This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The two most common pricing models are fee-onlyfinancial planners (flat-fee or fixed-fee advisors) and AUM-based financial advisors (who charge a percentage of assets under management). While AUM advisors may seem appealing, they often come with high lifetime fees and potential conflicts of interest.

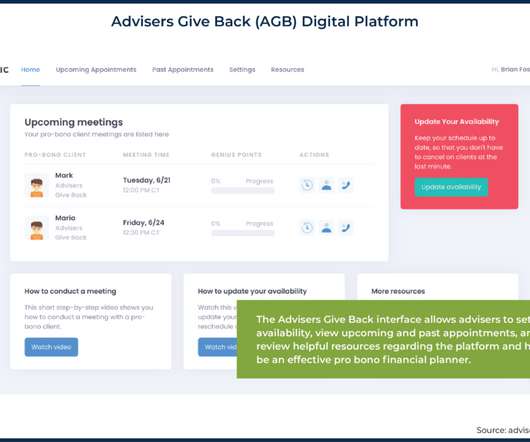

By helping clients develop financial goals, creating a financial plan, and supporting the implementation and monitoring of the plan, advisors help clients live their best lives. Pro bono financial planning refers to free, no-strings-attached financialadvice and planning for underserved people. Read More.

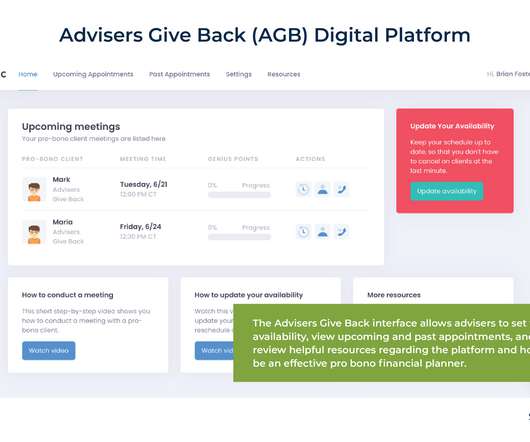

By helping clients develop financial goals, creating a financial plan, and supporting the implementation and monitoring of the plan, advisors help clients live their best lives. Pro bono financial planning refers to free, no-strings-attached financialadvice and planning for underserved people. Read More.

Hybrid firms can switch between their status as a registered investment advisor and brokerage, which can be problematic for individuals seeking unbiased financialadvice. Benefits of working with an independent fiduciary advisor Independence is important when seeking financialadvice.

Consumers have a wide range of options when it comes to choosing a provider of financialadvice, from larger wirehouses and asset managers to smaller Registered Investment Advisers (RIAs).

Zack is the Director of Financial Planning and Participant Engagement of Greenspring Advisors, an RIA based in Towson, Maryland, that manages $2 billion of private wealth assets under management for 1,300 client households and advises on an additional $5 billion in retirement plan assets.

This might have been their own doing or the result of poor financialadvice. Do it yourself if you’re comfortable or hire a fee-onlyfinancial advisor to help you. If you have a financial plan this is an ideal time to review it and see where you are relative to your goals.

With so little time until the end of the year, it may not be feasible to sell a home, business, or other assets unless it was already in the works. Further, if you weren’t planning to sell the asset, it’s usually not advisable to do so for tax reasons alone. Recognize the gain now.

Knowing the types of financial advisors and their compensation models can empower you to select a professional whose approach aligns seamlessly with your financial goals, risk tolerance, and overall budget. Below are the different types of financial advisors you can choose from based on their fee model: 1.

According to Veres, the revenue model and the value proposition are the most confusing things for the public when it comes to financialadvice. Providing financial plans vs. canned financial plans with a sales agenda. Fee-only vs. fee-based. The future of financialadvice.

When I started Vincere Wealth as a fee-only practice, the vision was to become the go-to place for Millennials who need help with their money. The problem was that I couldn’t give these younger clients the time of day in that setting because they didn’t have enough investable assets yet.

One common aspect that most individuals consider is the cost associated with engaging a financial advisor. Working with a financial advisor entails a financial commitment, typically represented by an annual fee of 1% of the assets entrusted to their management.

The primary fee structures are: Fee-only : Advisors only receive payment from their clients for the services they provide, not receiving any commissions or other incentives from product providers. Fee-based : This structure is a blend of fees and commissions. Hourly FeeFee charged per hour of advice.

But before we get to the blog… Look, there are alot of schmucks out there hawking crap products disguised as financialadvice. Please subscribe to my newsletter to receive updates that raise awareness of consumer financial issues. Pay attention to how you are actually paying the fee. Don’t be fooled!

I have a newsletter in which I talk about financial advisor lead generation topics which is best described as “fun and irreverent.” I am an irreverent and fun marketing consultant for financial advisors. Why is the fiduciary standard important in financialadvice? What is a conflict of interest in financialadvice?

The move to financial planning transparency is aflame! in all aspects of financialadvice, with a special focus on AdviceOnly, Flat Fee, and Hourly service models. There is an emphasis on logical and clear disclosure of services and their related fees. Client advocacy. There is a record of it.

Financial planners plan and manage your portfolio in a way that saves your time. You can hand over 1% of your annual assets to financial advisors and in return, you will be getting more and more bunch of advice. A financial advisor is someone who helps manage your money by planning for your future.

I said that brokers and sales agents are essentially predators, wolves in sheep’s clothing, where the sheep are fiduciary advisors, and the clothing is, well, you know what it is: ‘fee-based’ and ‘best interest’ (instead of fee-only and fiduciary). If we can’t, we’ll tell you, and help you find someone who can.

The convergence was really between my first-hand experience as a freelancer, my personal connection with the industry, and the feasibility of offering fee-onlyfinancial planning to a segment of the population with little to no investable assets that has traditionally been ignored. How are you getting COIs involved?

Is it better to have a financial advisor or do it yourself? Do you need a financial advisor if you don’t have a lot of money? What types of financial advisors should you avoid? Article related to financialadvice Do you need a financial advisor? When should you get a financial advisor?

Is it better to have a financial advisor or do it yourself? Do you need a financial advisor if you don’t have a lot of money? What types of financial advisors should you avoid? Article related to financialadvice Do you need a financial advisor? When should you get a financial advisor?

This interview with Cody Garrett, CFP, of Measure Twice Financial was mind-blowing. It’s so clear to me what the future of financialadvice is – what it should be – and what it will be. I am an irreverent and fun marketing consultant for financial advisors. What is an advice-onlyfinancial planner?

And that’s why I’m writing this blog; because I feel that financialadvice rendered by the hour is a great thing for the American public (for the reasons we’re going to discuss below). He does not take custody of assets or have discretion. His service focuses solely on advice. It was very successful.

It is not personal legal/tax/financialadvice or an exhaustive discussion of the exclusion. At any time before and right after issuance, the company’s aggregate gross assets were less than or equal to $50 million ¹. Generally, gross assets mean cash and adjusted tax basis in property held by the issuing corporation.

Large Cap Stocks were the best performing asset class of all nine categories three times and finished second twice. Large Cap was the next asset class under these foreign blue chips. Large caps beat the foreign stock categories yet still lost thirty-seven percent of their value, while 2011 was the only year where U.S.

They’re almost a billion dollars in assets. There’s no doubt in my mind, as having run a firm that was $90 million in assets, the one that is coming where $3 and eventually $4, when the last deal closes, a billion dollars is a lot of assets. I have half a billion dollars in assets. RITHOLTZ: Right?

If you see the IUL grifters on TikTok claiming an IUL policy is better than a 401k, or that is has upside potential with downside protection, a “can’t lost money asset”, or “privatized banking” you’ll know why the outrage is well deserved. Then how come it’s sold as “can’t lose money asset” and other BS claims?

Feeonly advisors can now purchase annuities for their clients without having to be licensed agents. And if you want to join the right for higher ethics in financialadvice, join the Transparent Advisor Movement. Scott Salaske is the founder and CEO of Firstmetric , a flat feefinancial advisor firm in Troy, Michigan.

Scott Salaske is the founder and CEO of Firstmetric , a flat feefinancial advisor firm in Troy, Michigan. Ever since the beginning of his 20+ year long career, Scott has pursued his mission of delivering high quality financialadvice in a low cost and unbiased way. He started Firstmetric a few years later.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content