This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

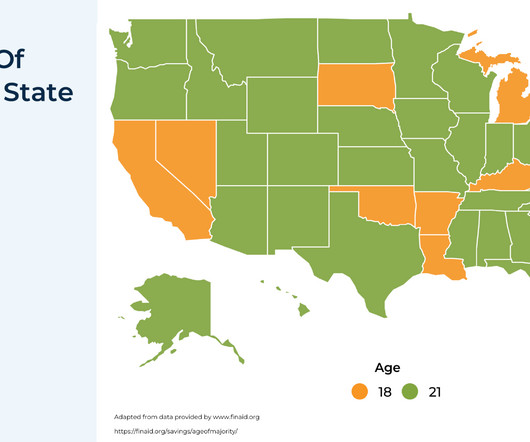

To achieve this, financial support may start at a very young age, allowing for a longer growth horizon and, in many cases, serving tax and estateplanning purposes. However, once a child reaches the age of majority, they may not always be in a position to manage assets responsibly.

The role of estateplanning is most commonly considered to be about transferring assets from one generation to the next in the most efficient manner possible (e.g., how to minimize the burden of estate taxes and avoid the public spectacle of the probate process). at age 21 or 30) or stagger distributions at multiple ages.

The role of estateplanning is most commonly considered to be about transferring assets from one generation to the next in the most efficient manner possible (e.g., how to minimize the burden of estate taxes and avoid the public spectacle of the probate process). at age 21 or 30) or stagger distributions at multiple ages.

morningstar.com) The biz Creative Planning was able to retain some 60% of the United Capital assets. riabiz.com) XY Planning Network is launching a new in-house RIA, XYPN Sapphire. obliviousinvestor.com) Estateplanning Changing an estateplan takes time. billion in donor-recommended grants in 2023.

One of the most important decisions you’ll make when designing your estateplan is who to name in the various fiduciary roles: trustee, personal representative, executor and agent. While a critical decision, it’s often given significantly less thought than the distribution of your assets.

Irrevocable trusts lie at the heart of a variety of estateplanning strategies, as gifts to irrevocable trusts can allow for the transfer of assets outside of an owner’s estate for estate tax purposes with more structure than an outright gift. the assets' original owner). the assets' original owner).

Estateplanning can be difficult to think about, let alone plan for. Maybe you’ve avoided putting together a concrete plan because you don’t want to think too far into the future when it’s time to pass on what you have. Or maybe you don’t think an estateplan is necessary because you’re not rich enough to warrant one.

Understand the basics first, and then create an estateplan. Wills and trusts are both important estateplanning tools with important differences. A will ensures property is distributed after your passing, according to your wishes, while a trust goes into effect as soon as you create it. A Will vs. a Trust.

Fortunately, financial professionals have tools and wealth transfer strategies that can help couples be intentional about the use of their assets in an estateplan. Why Focus on EstatePlanning for Blended Families A thoughtful plan and good communication can go a long way in heading off conflict in large families.

HSAs give you an upfront deduction for the year of contribution, grow tax-free, and distribute tax-free, making them one of the most powerful tax-advantaged accounts. Consider 529 Plans A 529 Plan is a tax-advantaged investment account specifically designed to fund education costs.

EstatesEstatePlanning in this Economic Climate Schedule a Complimentary Financial Review CLICK HERE TO SCHEDULE. If you are in the middle of estateplanning , consider the following strategies to develop a sound plan amidst widespread economic challenges. . Create a Trust .

Provisions of the SECURE Act may require advisors to revisit estateplans for clients who aren't utilizing their RMDs or who have qualified assets intended for the next generation. Some clients may benefit from strategies for using life insurance to maximize the value of qualified assets while minimizing their tax burden.

While a financial plan focuses on managing your finances during your lifetime, an estateplan is essential for determining the fate of your assets after you pass away. Estateplanning involves the transfer of your assets to your heirs in the event of your passing.

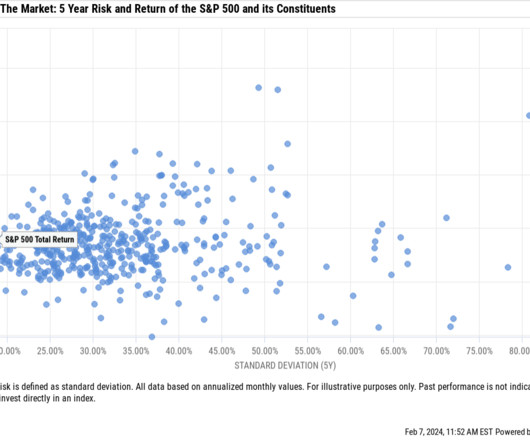

If one stock makes up more than 10% of your overall asset allocation, it’s probably too much. When considering the distribution of excess lifetime returns of individual stocks vs the Russell 3000, the median stock underperformance was almost -10%.(J.P. What is a concentrated stock position?

The Imperative of EstatePlanning: Not Just for the Affluent Often, there’s a prevailing misconception that estateplanning is a luxury reserved for the wealthy elite. Real estateplanning is a crucial undertaking that every adult and family should prioritize.

Roth IRAs offer unique advantages including tax-free growth, no required minimum distributions during the owner’s lifetime, and potential tax benefits for heirs. The absence of required minimum distributions during the owner’s lifetime. Some investors even convert stable-value assets first to minimize market risk.

This can include investing in stocks, bonds, real estate, and other assets. [3] 3] However, it’s not about picking the right assets and hoping to get rich quickly. Instead, it’s about knowing your options and executing a plan with consistency. Doing so may give you the best chance at increasing your wealth.

They can help you diversify your money across various asset classes and reduce your portfolio’s risk while aiming for consistent returns. A financial advisor can help you with estateplanning and preparing for your legacy goals Life is ever-changing, and estateplanning becomes even more crucial during retirement.

Donor Advised Fund (DAF): DAFs are charitable giving accounts that allow individuals, families, or organizations to make contributions to a fund, and receive an immediate tax deduction for the contribution while distributing grants out to charities over time. Here is an additional Mainstreet article that dives a little deeper into this topic.

An estimated 90% of wealthy families lose their wealth by the third generation, so if you are planning on leaving behind assets to your family, knowing the unique risks to the affluent investor and considering strategies to maintain your wealth within your family can be very beneficial. [1]

As a person grows old, they may lack the energy, health, and interest to manage their money and other assets. This can ensure that the client’s hard-earned money and other assets are well-protected and not misused. Help the elderly with estateplanningEstateplanning is an integral component of financial advice for seniors.

Business owners may be able to accelerate tax-deferred savings even more through different retirement plan structures. Optimize your investments with asset location If investors haven’t already been working to optimize their tax situation with asset location, now is the time.

Depending on the nature of the windfall, planning opportunities and considerations will vary. For example, the tax laws and distribution terms for an inheritance is quite different to the tax and liquidity considerations during an IPO. There are many ways individuals become suddenly wealthy.

These plans will not be offered to everyone and have restrictions for use. TAX AND ESTATEPLANNING. Another overlooked area of a sound financial plan is insurance coverage and their respective coverage amounts. We should review our personal insurance coverage yearly as our assets and liabilities change.

Unlocking the Power of Net Unrealized Appreciation (NUA) Many workers receive company stock as part of their compensation package or can take advantage of a company 401(k) plan, choosing from a menu of mutual funds, exchange-traded funds and company stock for their investments. The remaining assets may be rolled over.

According to a Fidelity study, 45 percent of younger investors are more inclined to consolidate their assets with one advisor as opposed to spreading assets across multiple advisors. Starting Out clients are typically focused on beginning to build wealth.

Only 26% of Americans have an estateplan. If you’re thinking, “But my clients are high-net-worth…many more have an estateplan.” And you’ll see in our Q&A below, that tax advisors can bring estateplanning into the conversation early on in a client relationship. What do these numbers tell us?

By Taylor Graff, Head of Asset Allocation Research and Ed Chadwyck-Healey, Head of International Private Clients ⚑ Investment Outlook Falling Interest Rates Trigger Investor Hunger For Yield Investors snapping up U.S. Consequently, investors need to build a solid defensive position while seizing opportunities that arise amid the instability.

By Taylor Graff, Head of Asset Allocation Research and Ed Chadwyck-Healey, Head of International Private Clients ? Private credit occupies a sweet spot on the investment landscape, offering earlier distributions than private equity and higher yields than most publicly traded securities. Investors snapping up U.S.

When considering the distribution of excess lifetime returns of individual stocks vs the Russell 3000, the median underperformance was almost -10%.³ Individuals who inherit a concentrated stock position should speak with their estateplanning attorney to confirm whether they’ll receive a step-up in basis.

Create or revise your estateplan 9. Plan for emergency expenses 11. Create or revise your estateplan While it’s not the most cheerful topic, having an estateplan is crucial when you’re preparing for a baby. If you already have an estateplan, make sure to update it to include your new baby.

Blind Spot 3: Inadequate estateplanning In today’s age, where 60 is the new 50 and people are more active and health-conscious than ever before, it is common to think that estateplanning can wait. Life is inherently unpredictable, and unanticipated circumstances can arise at any moment.

The Q3FY24 results displayed a positive outlook for the company with a 34% YoY increase in Total Revenue and 43% YoY in their assets under management (AUM). As of 2023, the industry boasts a staggering AUM (assets under management) of over Rs 39.4 of the Assets Under Management (AUM) originate from clients above Rs 50 Crores.

Long-term goals typically encompass retirement planning, wealth preservation and estateplanning. Your risk tolerance will influence your investment strategy and asset allocation. They are well-versed in various aspects of financial planning, including investments, retirement planning, estateplanning and tax management.

Update or create your estateplan If you don’t already have an estateplan , now would be a great time to create one. You should update or create an estateplan to reflect the change. Consult with an estate attorney to make decisions about how your loved ones will be taken care of.

But when it comes to your crypto assets, there are some strategies you can employ to make sure you don’t pay any more than you have to. Just like with other assets, if you buy crypto through an IRA, the tax will be paid at your income tax rate at retirement. Be aware of how long you have held onto your crypto assets.

Long-term goals typically encompass retirement planning, wealth preservation and estateplanning. Your risk tolerance will influence your investment strategy and asset allocation. They are well-versed in various aspects of financial planning, including investments, retirement planning, estateplanning and tax management.

A great way to save for college costs (and even K-12 education) is with a 529 plan. A 529 plan is a state-sponsored tax-advantaged way to save for education. While contributions are after-tax, both investment gains and qualified distributions are tax-free. . Check-In On Your EstatePlan.

Donors who contribute to a DAF can deposit cash, securities, or other assets into the fund. The donor relinquishes ownership of the assets but retains advisory privileges over how the contributions are invested and how grants are distributed to charities.

Specialized areas can include estateplanning and tax-efficient investment strategies. This includes in-depth insights into tax-efficient strategies for asset growth and diversification, detailed cash flow forecasting, budgeting, and leveraging financial data to make informed decisions.

Financial planning is about understanding and utilizing your assets in a manner that helps you and your family work towards achieving your goals and meeting your needs. While it may seem like a luxury that is only available to the wealthy, anyone is capable of building an effective financial plan and putting it into action.

The only other real variables that go into your standard of living in retirement are the amount of assets you have and your return on them, and you can’t really do anything about those at retirement. A minor one that most can do is to not automatically increase their distributions every year for inflation. That’s in Bucks County).

Market conditions may be volatile, but our planning efforts are, as always, focused on stability and consistency. You can find our annual planning checklist at the end of this article. OZ Funds” allow the deferral, and partial avoidance, of capital gains arising out of the sale of appreciated assets.

Business owners may be able to accelerate tax-deferred savings even more through different retirement plan structures. Optimize your investments with asset location If investors haven’t already been working to optimize their tax situation with asset location, now is the time.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content