This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Answering it well requires a range of assumptions – from estimating average investment returns to understanding correlations across asset classes. These assumptions are rooted in Capital Market Assumptions (CMAs), which project how different assets might perform in the future.

Welcome to the 432nd episode of the Financial Advisor Success Podcast! Seth is the founder of Heartwood FinancialPlanning, an advisory firm affiliated with PlanMember Securities Corporation that is based in Fresno, California, and oversees approximately $100 million in assets under management for 850 client households.

One of the best tax deductions for a small business owner is funding a retirementplan. Beyond any tax deduction you are saving for your own retirement. You deserve a comfortable retirement. If you don’t plan for your own retirement who will? You need to start a retirementplan today.

And as 2024 draws to a close, we wanted to highlight 24 of the most popular and insightful articles that were featured throughout the year (that you might have missed!).

Historically, advisors haven't had many avenues to manage clients' 401(k) plan accounts, since unlike traditional custodial investment accounts, advisors generally lack discretionary trading authority in employer-sponsored retirementplans. Read More.

Historically, advisors haven't had many avenues to manage clients' 401(k) plan accounts, since unlike traditional custodial investment accounts, advisors generally lack discretionary trading authority in employer-sponsored retirementplans. Read More.

By Jake Anderson, CFP ® , Wealth Planner When helping clients begin retirementplanning, the same questions often arise: What should my retirementplan look like? Although there are some basic guidelines, your financial life is as unique as your fingerprint. Looking for personalized retirementplanning advice?

Freelancing is liberating, but without a solid financialplan, it can also be unpredictable. As a freelancer, you juggle not only your craft but also your finances, taxes, and retirementplanning. That’s where financialplanning for freelancers comes in. Plan for taxes ahead of time 4.

As owners of financialplanning firms approach retirement, some may decide to sell to an external buyer, while others may plan for an internal succession. Sometimes, this succession plan can include the owner's child, providing an opportunity to keep the business in the family.

Brad is the Co-Founder & CEO of Intellicents, an independent RIA with 12 offices across the country and headquartered in Albert Lea, Minnesota, that oversees $6 billion in assets under management for more than 3,000 client households.

We’ve covered a lot of ground with regard to how various tax laws impact your retirementplans: pensions, IRAs, 403(b) and 401(k) plans. But we’ve primarily focused on the US income tax laws (the IRS) affect your plans – and there are many nuances that you need to take into account with regard to state tax laws.

The study also identified attributes of "top performing" firms across a range of metrics, finding that they are more likely than other firms to have a clear ideal client persona, client value proposition, and marketing plan.

Realistic RetirementPlanning My children have consistently (and kindly) remarked about how grateful they are to have been able to graduate (with honors) from fine universities without any debt. Our retirementplanning took a hit to do so. Much retirementplanning advice focuses on saving more and saving earlier.

Zack is the Director of FinancialPlanning and Participant Engagement of Greenspring Advisors, an RIA based in Towson, Maryland, that manages $2 billion of private wealth assets under management for 1,300 client households and advises on an additional $5 billion in retirementplanassets.

Within this framework, the concept of the five pillars of retirementplanning emerges as a valuable strategy. These pillars provide a comprehensive framework for building a resilient and sustainable plan. Another important aspect of investment planning is its role in combating inflation.

Also in industry news this week: While the FPA is going full steam ahead on its federal and state lobbying efforts to regulate the title “financial planner”, CFP Board is more focused on increasing recognition of the CFP marks. How firms can best leverage their internal data to improve the number of client referrals they receive.

There are some things in life you just can’t plan for: an unexpected illness, job loss, death of spouse, disability. And while experiencing one of these major events can drastically impact your life, having an effective financialplan can help ensure that it doesn’t ruin your financial well-being.

Liz is the co-owner of Pleasant Wealth, a hybrid advisory firm based in Canton, Ohio that oversees $146 million in assets under management for 522 client households.

There are many financialplanning considerations before, during, and after a divorce. A key part of the process from a financial standpoint is dividing the assets. Generally, couples split the value of their assets 50-50 (though not always). Here are some key considerations when financialplanning for a divorce.

But 20 years is a long time and most of us aren’t disciplined to let our assets sit around for 20 years because we live our lives in the present. And so the better you can match your income or returns to your expenses the more predictable you can make your financial life.

Additionally, financial habits such as lower contributions to retirementplans and reliance on tangible assets pose unique challenges. The post FinancialPlanning for the Latino Community appeared first on www.tobiasfinancial.com.

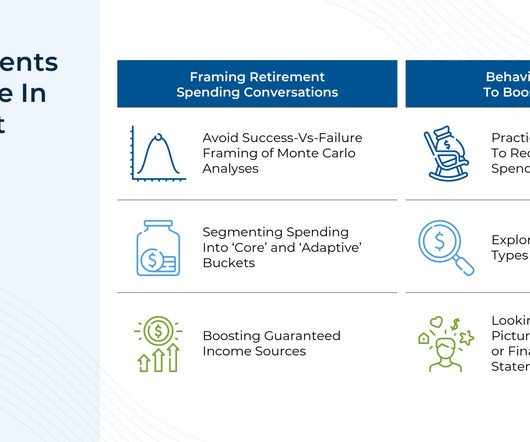

Financial advisors have a wide range of strategies at their disposal to create financialplans for their clients. This strategy is valuable because it generally allows for higher initial withdrawal rates than more static approaches that don’t accommodate clients willing to adjust their spending in retirement.

often fail to consider sequence of return, housing, longevity, health or family risks faced in retirement. Focus on Your RetirementPlan Rather Than a Magic Number. would be “How do I plan for retirement?“ Consider breaking assets into three columns: cash, investment assets and personal property.

Financialplanning is essential for anyone who wants to achieve financial independence. The goal of financialplanning is to help you reach your financial goals, whether that be retiring by a certain age or having the money to open a new business. Establish personal & business financial goals.

Welcome back to the 297th episode of the Financial Advisor Success Podcast ! Andy is the owner of Tenon Financial, a virtual independent RIA that oversees $70 million in assets under management for 43 retired client households. My guest on today's podcast is Andy Panko.

The key now, if you have recently retired or you are about to retire, is to start putting those different pieces together to form a complete picture of what you have and what you may need going forward. 401(k) This is the most common kind of retirement account. 1] Traditional IRA IRA stands for Individual Retirement Account.

When choosing a financial advisor, how they charge for their services can significantly impact your long-term wealth. The two most common pricing models are fee-only financial planners (flat-fee or fixed-fee advisors) and AUM-based financial advisors (who charge a percentage of assets under management).

No one cares about your financial well-being more than you, so it's important to have a financialplan for yourself. Knowing how to make a financialplan will allow you to save money, afford the things you really want, and achieve long-term goals like saving for college and retirement.

The end of the year is an ideal time to start planning for the year ahead and make sure you’re on target to achieve those goals. Asset and Liability Matching. Good financialplanning is all about asset and liability matching across time. Asset Allocation and Goals.

Of an estimated 104 million households seeking some level of financial advice, 88 million of those households want that advice from a financial professional. In this overview, we will explore the demographics of each stage, the financialplanning needs of people in each stage, and strategies for serving them.

Assuming that you have a financialplan with an investment strategy in place there is really nothing to do at this point. Ideally you’ve been rebalancing your portfolio along the way and your asset allocation is largely in line with your plan and your risk tolerance. Do nothing. Focus on risk. Look for bargains.

Your expenses get divided, your debts are lessened, and your assets are increased. In addition to this, you can save more and plan for more significant purchases with greater ease. For these reasons and several others, it is essential to follow specific financialplanning tips for dual-income families.

If you have student, personal or car loans, credit card debt or a mortgage, you need to have a plan on how to pay them off – and which ones to tackle first. While from a behavioral standpoint some suggest you should tackle low balance accounts first, a financialplanning approach suggests you tackle high interest rate debt first.

No one cares more about your financial well-being than you, so having a personal financialplan is important. Knowing how to make a financialplan will allow you to save money, afford the things you want, and achieve long-term goals like saving for college and retirement. What is a full financialplan?

Because of these differences, stocks and bonds accomplish different things in an asset allocation. But it helps illustrate the importance of diversifying within an asset class like fixed income. Morgan Asset Management. But correlations shift over time and within the asset class itself. Morgan Asset Management.

FinancialPlanning is vital. If you don’t have a financialplan in place, or if the last one you’ve done is old and outdated, this is a great time to review your situation and to get an up-to-date plan in place. Do it yourself if you’re comfortable or hire a fee-only financial advisor to help you.

Do you have a plan in place for your retirement? For many people, the extent of their retirementplanning includes signing up for the plan at work – which is often more of a starting point than a comprehensive retirementplan. There are also 457 plans available for some private companies.

For instance, after a lifetime of 'maximizing' their finances (likely seeing their net worth increase steadily over time), some clients might find it difficult to see their portfolio balances decline in retirement as they draw down their assets to support their lifestyles. Read More.

Last year’s considerable losses and market fluctuations underscore the need for clients to assess their retirementplans to ensure it aligns with their objectives, financial situations, timelines, and attitudes toward market volatility. You can help them start the year right by conducting a retirement checkup.

Retirementplanning is an essential aspect of financial security, especially as one transitions from a phase of regular income to relying on savings and investments. With increased life expectancy, the modern retirementplan may need to account for not only a longer life but also for the increased expectations during this phase.

Petersen, CPA, CFP ® , CP, Affluent Wealth Planning The holidays are upon us! That must mean it’s time to roll up my sleeves and get to work on year-end financialplanning – with an emphasis on 2023 income tax. Lastly, I allocate the retirementplan contributions between Roth and Traditional 401(k) accounts.

How much should Gen X have in their retirement accounts and when should they reach out to a financial advisor? Across their investable assets, Brian says they should have at least half a million or be aggressively saving at this point. Baby Boomers make up the majority of retirees, but Gen X is coming up next.

Know these 3 ages that can help you get the most out of your retirement accounts. At age 50, workers with certain qualified retirementplans can make annual “catch-up” contributions in addition to their normal contributions. 3 Now, many retirees have more time to let their retirement savings grow tax-free. 3] IRS.gov.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content