This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Historically, advisors haven't had many avenues to manage clients' 401(k) plan accounts, since unlike traditional custodial investment accounts, advisors generally lack discretionary trading authority in employer-sponsored retirement plans.

Pete is the Director of Sustainable Investing of Earth Equity Advisors, an RIA based in Asheville, North Carolina, that oversees approximately $200 million in assets under management for 250 client households. My guest on today's podcast is Peter Krull.

Historically, advisors haven't had many avenues to manage clients' 401(k) plan accounts, since unlike traditional custodial investment accounts, advisors generally lack discretionary trading authority in employer-sponsored retirement plans.

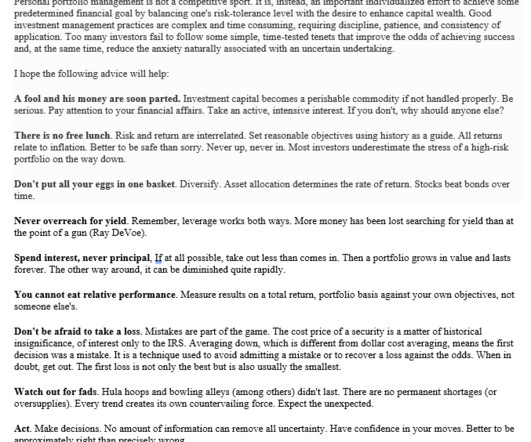

He eventually became president of Merrill Lynch AssetManagement, leading the division with a value-oriented approach and a focus on long-term fundamentals. He co-authored Investment Analysis and Portfolio Management , now in its fifth edition. Most investors underestimate the stress of a high-risk portfolio on the way down.

Category: Clients Risk. Determining the client’s risktolerance is not an exact science and requires you to communicate with your client. What Does The Word “Risk” Mean For Your Clients? For some clients, “risk” maybe something exciting or daring that they enjoy and not something they generally avert from.

If one stock makes up more than 10% of your overall asset allocation, it’s probably too much. A diversified portfolio is the cornerstone of a risk-adjusted investment strategy. Since single stocks don’t move like the broader market, you’re exposed to much greater risk. What is a concentrated stock position?

Enjoy the current installment of “Weekend Reading For Financial Planners” - this week’s edition kicks off with the news that a recent study found that advisory forms working with a younger client base tend to have relatively stronger growth in assets under management and revenue over time.

Stocks and bonds differ in many aspects, including the risk and return investors can expect. Because of these differences, stocks and bonds accomplish different things in an asset allocation. The choice between stocks and bonds depends on their individual circumstances, such as risktolerance, time horizon, and financial goals.

Investors have lots of questions when allocating to this trading asset class, including how much capital do you need? Chasing that performance has led the hedge fund space to swell to over 5 trillion in assets today, with forecasts topping 13 trillion globally by 2032. What percentage of your portfolio should be allocated?

While no investment is entirely devoid of risk, and there is always some degree of threat to your money when you put it in the market, you can managerisk and protect your investments with some strategies. It is essential to choose investments that match your risk appetite to avoid unnecessary stress and surprises later.

Asset Allocation: Developing a Long-Term Investment Strategy for Mission-Driven Organizations. When putting a plan in place, we believe it is critical for any mission-driven organization to develop an effective, long-term asset allocation strategy to manage its endowment assets. Tue, 09/06/2022 - 10:30. 70–90% vs. 80%).

He is the Chief Investment Officer of Asset and Wealth Management at Goldman Sachs. He’s a member of the management committee. He co-chairs a number of the assetmanagement investment committees. trillion in assets under supervision. At the end of 2008, we owned a lot of illiquid assets.

As a result, advicers have more options than ever to add value for their clients by tailoring investment portfolios that are specific to their unique needs, goals, and risktolerance. In this guest post, Robert Hum, a Managing Director and U.S. size, industry, location) of early mutual funds.

When it comes to managing your wealth and pursuing your financial goals, clarity can be key. Enter bucketing, a powerful strategy that helps simplify your financial planning by categorizing your assets into three time-based buckets: today, tomorrow, and the future. What Is Bucketing?

A portfolio review can help you: Assess your investment objectives and confirm they align with your financial plan Evaluate your time horizon and risktolerance Ensure proper diversification and asset allocation Review tax management strategies, including capital gains and the Net Investment Income Tax (NIIT) Monitor performance beyond just returns, (..)

However, it should be well understood that a client’s financial profile includes their risktolerance and their risk capacity. In this article, although we will be focusing on the latter one and why it is significant to determine your client’s risk capacity let’s first understand the difference between the two.

Review risktolerance and current asset allocation strategy It’s important to ensure your clients’ portfolios align with their risktolerance because taking too much risk can negatively impact their ability to navigate market fluctuations.

Your lifestyle, goals, family situation, and risktolerance will give a unique signature to your retirement plan. Develop Your Personal Asset Allocation Now that have your 401(k) and IRA open and funded, how can you determine the correct asset allocation for each? How much should I be saving?

Bill Huang ran the hedge fund Archegos Capital Management and they very famously ran up a stake of a billion dollars using leverage and very aggressive trading up to $20 billion before they ultimately just blew up. that’s right] You would have taken Oh my God I’m up 30% I gotta take some profits.

Capital gains Stocks, bonds, and other investment products are called capital assets. Whenever you sell a capital asset for a profit , you make a gain. The difference between your cost of buying the asset and the amount you sell it for is a capital gain. At the same time, you lower your exposure to the risks of each.

The financial advisor recommends rebalancing within the asset allocation. This is measured vs. a model specific to the client’s risktolerance. The client knows someone else (often the money manager) is driving the bus. The advisor and client work together to identify goals and work toward them.

Any investment strategy that does not incorporate your goals, time horizon, and risktolerance is flawed. Perhaps it’s time to rebalance and to rethink your ongoing asset allocation. Solid, well-managed active funds can also contribute to a well-diversified portfolio. Take stock of where you are. Costs matter.

When investing in dividend stocks, bonds, or funds, a higher dividend yield may make an asset look more attractive, but this metric alone doesn’t make a worthwhile investment. But as with any investment, there are always risks. Asset allocation Generally, dividend stocks tend to be older, more mature companies.

Each has unique benefits and drawbacks, and understanding these can help you decide which fits best with your financial situation, risktolerance, and goals. Drawbacks: Impacts financial aid: Assets in a 529 Plan can affect eligibility for financial aid.

An endowment is a portfolio of assets that is invested to provide support for a cause. Donations to endowment funds are tax-deductible, giving them a place in your overall financial management and tax plan. Managing a Charitable Endowment Fund Once an endowment is established, it must be maintained. What Is an Endowment?

When it comes to money management, there are a lot of different schools of thought. On the other hand, if you tend to struggle with budgeting or find financial planning overwhelming, then professional money management could be a better solution. Money management and financial planning are the first steps when DIYing your finances.

How to Choose the Right Wealth Management Firm in Kansas City Managing your wealth is a crucial aspect of financial success and security. Let’s look at key factors to consider when selecting the ideal wealth management firm in the Kansas City metro area. But with many options available, how do you choose the right one?

1] What are Your Investment Goals and RiskTolerance When selecting investments for your IRA, consider your investment goals and risktolerance. If you are younger, you may be able to take more risks because you have a longer time horizon to earn back potential gains and receive more income in the future.

When investors create an investment portfolio, they consider several factors, like risk, asset class, inflation, etc., However, what is equally critical when it comes to creating a portfolio is asset allocation and selection. Read more to learn about asset allocation and how it can impact your portfolio.

William Bernstein explains how to manage our emotions to avoid poor outcomes in markets. ” He manages client assets ($25m minimum) at Efficient Frontier Advisors. Dr. William Bernstein : You can think of investing metaphorically as a highway on which you drive your assets from your present self to your future self.

You see, financial advisors that focus primarily on wealth management can be costly to keep around. They charge either a percentage of assetsmanaged or a flat hourly rate that can run as high as several hundred dollars per hour, plus trading commissions and administrative fees. Personal Capital to the rescue.

In investments, having too high a return expectation with a lesser ability to take risks can disrupt your game. Having a very low-risktolerance can compromise achieving decent returns. This is the only way to create wealth by way of compounding in the long term.

They can assess your financial situation, long-term goals, risktolerance, and investment preferences to create personalized strategies. They can also help you optimize your savings and investment plans, ensuring that you maximize your earning potential while minimizing risks.

If so, this is a good time to revisit your asset allocation and perhaps reduce your overall risk. Manage your portfolio with an eye towards downside risk. Manage your portfolio with and eye towards downside risk. Learn from the past . Maybe they’re right. Click To Tweet. Need help getting on track?

How to Choose the Right Wealth Management Firm in Kansas City Managing your wealth is a crucial aspect of financial success and security. Let’s look at key factors to consider when selecting the ideal wealth management firm in the Kansas City metro area. But with many options available, how do you choose the right one?

10 steps to manage a financial windfall Expert tip: Keep living your life normally Factoring in taxes How do you deal with sudden financial windfall? Articles related to being wise with money Manage your large sum of money smartly! 10 steps to manage a financial windfall A situation like this might feel like a stroke of luck—and it is!

Rebalancing involves adjusting the mix of assets in your 401(k) portfolio to maintain a desired level of risk and return. Rebalancing a 401(k) refers to adjusting the asset allocation of your investment portfolio back to its original target percentages. This may lead to a higher or lower risk profile than initially intended.

Individuals can choose the investment options that best suit their retirement goals and risktolerance. Investment Options : Individuals should choose a provider that offers a wide range of investment options to meet their retirement goals and risktolerance.

Once you have your goals set, you can build your plan with any combination of the following elements: Budgeting and expense management: Create a detailed budget outlining income, expenses, and savings targets. Debt management: Develop a strategy to pay off existing debts efficiently, minimizing interest costs.

There are many options, but your top priority should be choosing an investment that aligns well with your goals and risktolerance. Note that Fundrise requires a 0.15% annual advisory fee and an annual assetmanagement fee of up to 0.85%. This asset class comes in many forms, including the website you’re reading.

Your asset allocation is the percentage of your portfolio that you distribute between different asset classes, like stocks and bonds. To rebalance your portfolio, you’ll buy and sell certain investments to realign to your accounts with your desired asset allocation. Why do you need to rebalance your portfolio?

When it comes to managing wealth and planning for a secure financial future, the services of financial professionals, such as financial advisors or wealth managers, are invaluable. Wealth managers and financial advisors offer a wide range of wealth management services designed to help clients achieve their financial goals.

On the flip side, park your cash in fixed-income products, and you’ll generate higher, more consistent returns than what a checking account would offer, but at the cost of being unable to withdraw your money on your terms, among other risks. This is where IntraFi Network Deposits come in.

Endowment and Foundation Challenges: Managing Charitable Gift Annuities ajackson Tue, 09/29/2020 - 14:00 The charitable gift annuity is one of a number of donor-friendly solutions that nonprofit institutions can offer to donors. However, the management of underlying assets in a gift annuity pool is a different matter.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content