises an interest question about how much or how little alpha does the typical person who saved for retirement, trying to make it through and maybe leave a little bit for their kids actually need? The person has been retired the whole time. million to do so and have $1.3

A Contributory IRA, otherwise known as a traditional IRA , is a retirement savings account that allows individuals to make contributions from their earned income. The contribution limit may be reduced or eliminated for individuals who have high incomes or who participate in an employer-sponsored retirementplan.

Offer more ways clients may achieve their retirementplan goals while helping address the diverse investment needs of participants. Learn about our industry-leading investments and expertise—featuring more default options and more personalized assetallocation.

In a world where the cost of living is steadily climbing and market uncertainties loom large, the idea of a serene retirement can seem like a distant dream. But let’s face it: the importance of saving for retirement hasn’t waned; if anything, it’s become more crucial. When to start saving for retirement?

AssetAllocation and Goals. We are big advocates of time based assetallocation. This means you should try to create specific buckets for your portfolio where you’re matching future expenses and liabilities to specific corresponding assets. RetirementPlanning Review your retirement goals and objectives.

The Wall Street Journal took what might be a sympathetic approach to 401k investors who might be feeling disillusioned by generally poor performance with the focus being on target date funds which have of course become a major staple of 401k plans. First, it's your retirement, how do you not care enough to engage just a little?

When you shift towards retirement your time horizon and risk profile shifts to a more conservative position. You can’t be fully invested in stocks when you’re nearing retirement because that creates enormous sequence of return risk. 1 He said that a real return of 8% means that rules like the 4% rule are silly.

A crucial point of understanding for navigating any sort of adverse market event regardless of whether there is visibility for it or if it comes out of left field is to have the proper assetallocation for your circumstance. Then it really doesn't matter at all what the stock market does over the next little bit.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content