This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Also in industry news this week: A recent survey indicates that younger "DIY" investors are more likely to be interested in working with a human advisor than their older counterparts, suggesting an opportunity for advisors to tap into this demographic (perhaps by setting minimum planning fees that ensure these clients can be served profitably today (..)

We’ve covered a lot of ground with regard to how various tax laws impact your retirementplans: pensions, IRAs, 403(b) and 401(k) plans. But we’ve primarily focused on the US income tax laws (the IRS) affect your plans – and there are many nuances that you need to take into account with regard to state tax laws.

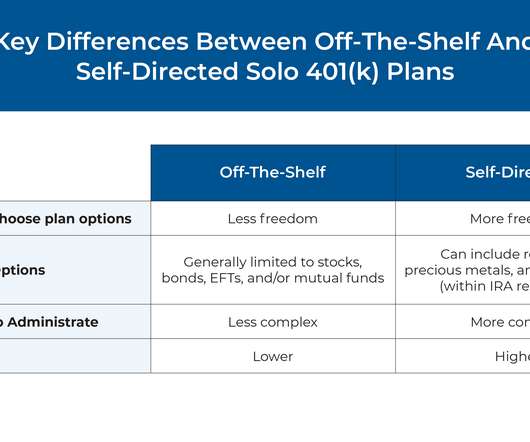

Among the several different types of retirementplans that are available to self-employed workers, solo 401(k) plans can offer the most flexibility and the ability to contribute the highest amount of tax-advantaged savings.

Financial advisors have a wide range of strategies at their disposal to create financial plans for their clients. And when it comes to retirementplanning, one popular technique is the use of ‘guardrails’, which set an initial monthly withdrawal rate that can be later adjusted as the size of the client’s portfolio changes.

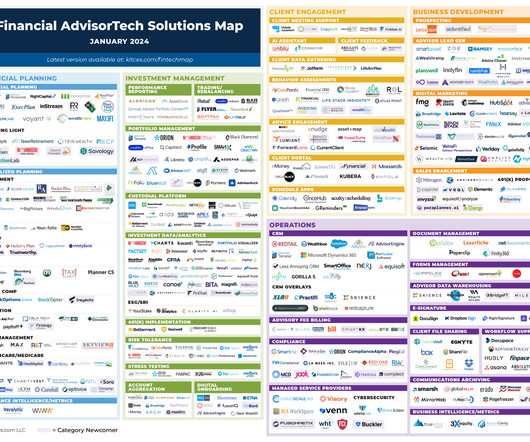

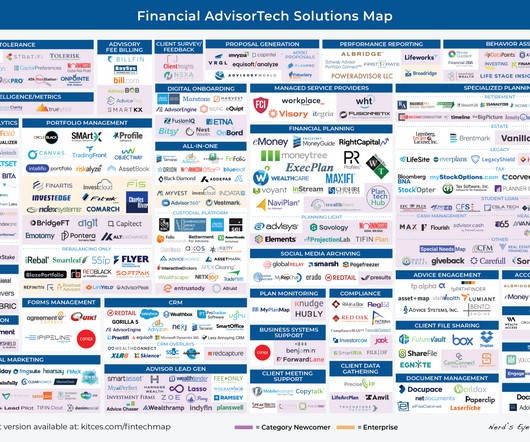

Welcome to the January 2024 issue of the Latest News in Financial #AdvisorTech – where we look at the big news, announcements, and underlying trends and developments that are emerging in the world of technology solutions for financial advisors!

equity valuations: “Baby-boomers’ huge flow of 401K plan contributions helped to drive equities higher; now that ~70 million Boomers are retiring, when do demographics flip this from a huge positive to a net drag?” aka The Hidden World of Failure ) (October 23, 2020) Stock Ownership : Distribution of Household Wealth in the U.S.

Also in industry news this week: A study suggests that simplification is the top reason consumers combine their investment accounts, signaling that the onboarding process for new advisory client assets is a value-add in itself.

From there, we have several articles on investment planning: While I Bonds have received significant attention during the past year, TIPS could be an attractive alternative for many client situations. A survey showing how millionaires allocate their assets and the importance they place on the recommendations of their financial advisors.

When you have the bulk of your financial assets in retirementplans, you might accidentally expose yourself to some risks that you haven’t thought about… since retirementplanassets are much more likely to be impacted by changes to legislation – as we have seen in the past. No related posts.

Unlike most types of retirementplans, the SEP IRA is funded by the employer. A SEP IRA (Simplified Employee Pension Individual Retirement Account) is a type of retirementplan specifically designed for self-employed individuals and small business owners. What is a SEP IRA?

GeoWealth has acquired its fellow TAMP First Ascent Asset Management, marrying GeoWealth’s tech-forward, open-architecture investment management platform with First Ascent’s 'concierge'-style investment and service-oriented solution (and its flat-fee TAMP business model).

Roth IRAs offer unique advantages including tax-free growth, no required minimum distributions during the owner’s lifetime, and potential tax benefits for heirs. This structure particularly benefits those expecting lower tax rates in retirement than during their working years. One of the Roth IRA’s most compelling features?

Your retirement income plan may be sending up bubbles, too, whether around Social Security, retirement account distributions, taxes or somewhere else – and these holes need to be patched up right away. So, to help your retirementplan be more airtight, let’s look at a few of the common leaks.

Do you have a plan in place for your retirement? For many people, the extent of their retirementplanning includes signing up for the plan at work – which is often more of a starting point than a comprehensive retirementplan. There are also 457 plans available for some private companies.

Know these 3 ages that can help you get the most out of your retirement accounts. At age 50, workers with certain qualified retirementplans can make annual “catch-up” contributions in addition to their normal contributions. Some 401(k) plans allow this, and others do not. Required Minimum Distributions at age 72.

According to research firm Cerulli Associates, Fidelity is a leading 401(k) plan provider with over $2.4 trillion in assets and more than a third of total 401(k) assets. Microsoft can offer a broad range of investment choices for plan participants through this platform. Microsoft’s 401(k) provider is Fidelity Investments.

RetirementPlanning 5 Ways to Catch Up on RetirementPlanning Later in Life Schedule a Complimentary Financial Review CLICK HERE TO SCHEDULE. Retirement is a significant investment, which is why so many financial experts recommend establishing goals and starting when still a younger adult. SIMPLE 401(ks) and IRAs

Two primary goals of the IRA were to provide a tax-advantaged retirementplan to employees of businesses that were unable to provide a pension plan; in addition, to provide a vehicle for preserving tax-deferred status of qualified planassets at employment termination (rollovers).

The IRS implements whats known as the wash-sale rule, which prohibits you from buying a substantially identical security within 30 days before or after the sale of a loss-producing asset. Charitable Contributions Consider donating appreciated assets such as stocks or real estate. Available to taxpayers aged 70.5

Further, unlike retirement accounts, assets in a brokerage account can be used for any purpose at any time without early withdrawal penalties. For high-income individuals, maxing out annual 401(k) contributions likely won’t be enough to maintain an equal lifestyle in retirement , especially if you wish to retire early.

If you’re not, put a plan in place, get on the right track. 2. Leave It Where It Is You may elect to do nothing and leave your assets in your old 401(k). Be sure you know the details on balance requirements before you do – the account balance may need to exceed a certain balance to be allowed to stay in the plan.

While grappling with various aspects of retirementplanning, it is imperative to acknowledge a critical factor that often does not receive its due attention – longevity risk. While this is undoubtedly positive, it introduces the challenge of ensuring that your financial resources last an extended retirement period.

If you think retirementplanning moves stop at retirement, think again. Although it won’t make sense in every situation, retirement can be a unique opportunity for Roth conversions for some investors. The example above assumes the couple does not need the full distribution from the IRA to meet lifestyle expenses.

Form 1099-DIV is sent to investors who receive dividends and distributions. Form 1099-R reports distributions from pensions, annuities, retirementplans etc. Records for any stocks or other investments you sold in 2022, including crypto transactions or other digital assets. Did you have AMT? Do you have dependents?

Understand the basics first, and then create an estate plan. Wills and trusts are both important estate planning tools with important differences. A will ensures property is distributed after your passing, according to your wishes, while a trust goes into effect as soon as you create it. A Will vs. a Trust.

Unlocking the Power of Net Unrealized Appreciation (NUA) Many workers receive company stock as part of their compensation package or can take advantage of a company 401(k) plan, choosing from a menu of mutual funds, exchange-traded funds and company stock for their investments. The remaining assets may be rolled over.

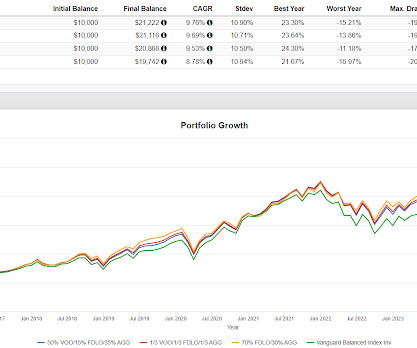

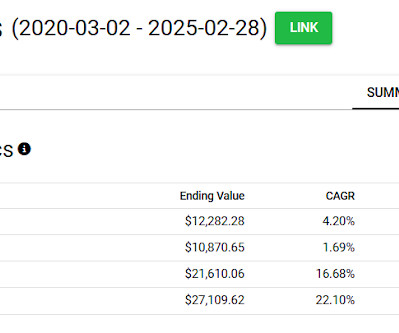

The first example to look at they call Leverage In The Strategic Asset Allocation via this table in the paper. The distribution of results are pretty even. These are easy to model. We'll use Fidelity Low Volatility Factor ETF (FDLO) as a proxy for low volatility for this post. The results here are consistent with the paper.

As we look forward to 2023, the IRS recently announced that the contribution limits for employer-sponsored retirementplans are going up. You may want to review your contribution amounts and adjust for January payrolls if your goal is to maximize funding your retirementplan contributions. . IRA Accounts.

Plan for Healthcare Healthcare is one of the biggest uncertainties in retirementplanning. There are approaches to investing in retirement that seek to align your risk tolerance with your need to turn investment assets into retirement income.

Further, both examples ignore other sources of income, such as wages, pre-tax retirement account distributions, dividends, etc., Considering tax planning strategies to reduce the impact of the new MA surtax. Further, if you weren’t planning to sell the asset, it’s usually not advisable to do so for tax reasons alone.

Tax benefits and owner retirement savings options also make establishing a 401(k) plan a smart choice for employers. This guide will help you learn more about the advantages of offering retirementplans to employees, how to get started and options for effectively distributingplan information.

That will give you an opportunity to invest in crypto on the same platform where you hold other assets. Crypto is considered to be an alternative asset that represents a diversification away from more traditional financial assets like stocks and bonds. Unlike most other assets, crypto is not backed by anything.

And how does it compare to the 401k and other retirementplans that exist? Being a self-employed retirementplan , the SIMPLE IRA gives you the discretion of what exactly you want your money invested into. . Most retirementplans — 401(k)s, regular IRAs, or Roth IRAs, etc. What is a Simple IRA?

New assets in to the fund and the passing of existing fund holders become potential sources for higher payouts. There's pending legislation that if passed could be very favorable for retirement savers and retirees in terms of providing more flexibility. Stay tuned.

Barron's wrote about the difficulty of spending down accumulated assets in retirement. XYLD's distributions appear to be 60/40 but only a medium degree of confidence on that so check for yourself. WIW is the Western Asset Inflation Linked Opportunity and Income Fund. Several quick hits today.

Take Advantage of RetirementPlans and Matching Contributions. Most employer retirementplans allow you to save on a tax-deferred basis, meaning that contributions into these types of accounts are not considered in calculating your taxable income. . Determine an Appropriate Risk Tolerance for a Longer Time Horizon .

Your asset allocation is the percentage of your portfolio that you distribute between different asset classes, like stocks and bonds. To rebalance your portfolio, you’ll buy and sell certain investments to realign to your accounts with your desired asset allocation. Why do you need to rebalance your portfolio?

Business owners may be able to accelerate tax-deferred savings even more through different retirementplan structures. Optimize your investments with asset location If investors haven’t already been working to optimize their tax situation with asset location, now is the time.

Blind spots in retirementplanning are those aspects that are often overlooked, either intentionally or subconsciously. From seemingly harmless low-interest debt to underestimating the emotional impact of transitioning out of the workforce, various factors can disrupt your peace of mind during your retirement years.

The rules surrounding Individual Retirement Accounts (IRAs) undergo frequent and impactful changes. While IRAs are a cornerstone for many retirementplans, these accounts being inherited adds a layer of complexity to them. The IRS has instituted separate rules and options for each category.

As these resources lay idle, they may miss out on potential growth through investment returns, compounding the challenge of securing a comfortable retirement. This suggests that the total value of uncashed retirementplan checks could easily exceed $500 million cumulatively.”

Roth IRAs don’t come with Required Minimum Distributions (RMDs) at age 72 like a traditional IRA either, so you can continue letting your money grow until you’re ready to access it. When you do decide to take distributions from a Roth IRA, you won’t have to pay income taxes on that money. Not sure about your future tax brackets?

For high-net-worth individuals and families, retirement is a significant shift. A high-net-worth individual, also known as an HNWI, is typically someone with at least $1 million in cash or assets that can be easily converted into cash, including stocks, bonds, mutual fund shares, and other investments. [1]

There is concern, however, that the 4% rule does not account for the goals of the retiree, asset location, or taxation. There is concern, however, that the 4% rule doesn’t account for the goals of the retiree, asset location, or taxation. In addition, location of assets is generally not considered in the 4% rule.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content