This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

One of the best tax deductions for a small business owner is funding a retirementplan. Beyond any tax deduction you are saving for your own retirement. You deserve a comfortable retirement. If you don’t plan for your own retirement who will? You need to start a retirementplan today.

By Jake Anderson, CFP ® , Wealth Planner When helping clients begin retirementplanning, the same questions often arise: What should my retirementplan look like? Your lifestyle, goals, family situation, and risk tolerance will give a unique signature to your retirementplan. How much should I be saving?

Like native-born workers, foreign workers need to think about saving for retirement, planning for their children’s college, managing healthcare costs, and all manner of other financial goals. For example, the tax benefits of certain accounts can sometimes work in the other direction if a non-U.S.-born

We’ve covered a lot of ground with regard to how various tax laws impact your retirementplans: pensions, IRAs, 403(b) and 401(k) plans. But we’ve primarily focused on the US income tax laws (the IRS) affect your plans – and there are many nuances that you need to take into account with regard to state tax laws.

Within this framework, the concept of the five pillars of retirementplanning emerges as a valuable strategy. These pillars provide a comprehensive framework for building a resilient and sustainable plan. Another important aspect of investment planning is its role in combating inflation.

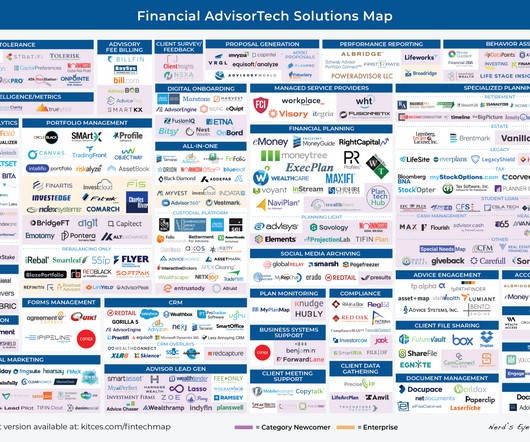

The survey also suggests that a firm's tech stack can affect its ability to attract and retain clients, with 93% of advisors who said they work with state-of-the-art technology reporting that they have added new clients as a result of another firm's bad technology, and 58% of all advisors surveyed reporting they had lost new business due to bad technology. (..)

Retirementplanning is a critical part of financial security that many women still overlook. However, remember that as a woman, you have a longer life expectancy than a man, which means retirementplanning is even more important. Consider early retirementtaxplanning. Educate yourself about finances.

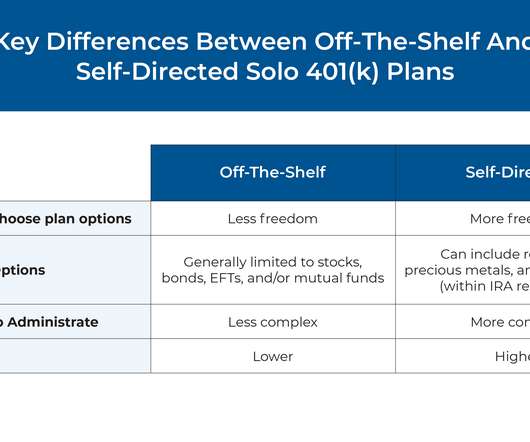

Among the several different types of retirementplans that are available to self-employed workers, solo 401(k) plans can offer the most flexibility and the ability to contribute the highest amount of tax-advantaged savings.

Also in industry news this week: The Office of Management and Budget (OMB) has completed its review of the Department of Labor's new "fiduciary rule ", indicating that it could be released in the coming days or weeks (though, like its predecessors, its ultimate disposition is likely to be determined in the courts) The IRS announced this week that it (..)

In late 2019, Congress passed the Setting Every Community Up for Retirement Enhancement (SECURE) Act, introducing several significant changes to retirementplanning. This shift has led financial advisors to explore new strategies for mitigating the resulting tax-planning challenges.

Retirementplanning can be a difficult and confusing process for couples. By focusing on a few key areas, setting financial goals, and doing your research, you can find ways to enjoy retirement together. Set Financial Goals In retirement, educate yourself on your financial situation and investment strategy.

Realistic RetirementPlanning My children have consistently (and kindly) remarked about how grateful they are to have been able to graduate (with honors) from fine universities without any debt. Our retirementplanning took a hit to do so. Much retirementplanning advice focuses on saving more and saving earlier.

The report suggests this might be due in part to increased RIA valuations and the assumption of some firm founders that next-generation employees won't be financially able to buy out the firm from them, though additional data indicates that many firms don't have career paths in place that could help next-generation advisors envision their path to firm (..)

Unlike most types of retirementplans, the SEP IRA is funded by the employer. Here’s more on what a SEP IRA is, tax benefits, contribution limits, and important deadlines. The SEP IRA is a straightforward and cost-effective way for small business owners to save for retirement. What is a SEP IRA?

Anyone who owns company stock will eventually have to decide how to distribute their assets — typically when there is a job change or retirement involved. When you transfer most assets to a taxable account, there will be income tax, but with company stock, you can take advantage of net unrealized appreciation (NUA). .

This month's edition kicks off with the news that digital estate planning platform Wealth.com has raised a whopping $30 million in Series A funding, following on the heels of Vanilla's follow-on $20M capital round just a few months ago – which on the one hand reflects the anticipated enthusiasm for solutions that can help advisors efficiently (..)

We start with several articles on retirementplanning: Why considering a client's retirement time horizon and spending flexibility could lead to more accurate (and often higher) safe withdrawal rates than the simpler "4% rule" Four unique risks retirees face when drawing down their assets, from sequence of returns risk to tax risk, and how financial (..)

Which could prove to be a boon for the financial advice industry as more consumers are willing to entrust their assets to an advisor (while at the same time possibly making it tougher for some advisors to differentiate themselves primarily by how they put their clients' interests first?).

It’s held jointly between you and your employer and contains contributions from you both, and it consists of stocks, bonds, mutual funds, and other assets. The contents of a 401(k) are not taxed until they are withdrawn and taken directly out of your paycheck, which may be useful depending on your financial situation.

This month's edition kicks off with the news that robo-advisor Betterment entered into a $9M settlement with the SEC for misrepresenting its tax-loss harvesting practices in its client agreements and marketing materials compared with its actual practices (e.g.,

often fail to consider sequence of return, housing, longevity, health or family risks faced in retirement. Focus on Your RetirementPlan Rather Than a Magic Number. would be “How do I plan for retirement?“ Consider breaking assets into three columns: cash, investment assets and personal property.

Andy is the owner of Tenon Financial, a virtual independent RIA that oversees $70 million in assets under management for 43 retired client households. Welcome back to the 297th episode of the Financial Advisor Success Podcast ! My guest on today's podcast is Andy Panko. Read More.

I've talked about my asset allocation before being overwhelmingly in cash or cash proxies, about 25% in "normal" equity investments, my exposure to crypto these days might be 2-3% up from 1/2 of a percent from when I bought Bitcoin in late 2018 but down from 6-7% when Bitcoin was higher.

Notably, this decision has provided both qualitative and quantitative benefits for these advisors, as 85% said they now have more control over their future and 80% saw their assets under management subsequently grow, with a median increase of 42%.

A recent study shows that while many consumers have expressed an interest in ESG investing, such funds within retirementplans have received limited allocations from investors. A survey showing how millionaires allocate their assets and the importance they place on the recommendations of their financial advisors.

equity valuations: “Baby-boomers’ huge flow of 401K plan contributions helped to drive equities higher; now that ~70 million Boomers are retiring, when do demographics flip this from a huge positive to a net drag?” This demographic cohort is simply not a seller due to retirement – the tax expenses would be too great.

This is before we get to the issue of capital gains taxes, which create a hurdle of (minimum) 20% on those pesky profits just to get to breakeven. Low Stakes : The most successful market timers are often those people who do not have actual assets at risk. When you get it wrong, it crushes your retirementplans.

That must mean it’s time to roll up my sleeves and get to work on year-end financial planning – with an emphasis on 2023 income tax. One consideration this year is that we’re two years from the expiration of the Tax Cuts and Jobs Act of 2017 (TJCA). AGI impacts multiple other tax considerations.

As you move toward retirement, you can’t be content just to accumulate assets. You need to develop a retirement income plan that can help guide you when it comes time to turn savings into sustainable retirement income. of Social Security benefits are paid to retired workers and their dependents.

It is March…that means you have just about 5 weeks left to get organized and submit your tax return. The tax deadline is April 18, 2023 (some taxpayers in disaster areas in California, Georgia and Alabama have an extended deadline). Gathering all your documents is crucial to complete a tax return free of mistakes.

Enjoy the current installment of "Weekend Reading For Financial Planners" - this week's edition kicks off with the news that SIFMA, which represents broker-dealers, investment banks, and asset managers, released a white paper that argues that CFP Board "increasingly functions as a de facto private regulator for CFP certificants" and proposes that CFP (..)

Early on in my savings journey I prioritized tax-deferred retirement accounts over all else. The set-it-and-forget-it nature of a workplace retirementplan is one of my favorite features. I like the ease and simplicity of 401k contributions coming out of my paycheck before it ever even touches my checking account.

Last year’s considerable losses and market fluctuations underscore the need for clients to assess their retirementplans to ensure it aligns with their objectives, financial situations, timelines, and attitudes toward market volatility. You can help them start the year right by conducting a retirement checkup.

In November 2022, proponents of the Massachusetts ‘millionaires’ tax (question 1) won their bid to nearly double the income tax rate on individuals with taxable income over $1M a year. As proposed, the new legislation would increase these tax rates to 9% and perhaps even 16% , respectively, starting in 2023.

This will allow you to maintain your tax-deferred status and continue to grow that nest egg for your retirement. If you’re not, put a plan in place, get on the right track. 2. Leave It Where It Is You may elect to do nothing and leave your assets in your old 401(k).

The 2017 Tax Cuts and Jobs Act (TCJA) brought sweeping changes to the tax code, impacting every taxpayer and business owner. Here’s a summary of the major tax law changes coming in 2026 and some steps individuals and business owners can take to prepare. For some, this may lead to more taxes paid on capital gains.

The clock is ticking for taxpayers who wish to minimize the taxes they will owe in the spring. The IRS does not tax what you divert directly from your paycheck into your retirement or health savings accounts. In 2022, the limit for a 401(k) plan is $20,500 or $27,000 if you are age 50 or above.

I don't minimize the benefits of being lucky but when someone understands how correlations work and how to implement some of the portfolio into low and negatively correlated assets, they are creating their own good luck.maybe? It's an interesting thought exercise. Luck can trickle into portfolio results in a bunch of different ways.

There are rules and regulations that can help you avoid higher taxes and penalty fees and help you structure your income to minimize taxes. Know these 3 ages that can help you get the most out of your retirement accounts. Age 59½ is the earliest you can withdraw funds from an IRA account and pay no early withdrawal penalty tax.

Key Takeaways: Preparing for retirement is important. But sometimes clients can use simplified tips to help them think through their plans. Knowing their monthly expenses, social security plans, long term tax implications, and more can be important steps in helping clients prepare for retirement. We all know that.

The same is true of retirementplanning – if you zero in on your portfolio and nothing else, you’ll miss out on some major factors that can make a significant difference in your retirement and ultimately your bottom line. Hurdle #3: Tax Efficiency Now we move on from death to taxes – the other “sure thing” in life.

Both are Individual Retirement Accounts meaning the account is opened and funded by the worker and are tax-advantaged accounts designed for retirement savings. Certain other types of retirement accounts are sponsored by employers and can be funded with both worker and employer contributions.

One of those options might be to set up a defined contribution plan such as a 401(k). [1] 1] A 401(k) will allow you to set aside some of your assets into a tax-advantaged account that can have market exposure and the potential to grow over time. [2] 4] This is a tax-advantaged account, much like a 401(k). [5]

Because many taxpayers earn too much to make pre-tax IRA contributions as they have a 401(k) at work. Although any investor with earned income can make a non-deductible contribution to an IRA (up to $7,000 in 2024-2025 if under age 50) and still take advantage of tax-deferred growth, it still may not be advisable. Yes and no.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content