This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Benefits of working with an independent fiduciary advisor Independence is important when seeking financial advice. Advisors affiliated with a bank, broker dealer, or large asset manager might not be able to make a fully independent recommendation. Only registered investment advisors have a full-time fiduciaryduty to their clients.

They exist in all fee models, whether they be commissions, assets under management, fixed fee, or hourly. Conflicts are everywhere in financial planning. Any time money changes hands there are conflicts of interests.

Although some firms use these compensation methods, the majority base fees on a percentage of assets under management (AUM) for their services. Fee-only firms are unique as they do not receive commissions from selling financial products, such as insurance policies or investment products.

Advisors have different fee structures where you can hire their services on an hourly rate, a retainer basis, or the assets under management (AUM) model where the advisor is paid a certain percentage as fee based on the amount of assets managed by him on behalf of his clients.

These professionals work with wealthy people, helping them manage their assets and offering related financial assistance. They register with the United States Securities and Exchange Commission ( SEC ) to gain the designation. . Some advisors do not observe fiduciaryduty but are bound to a suitability standard.

It requires not just sophisticated skill-set for asset allocation calls (across asset classes, sub-categories, and schemes), the temperament to keep emotions under check but also an ability to quickly understand the impact of the latest market developments (global and domestic) on various asset classes in a rapidly-changing world.

Fee-Only financial advisors are most often compensated as a percentage of assets (AUM), though also may be paid hourly, as a retainer, or as a flat fee, depending upon the planner you choose. Fee-Only financial advisors , on the other hand, do not receive commissions and are compensated through a fee-for-service model.

Fee-Only financial advisors are most often compensated as a percentage of assets (AUM), though also may be paid hourly, as a retainer, or as a flat fee, depending upon the planner you choose. Fee-Only financial advisors, on the other hand, do not receive commissions and are compensated through a fee-for-service model.

They charge either a percentage of assets managed or a flat hourly rate that can run as high as several hundred dollars per hour, plus trading commissions and administrative fees. They are salespeople paid to push products, earning commissions and kickbacks when they do. This is huge! And, that’s it.

Your risk tolerance will influence your investment strategy and asset allocation. When researching wealth management firms, paying attention to their credentials and qualifications is essential, including whether they have a fiduciaryduty to uphold. Advisors charge a percentage of your total assets that they manage.

Legal definition of the fiduciary standard To quote directly from a paper by Attorney Lorna Schnase , two bodies of law form the legal basis for the fiduciary standard: Common law: Under common law principles of agency, an investment adviser, as agent, owes fiduciaryduties to its client, as principal.3

Fee-only financial advisors Average cost: $200 to $400 an hour/ $1,000 to $3,000 per plan/ 1.18% to 0.59% of AUM Fee-only financial advisors are professionals who do not receive commissions from selling financial products. Instead, they charge fees directly to their clients for the services they provide.

These pre-packaged investments usually feature assets connected to interest and an additional. Securities and Exchange Commission. more of the core assets’ performance instead of the cash flow of the entity issuing the structured. Structured products help investors in accessing asset classes and additional benefits that might.

Your risk tolerance will influence your investment strategy and asset allocation. When researching wealth management firms, paying attention to their credentials and qualifications is essential, including whether they have a fiduciaryduty to uphold. Advisors charge a percentage of your total assets that they manage.

Larger asset managers have been able to build fairly passive approaches to ESG integration, where indexes or portfolios with low active share are “tilted” to emphasize holdings with lower reported carbon emissions or other desired ESG metrics. 1 Isn’t this a fiduciary’s responsibility, over the long term, to its pension beneficiaries?

Larger asset managers have been able to build fairly passive approaches to ESG integration, where indexes or portfolios with low active share are “tilted” to emphasize holdings with lower reported carbon emissions or other desired ESG metrics. 1 Isn’t this a fiduciary’s responsibility, over the long term, to its pension beneficiaries?

Larger asset managers have been able to build fairly passive approaches to ESG integration, where indexes or portfolios with low active share are “tilted” to emphasize holdings with lower reported carbon emissions or other desired ESG metrics. 1 Isn’t this a fiduciary’s responsibility, over the long term, to its pension beneficiaries?

Do advisors breach fiduciaryduty when they fail to recommend annuities? Should those with only insurance licenses that allow them to sell annuities and/or life insurance be held to the same “fiduciary standard” as Registered Investment Advisers (RIAs) with the SEC or state regulators? Are commissions bad?

BARRY FLAGG OR STEVEN ZEIGER: That’s what really makes paralytic so easy, because overly benchmarks illustration against the life insurance industry benchmarks, and you can easily see where you fall along continuum by my costs are lower than everyone else’s… Great, let’s party.

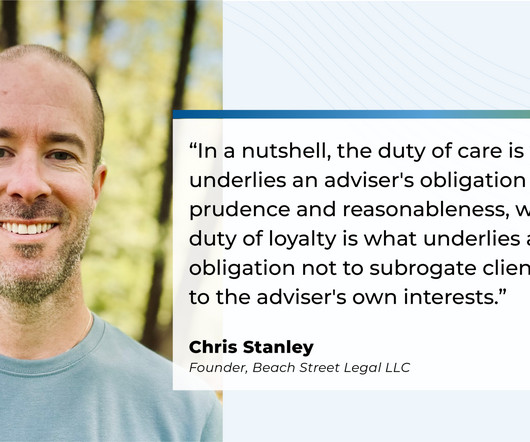

While this requirement might sound relatively straightforward, the lack of a single definition for what this duty actually requires can make it challenging for advisers seeking to understand precisely what it means to comply with this responsibility. Read More.

And so I would see how the over-the-counter desk, over-the-counter stock desk would push stocks and encourage brokers to sell them, put a lot of commission in them, to move them because some big seller was coming into the market. Or should this be kept out of private asset allocators’ hands? RITHOLTZ: Right. Kind of a thing.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content