This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Historically, advisors haven't had many avenues to manage clients' 401(k) plan accounts, since unlike traditional custodial investment accounts, advisors generally lack discretionary trading authority in employer-sponsored retirement plans.

Pete is the Director of Sustainable Investing of Earth Equity Advisors, an RIA based in Asheville, North Carolina, that oversees approximately $200 million in assets under management for 250 client households. My guest on today's podcast is Peter Krull.

Historically, advisors haven't had many avenues to manage clients' 401(k) plan accounts, since unlike traditional custodial investment accounts, advisors generally lack discretionary trading authority in employer-sponsored retirement plans.

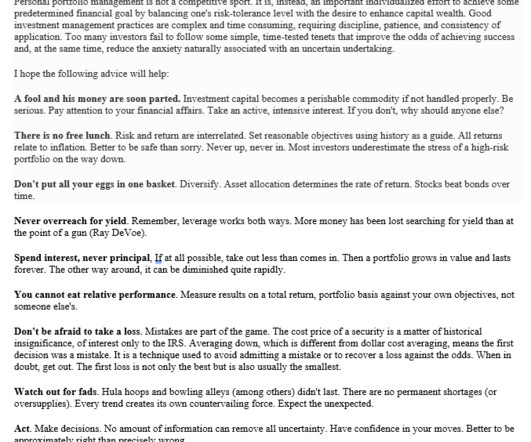

He eventually became president of Merrill Lynch Asset Management, leading the division with a value-oriented approach and a focus on long-term fundamentals. It is, instead, an important individualized effort to achieve some predetermined financial goal by balancing ones risk-tolerance level with the desire to enhance capital wealth.

Category: Clients Risk. Determining the client’s risktolerance is not an exact science and requires you to communicate with your client. What Does The Word “Risk” Mean For Your Clients? For some clients, “risk” maybe something exciting or daring that they enjoy and not something they generally avert from.

Enjoy the current installment of “Weekend Reading For Financial Planners” - this week’s edition kicks off with the news that a recent study found that advisory forms working with a younger client base tend to have relatively stronger growth in assets under management and revenue over time.

Enter bucketing, a powerful strategy that helps simplify your financial planning by categorizing your assets into three time-based buckets: today, tomorrow, and the future. By dividing your investments into these three buckets, you help create a clear plan for how and when your money will be used. What Is Bucketing?

Assuming that you have a financial plan with an investment strategy in place there is really nothing to do at this point. Ideally you’ve been rebalancing your portfolio along the way and your asset allocation is largely in line with your plan and your risktolerance. Focus on risk. Do nothing.

Stocks and bonds differ in many aspects, including the risk and return investors can expect. Because of these differences, stocks and bonds accomplish different things in an asset allocation. The choice between stocks and bonds depends on their individual circumstances, such as risktolerance, time horizon, and financial goals.

It is essential to choose investments that match your risk appetite to avoid unnecessary stress and surprises later. A financial advisor can help you understand your investment risktolerance. This article will focus on the risks of investing, how they impact you, and what you can do to determine your risk appetite.

In this article, we will explore three popular savings and investment options: 529 Plans, Roth IRAs, and Real Estate. Each has unique benefits and drawbacks, and understanding these can help you decide which fits best with your financial situation, risktolerance, and goals.

For more years than I’d care to name, I’ve been trying to put my finger on exactly why I have a such a huge problem with the traditional (Think: Riskalyze, now Nitrogen) risktolerance assessments in the financial planning profession. You can actually test various bear markets and adjust accordingly.)

Riskalyze signals an intent to rebrand itself away from ‘just’ risktolerance assessments to a broader focus on helping advisors grow clients and assets. Hearsay Systems rolls out a new small-to-mid-sized RIA platform for social media compliance and website design.

Asset Allocation: Developing a Long-Term Investment Strategy for Mission-Driven Organizations. When putting a plan in place, we believe it is critical for any mission-driven organization to develop an effective, long-term asset allocation strategy to manage its endowment assets. Tue, 09/06/2022 - 10:30. 70–90% vs. 80%).

It is for information and planning purposes only. Whether youre new to investing or have years of experience, taking a step back to evaluate your strategy can help ensure that your portfolio remains aligned with your objectives, especially in times of market uncertainty and volatility.

Last year’s considerable losses and market fluctuations underscore the need for clients to assess their retirement plans to ensure it aligns with their objectives, financial situations, timelines, and attitudes toward market volatility. Here are some key points to use with clients as you help them assess their retirement plans.

It’s really important from a financial well-being point of view for people to have their own individual authentic goals hopefully baked into some form of a financial plan. Brian Portnoy : Investing outside of a well-defined financial plan is speculation. It was just more for the sake of more.

There are many steps in building an investment portfolio, in this article, I’ll discuss how asset allocation and risktolerance are important considerations when investing. In simple terms, asset allocation is the mix of all the different types of investments you have in your portfolio. Some examples include U.S.

However, it should be well understood that a client’s financial profile includes their risktolerance and their risk capacity. In this article, although we will be focusing on the latter one and why it is significant to determine your client’s risk capacity let’s first understand the difference between the two.

The overall theme that were really getting at is you really have to be aware of your risktolerance and your financial plan, Chad shared. Are you comfortable with your current risk level? Do you have the right mix of assets to support your retirement goals? That instinct is a good one.

Among these are your longevity, lifestyle, comfort with market performance, sequence of return risk, current health, housing plan, proportion of fixed to variable expenses, proximity to children and so much more. often fail to consider sequence of return, housing, longevity, health or family risks faced in retirement.

When investing in dividend stocks, bonds, or funds, a higher dividend yield may make an asset look more attractive, but this metric alone doesn’t make a worthwhile investment. But as with any investment, there are always risks. Generally, investors don’t increase their risk profile as they move through retirement.

Rather I suggest an investment strategy that incorporates some basic blocking and tackling: A financial plan should be the basis of your strategy. Any investment strategy that does not incorporate your goals, time horizon, and risktolerance is flawed. Take stock of where you are. Photo credit: Flickr.

No one cares about your financial well-being more than you, so it's important to have a financial plan for yourself. Knowing how to make a financial plan will allow you to save money, afford the things you really want, and achieve long-term goals like saving for college and retirement. What is a financial plan?

Capital gains Stocks, bonds, and other investment products are called capital assets. Whenever you sell a capital asset for a profit , you make a gain. The difference between your cost of buying the asset and the amount you sell it for is a capital gain. At the same time, you lower your exposure to the risks of each.

For example, your plan might call for a 60% allocation to stocks but with the gains that stocks have experienced you might now be at 70% or more. This is great as long as the market continues to rise, but you are at increased risk should the market head down. Financial Planning is vital. Learn from the past . Click To Tweet.

Does your plan properly account for inflation, now and in the future? Let’s talk about the things you need to be thinking about right now in your financial plan. What is the inflation rate that Brian factors into financial plans? What is the inflation rate that Brian factors into financial plans?

They can assess your financial situation, long-term goals, risktolerance, and investment preferences to create personalized strategies. They can also help you optimize your savings and investment plans, ensuring that you maximize your earning potential while minimizing risks. But their support does not end there.

This bucket is for high-growth assets that may grow a lot in value but could see significant pullbacks during a downturn. The Safe Bucket often refers to assets that may not have a great upside but don’t have as much of a downside. This allows you to steadily build up your income-earning assets without having to time the market.

If one stock makes up more than 10% of your overall asset allocation, it’s probably too much. A diversified portfolio is the cornerstone of a risk-adjusted investment strategy. Since single stocks don’t move like the broader market, you’re exposed to much greater risk. What is a concentrated stock position?

1] What are Your Investment Goals and RiskTolerance When selecting investments for your IRA, consider your investment goals and risktolerance. If you are younger, you may be able to take more risks because you have a longer time horizon to earn back potential gains and receive more income in the future.

For one person, that might mean reassessing their risktolerance and portfolio holdings to make sure that they hold assets that will at least sustain their value or provide a safer return, such as an interest rate or a dividend yield. Why Meet with a Financial Advisor?

No one cares more about your financial well-being than you, so having a personal financial plan is important. Knowing how to make a financial plan will allow you to save money, afford the things you want, and achieve long-term goals like saving for college and retirement. Table of contents What is a financial plan?

But you might consider increasing your impact by setting up a structured , long-term philanthropic plan such as an endowment. An endowment is a portfolio of assets that is invested to provide support for a cause. Donations to endowment funds are tax-deductible, giving them a place in your overall financial management and tax plan.

Historically, staying the course and following a financial plan has outperformed rash investment decisions when there are times of uncertainty in the financial market. But it takes a strong plan—and no small amount of willpower—to do this. You can also look at cash management and debt reduction solutions.

When investors create an investment portfolio, they consider several factors, like risk, asset class, inflation, etc., However, what is equally critical when it comes to creating a portfolio is asset allocation and selection. Read more to learn about asset allocation and how it can impact your portfolio.

There are many options, but your top priority should be choosing an investment that aligns well with your goals and risktolerance. Open a 529 College Savings Plan. Open a 529 College Savings Plan. Note that Fundrise requires a 0.15% annual advisory fee and an annual asset management fee of up to 0.85%.

One area that often gets overlooked in the midst of planning is reviewing your financial habits and goals, so I’ve put together a short list of 3 areas to review before January. If you are unsure if your portfolio aligns with your risktolerance, time horizon and goals, reach out to us at Mainstreet and we would be happy to help!

Rebalancing involves adjusting the mix of assets in your 401(k) portfolio to maintain a desired level of risk and return. Rebalancing a 401(k) refers to adjusting the asset allocation of your investment portfolio back to its original target percentages. Click to compare vetted advisors now. What is 401(k) rebalancing?

While 529 college savings plans are a popular choice for many families, there are several other options worth considering. Let’s explore how 529 plans compare to Coverdell Education Savings Accounts (ESAs), pre-paid tuition plans, custodial accounts, and taxable investment accounts.

Take, for example, Erin Scannell , who, during his career, grew his firm to $4 billion in assets under management and handled up to 800 clients at one point. 02 Why a Well-Planned Transition Enhances Advisor Confidence? The first step to successful client transitions is meticulous planning.

The idea here is to build a plan around a specific goal. Add up all of your assets and subtract your debt. Debt is what you owe to any creditor, and assets include the value of all of your bank, brokerage, investment and crypto accounts, real estate holdings, and high-ticket vehicles like jets, boats and luxury cars.

Tweet “They have come a long way since inception and now allow you to invest in alternative assets like artwork and cryptocurrencies. The investment service includes access to dedicated financial advisors and assistance with managing your employer-sponsored retirement plan. Investment advice for employer-sponsored retirement plans.

For some, concentration risk might mean holding any amount of a single stock position in a company they work for. For others, concentration might feel suitable if they have significant other assets and/or if they have a high risktolerance or high risk capacity.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content