This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Also in industry news this week: NASAA has proposed an amendment to its broker-dealer conduct model rule that would restrict the use of the terms “advisor” and “adviser” for broker-dealers and their registered representatives who are not also investment advisers or investment adviser representatives A recent study suggests that (..)

As the year comes to a close, now is the time to review potential financial moves to help minimize your tax burden heading into 2025. Proactive year-end taxplanning can lead to significant savings and set you up for financial success in the new year. Find your next tax advisor at Harness today.

As a result, there's a common line of thinking that people saving for retirement should avoid pre-tax retirement accounts entirely and contribute (or convert existing pre-taxassets) to Roth instead – regardless of which tax bracket they're in today.

If you've heard of a DAF and are curious about incorporating it into your giving and taxplanning strategy, this article is for you. Key Takeaways: Contributions to a donor-advised fund reduce your tax bill in the year your contribution is made. What is a Donor Advised Fund?

The IRS implements whats known as the wash-sale rule, which prohibits you from buying a substantially identical security within 30 days before or after the sale of a loss-producing asset. Defer income where possible Strategically timing your income can have a major effect on your tax liability. Available to taxpayers aged 70.5

As we begin our countdown to 2024, it is a great time to ensure your year-end taxplan is in place. Taxplanning is a vital component of meeting your overall financial goals. Our team of professionals is here to assist with your financial and taxplanning needs. You can access the webinar recording here.

Other reasons involve changes in investment strategy, portfolio rebalancing, or a simple desire to exit a specific asset class. Instead, partners (investors) are taxed directly on their share of the fund’s income, gains, losses, and deductions, regardless of whether those amounts are actually distributed.

But you might consider increasing your impact by setting up a structured , long-term philanthropic plan such as an endowment. An endowment is a portfolio of assets that is invested to provide support for a cause. Donations to endowment funds are tax-deductible, giving them a place in your overall financial management and taxplan.

The Tax Cuts and Jobs Act of 2017 eliminated recharacterization, transforming Roth conversions into permanent decisions requiring thorough analysis before execution. Roth IRAs offer unique advantages including tax-free growth, no required minimum distributions during the owner’s lifetime, and potential tax benefits for heirs.

Further, unlike retirement accounts, assets in a brokerage account can be used for any purpose at any time without early withdrawal penalties. Retiring early is also even more difficult without taxable assets as you’ll need to bridge the gap before penalty-free distributions from 401(k)s or IRAs begin, perhaps to cover medical expenses.

Cost-saving taxplanning can be much more difficult to implement after your company is well-established and has reached the stage where an IPO, merger, or acquisition becomes a likely event. The first three options are pass-through entities, so profits and losses are distributed to the owners who are taxed on them.

For example, if you convert $50,000 and it grows to $100,000 in a Roth IRA over the next several years, that essentially results in $50,000 tax-free dollars. Keeping your funds in a traditional IRA only defers taxation on the full amount until the funds are distributed at some point in the future.

The simple examples above only illustrate the state tax impact, but federal tax implications will also apply. Further, both examples ignore other sources of income, such as wages, pre-tax retirement account distributions, dividends, etc., that could increase the tax due from the surtax. Recognize the gain now.

What are appropriate checklists for year-end taxplanning? Tax planners often develop checklists to guide taxpayers toward year-end strategies that might help reduce taxes. Certain tax benefits may be available if you can claim an individual as a dependent. Family taxplanning. Financial investments.

If you are expecting sudden wealth from the sale of a business or other liquidity event, then it may not make sense to do a conversion in the same tax year, but could be worth considering alongside cash allocation discussions. You expect your future tax rate will be higher than it is today Time value of money.

They can help you diversify your money across various asset classes and reduce your portfolio’s risk while aiming for consistent returns. A financial advisor can craft tax-efficient withdrawal strategies to minimize the tax burden on your retirement income. Taxplanning is not solely about federal taxes.

A little bit of effort and forward thinking during our summer and fall months will lead to a much more palatable and, potentially, financially advantageous tax season the following year. The reason for this is quite simple – taxplanning requires actual planning. Timing: Ideally earlier in the year.

This tax benefit is scheduled to sunset at the end of 2026. Taxplanning for 2026 Depending on your situation, income, and goals, your planning options will vary. As with anything in taxplanning, it’s important not to let the tax-tail wag the dog.

The post Part 1: The Tools of the Tax-Planning Trade appeared first on Yardley Wealth Management, LLC. Part 1: The Tools of the Tax-Planning Trade Whether you’re saving, investing, spending, bequeathing, or receiving wealth, there’s scarcely a move you can make without considering how taxes might influence the outcome.

The post Part 1: The Tools of the Tax-Planning Trade appeared first on Yardley Wealth Management, LLC. Part 1: The Tools of the Tax-Planning Trade. Whether you’re saving, investing, spending, bequeathing, or receiving wealth, there’s scarcely a move you can make without considering how taxes might influence the outcome.

Limited partnerships can be used to split income taxes. Typically, parents form an FLP and transfer their assets (e.g., Gifting assets to family members is another way to shift income. It might be advantageous for you to gift income-producing investment assets (such as stock in various companies) to your relatives.

A DAF is an excellent way to achieve an immediate tax deduction without feeling obligated to give an entire gift at once. With a DAF, you contribute assets — cash, real estate, stock, even cryptocurrency — to a fund you establish through a custodial account, which then becomes a charitable account you personally control.

If you earn income from various sources throughout the year, such as equity windfalls, venture capital fund distributions, crypto investments, and sales, or small business income, you will need to pay estimated quarterly taxes. Any time you sell, exchange, or use crypto to purchase goods or services, you may trigger a taxable event.

However, a period of lower income in 2024 could present valuable taxplanning opportunities. One potential benefit of a job layoff is a temporary drop in your federal income tax bracket, which can create opportunities for future tax savings.

No required minimum distributions (RMDs) in Roth 401(k) plans. Starting in 2024, individuals who left assets in a Roth employer plan won’t be subject to mandatory distributions during their life. As with any financial decision, there are pros and cons to leaving money in an employer plan vs rolling it over.

Your retirement income plan may be sending up bubbles, too, whether around Social Security, retirement account distributions, taxes or somewhere else – and these holes need to be patched up right away. So, to help your retirement plan be more airtight, let’s look at a few of the common leaks.

Unlocking the Power of Net Unrealized Appreciation (NUA) Many workers receive company stock as part of their compensation package or can take advantage of a company 401(k) plan, choosing from a menu of mutual funds, exchange-traded funds and company stock for their investments. The remaining assets may be rolled over.

These numbers show an opportunity for tax practices to build deeper, meaningful relationships with their clients, helping them to navigate some of life’s most challenging financial decisions. And you’ll see in our Q&A below, that tax advisors can bring estate planning into the conversation early on in a client relationship.

It is one of the oldest with 22 years of operating in the Asset Management industry. Their funds include Active funds, Absolute Funds, Liquid Funds, Overnight Funds, Gilt Funds, TaxPlans, Large Cap, Dynamic Asset Allocation Funds, and others. 26,644 crore, Quant ELSS Tax Saver Fund’s AUM of around Rs. 3,936 crore.

According to a Fidelity study, 45 percent of younger investors are more inclined to consolidate their assets with one advisor as opposed to spreading assets across multiple advisors. Starting Out clients are typically focused on beginning to build wealth.

Regardless of your age or health status, having a comprehensive estate plan is essential for safeguarding your assets, ensuring your wishes are implemented, and providing peace of mind for you and your family. Diversifying reduces the likelihood of significant losses if one investment or asset class performs poorly.

Qualified Small Business Stock (QSBS): Private investors may be eligible for unique tax benefits depending on the type of business they invest in. To qualify, a business must be structured as a C corporation and have less than $50 million in assets at the time the stock is issued. Tax services provided through Harness Tax LLC.

Your risk tolerance will influence your investment strategy and asset allocation. Certified Public Accountant (CPA) CPAs specialize in taxplanning and accounting. While they may not be exclusively wealth managers, their expertise in tax matters can be invaluable in managing your taxes efficiently.

presidential election, we have grappled with the lack of clarity regarding the details of new tax legislation. The outcome of the tax reform debate is likely to impact how we advise clients on taxplanning, estate planning and a host of other topics. Since last year’s U.S. Those conditions do not exist today.

Donors who contribute to a DAF can deposit cash, securities, or other assets into the fund. The donor relinquishes ownership of the assets but retains advisory privileges over how the contributions are invested and how grants are distributed to charities.

This tax benefit is scheduled to sunset at the end of 2026. Taxplanning for 2026 Depending on your situation, income, and goals, your planning options will vary. As with anything in taxplanning, it’s important not to let the tax-tail wag the dog.

Unlike an endowment, taxes really matter. It’s a shift of mindset from the earlier days, when they were building their wealth, and we were more focused on income taxplanning. What we often see is people are too late to think about estate taxes. The remaining assets are then given to charity when the trust ends.

Your risk tolerance will influence your investment strategy and asset allocation. Certified Public Accountant (CPA) CPAs specialize in taxplanning and accounting. While they may not be exclusively wealth managers, their expertise in tax matters can be invaluable in managing your taxes efficiently.

Besides meeting all the requirements for this date, have you considered the impact of implementing long-term tax strategies on your wealth? So take advantage of the opportunity to optimize your taxplanning and maximize your financial growth potential. There is one opportunity left to lower your tax bill this year.

The Igloo Company Pudgy Penguin #7625 – source: sothebys.com As non-fungible tokens (NFTs) have gained mainstream popularity, it’s essential to understand the tax implications associated with these crypto assets. After selling an NFT at a loss, you may want to invest in a similar NFT or another asset class.

No-one loves paying taxes. But when it comes to your crypto assets, there are some strategies you can employ to make sure you don’t pay any more than you have to. Did you know you can buy crypto through an IRA and receive the same tax benefits? You can see the crypto advisor tax webinar replay here. Manage your timing.

In this article, we’ll go into all that and more, including: Vesting schedules and cliffs Alternative Minimum Tax The Post-Termination Exercise Period State residency considerations for relocation Vesting schedules and cliffs A vesting schedule is the timeline of when you will receive your stock options or grants.

These forms include: 1099-NEC (Non-Employee Compensation): Reports payments made to independent contractors or freelancers for services performed that total $600 or more in a tax year. 1099-DIV (Dividends): Reports dividends and other distributions from investments, typically received from stocks or mutual funds.

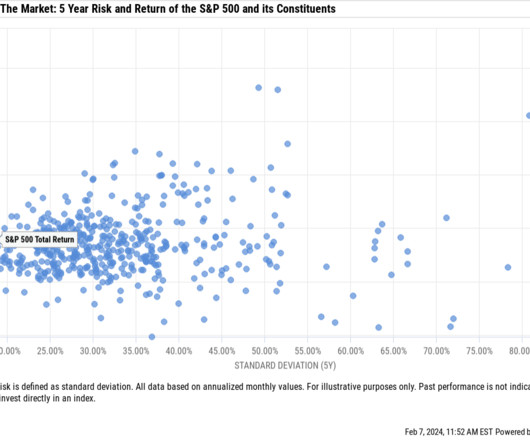

When considering the distribution of excess lifetime returns of individual stocks vs the Russell 3000, the median underperformance was almost -10%.³ Further, it means selling other diversified assets (or using cash) to fund the put option purchase, essentially furthering the concentration in the stock.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content