This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

We start with several articles on retirement planning: Why considering a client's retirement time horizon and spending flexibility could lead to more accurate (and often higher) safe withdrawal rates than the simpler "4% rule" Four unique risks retirees face when drawing down their assets, from sequence of returns risk to tax risk, and how financial (..)

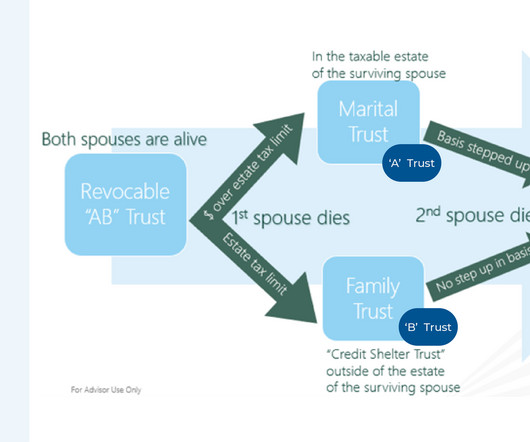

In recent years, the Internal Revenue Code (IRC) has endured some drastic changes resulting from legislative action that have altered the strategies estateplanning professionals have recommended to clients. For instance, prior to the 2017 Tax Cuts and Jobs Act (TCJA), "A/B trusts" had become ubiquitous for spousal estatetaxplanning.

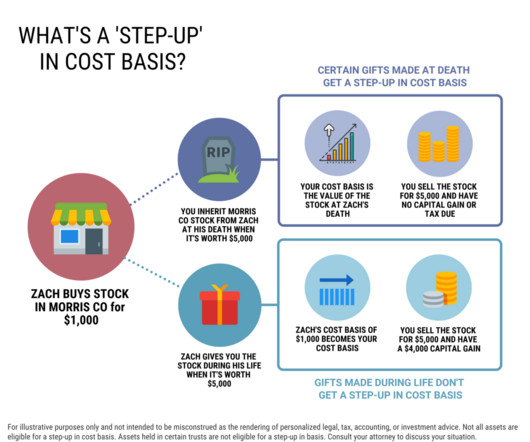

A step-up in basis is a tax advantage for individuals who inherit stocks or other assets, like a home. Heres how stepped up cost basis works on stock and other assets at death. Understanding step-up in basis at death If youve received an inheritance you may have questions about the tax treatment of certain assets.

morningstar.com) Early in retirement is the time to do some taxplanning. nextavenue.org) Estateplanning Mistakes to avoid in your estateplanning. theretirementmanifesto.com) If you have a valuable collection you need a plan for its eventual disposition.

While asset protection is a popular planning topic for High-Net-Worth (HNW) and ultra-high-net-worth clients, those who are not HNW are susceptible to the same threats to wealth. Notably, certain client assets have built-in creditor protection without the use of (often expensive) products or tools.

As a Christian, your estateplan should represent your dedication to financial stewardship according to Scripture. W hat important factors should Christians consider when estateplanning? W hat important factors should Christians consider when estateplanning?

As the year comes to a close, now is the time to review potential financial moves to help minimize your tax burden heading into 2025. Proactive year-end taxplanning can lead to significant savings and set you up for financial success in the new year.

Welcome to the October 2024 issue of the Latest News in Financial #AdvisorTech – where we look at the big news, announcements, and underlying trends and developments that are emerging in the world of technology solutions for financial advisors!

This shift has led financial advisors to explore new strategies for mitigating the resulting tax-planning challenges. Under the new law, non-spouse beneficiaries (with few exceptions) must now withdraw the entirety of an inherited IRA within 10 years of the account owner's passing rather than over their own lifetimes. Read More.

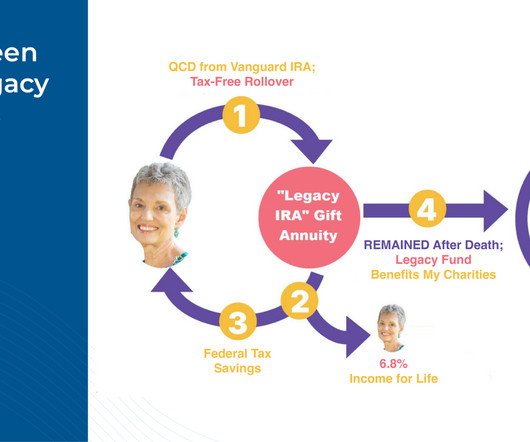

However, the caveat with current CGAs has been that they could only be funded with after-tax dollars before the donor’s death, meaning that if an individual only had tax-deferred funds (e.g., But the SECURE 2.0 But the SECURE 2.0 legislation at the end of 2022. Read More.

million in assets to both retire and pass on a legacy interest (though many have yet to establish an estateplan), according to a recent survey. Enjoy the current installment of "Weekend Reading For Financial Planners" – this week's edition kicks off with the news that affluent Americans believe they need an average of $5.5

Choosing whether to fund a trust with your assets is an important decision in the estateplanning process. Here are three main reasons you may want to consider putting your assets in a trust. A will and a trust are two different estateplanning tools. Do I need a revocable living trust?

In this guest post, Harness Tax Advisory Council member, Griffin Bridgers, J.D., covers some of the top estateplanning trends that tax advisors should be tracking during the second half of 2024. contained a number of changes relevant to estateplanning. citizens and residents. The SECURE Act 2.0

Like individuals, businesses holding investments and other capital assets should consider other income, gains, and losses when determining when to sell capital assets. Defer income Clients may consider putting off asset sales or delaying receipt of other income until next year to reduce 2023 taxable income.

Creating wealth that can provide financial security for generations to come is an incredible feat, and it requires careful planning, consideration, and communication among family members. Let’s take a look at the tax impact and other considerations of each. 200/share (today’s fair market value) – $188.44/share

However, at death, a living trust can provide two key benefits compared to owning assets not held in trust. What happens to my assets after I die? Before diving into a discussion on the benefits of living trusts, it’s important to first understand what happens to different types of assets after someone dies. non-attorney).

While there are certainly ways to do estateplanning without a lawyer, for most people hiring an estateplanning attorney makes the most sense. Estateplans can get complex fast, and even fairly straightforward estates can feel overwhelming if you’re not trained in the area. Do your research.

At its core, investment planning ensures that your financial resources are strategically allocated to various asset classes in accordance with your risk tolerance and investment objectives. Another important aspect of investment planning is its role in combating inflation. This makes them a valuable tool for taxplanning.

Tax loss harvesting involves selling losing investments to offset capital gains, thus limiting the taxes you owe. While it doesn’t always make sense to take a loss on investments, evaluate your portfolio and consider whether selling some poorly performing assets may make sense in your situation. Estateplanning.

Estateplanning is a critical component of a comprehensive financial plan. It involves deciding how your assets will be distributed upon your death or incapacitation. Furthermore, estateplanning includes aspects such as tax minimization strategies, asset protection, and charitable giving.

They can help you diversify your money across various asset classes and reduce your portfolio’s risk while aiming for consistent returns. A financial advisor can craft tax-efficient withdrawal strategies to minimize the tax burden on your retirement income. Taxplanning is not solely about federal taxes.

Navigating the complexities of estateplanning can often feel like charting through uncharted waters, especially when it comes to handling assets, taxes, and ensuring one’s legacy is preserved according to their wishes. However, there are nuances to consider.

With the fee-for-service model, you can customize service offerings for clients seeking advice who don’t (yet) have traditional portfolio assets to transfer to your firm’s custodian for full-time management. This approach allows you to engage these clients by charging a fee that’s covered through their monthly cash flow.

In this article, well explore all the details of alternative investments, the reasons behind their growth as an investment choice, and how their tax treatment differs from traditional assets. Well also go into some potential strategies to optimize tax efficiency. What Are the Tax Strategies for Alternative Investments?

This tax benefit is scheduled to sunset at the end of 2026. Taxplanning for 2026 Depending on your situation, income, and goals, your planning options will vary. As with anything in taxplanning, it’s important not to let the tax-tail wag the dog.

The post Part 1: The Tools of the Tax-Planning Trade appeared first on Yardley Wealth Management, LLC. Part 1: The Tools of the Tax-Planning Trade Whether you’re saving, investing, spending, bequeathing, or receiving wealth, there’s scarcely a move you can make without considering how taxes might influence the outcome.

The post Part 1: The Tools of the Tax-Planning Trade appeared first on Yardley Wealth Management, LLC. Part 1: The Tools of the Tax-Planning Trade. Whether you’re saving, investing, spending, bequeathing, or receiving wealth, there’s scarcely a move you can make without considering how taxes might influence the outcome.

This is a particularly important example for those considering leaving New York City for the New Jersey suburbs, as, in a liquidity event, that move would end up costing you a lot in state taxes. Estatetax should not be mistaken for inheritance tax, which is applied to the person who inherits the asset of the estate.

Investment strategy: Determine asset allocation and investment vehicles aligned with risk tolerance and financial goals. Retirement planning: Calculate retirement needs and contribute regularly to retirement accounts. What Could Happen if You Don’t Have a Financial Plan?

What do you need to consider about gifting as it relates to your overall estateplan? Let’s take a closer look at estate and gift taxes and how you can approach them with a financial planning mindset. Taxes on Giving??? Why do you have to pay taxes on money you’re giving away? The tax above the $13.61

Part 3: Tax-Wise Financial Planning In our last two pieces, we covered some tools of the tax-planning trade, as well as how to deploy them for tax-efficient investing. But taxplanning isn’t just for your investments. But we can weave each event into the tax-planning fabric of your financial life.

Part 3: Tax-Wise Financial Planning. In our last two pieces, we covered some tools of the tax-planning trade, as well as how to deploy them for tax-efficient investing. . But taxplanning isn’t just for your investments. Each can translate into tax-planning challenges and opportunities: .

Only 26% of Americans have an estateplan. If you’re thinking, “But my clients are high-net-worth…many more have an estateplan.” These numbers show an opportunity for tax practices to build deeper, meaningful relationships with their clients, helping them to navigate some of life’s most challenging financial decisions.

FINANCIAL PLANNING 4 Areas Your Financial Planner Should Cover as a High-Net-Worth Individual Schedule a Complimentary Financial Review CLICK HERE TO SCHEDULE. Unlike average investors, high-net-worth individuals (HNWIs) typically utilize accumulated assets and a constant income stream to pay for their future expenses.

Anyone who owns company stock will eventually have to decide how to distribute their assets — typically when there is a job change or retirement involved. When you transfer most assets to a taxable account, there will be income tax, but with company stock, you can take advantage of net unrealized appreciation (NUA). .

Part 2: Tax-Wise Investment Techniques In our last piece, we introduced some of the tools of the tax-planning trade. In other words, your tax-planning techniques matter at least as much as the tools. Tax breaks come and go, and are beyond our control. It’s another to make best use of them.

Part 2: Tax-Wise Investment Techniques. In our last piece, we introduced some of the tools of the tax-planning trade. These include tax-sheltered accounts for saving toward retirement, healthcare, and education, as well as tax-efficient tools for charitable giving, emergency spending, and estateplanning. .

According to a Fidelity study, 45 percent of younger investors are more inclined to consolidate their assets with one advisor as opposed to spreading assets across multiple advisors. Starting Out clients are typically focused on beginning to build wealth.

The end of the year is an ideal time to start planning for the year ahead and make sure you’re on target to achieve those goals. Asset and Liability Matching. Good financial planning is all about asset and liability matching across time. A financial plan with an asset liability mismatch is likely to fail over time.

Blind Spot 3: Inadequate estateplanning In today’s age, where 60 is the new 50 and people are more active and health-conscious than ever before, it is common to think that estateplanning can wait. Life is inherently unpredictable, and unanticipated circumstances can arise at any moment.

Long-term goals typically encompass retirement planning, wealth preservation and estateplanning. Your risk tolerance will influence your investment strategy and asset allocation. They are well-versed in various aspects of financial planning, including investments, retirement planning, estateplanning and tax management.

Your business advisory team may consist of: a business broker or M&A advisor, accounting and tax advisors, and transaction/M&A attorney. On the personal side, your financial advisor , estateplanning attorney, and CPA/tax advisor should be involved throughout the process.

The six-person team, led by managing partner, wealth advisor, Ty Vogele, and wealth advisors David Guenthner, CEPA ® and Ryan Wittman, AIF ® , manages over $400 million in assets. Now, we have the resources and support to deepen client relationships and explore innovative financial planning solutions.

Gift Tax Exemptions Each year, you can give up to $17,000 to any number of people tax-free. This means that if you have two children, you can give each of them $17,000 without a tax penalty in 2023. [1] 1] This can be something you do as part of your estateplan.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content