This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Also in industry news this week: NASAA has proposed an amendment to its broker-dealer conduct model rule that would restrict the use of the terms “advisor” and “adviser” for broker-dealers and their registered representatives who are not also investment advisers or investment adviser representatives A recent study suggests that (..)

Daniel is the CEO of WMGNA, a hybrid advisory firm based in Farmington, Connecticut, that oversees approximately $270 million in assets under management for 200 client households. My guest on today's podcast is Daniel Friedman.

We start with several articles on retirement planning: Why considering a client's retirement time horizon and spending flexibility could lead to more accurate (and often higher) safe withdrawal rates than the simpler "4% rule" Four unique risks retirees face when drawing down their assets, from sequence of returns risk to tax risk, and how financial (..)

The report suggests this might be due in part to increased RIA valuations and the assumption of some firm founders that next-generation employees won't be financially able to buy out the firm from them, though additional data indicates that many firms don't have career paths in place that could help next-generation advisors envision their path to firm (..)

Anjali is the Founder of FIT Advisors, an RIA based in Torrance, California (but works virtually with clients nationwide) and oversees $65 million in assets under management for 45 client households. My guest on today's podcast is Anjali Jariwala. Read More.

While asset protection is a popular planning topic for High-Net-Worth (HNW) and ultra-high-net-worth clients, those who are not HNW are susceptible to the same threats to wealth. Notably, certain client assets have built-in creditor protection without the use of (often expensive) products or tools.

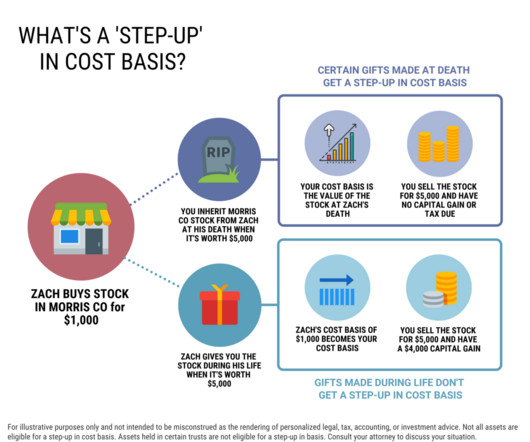

A step-up in basis is a tax advantage for individuals who inherit stocks or other assets, like a home. Heres how stepped up cost basis works on stock and other assets at death. Understanding step-up in basis at death If youve received an inheritance you may have questions about the tax treatment of certain assets.

As the year comes to a close, now is the time to review potential financial moves to help minimize your tax burden heading into 2025. Proactive year-end taxplanning can lead to significant savings and set you up for financial success in the new year. Find your next tax advisor at Harness today.

podcasts.apple.com) Retirement Retirement is a great time to do some creative taxplanning. readthejointaccount.com) Taxes What you need to know about paying taxes on your crypto trading. awealthofcommonsense.com) The best retirement withdrawal strategy is one you can live with.

justincastelli.io) Taxes Some speculation on what is next for the TCJA. kitces.com) Taxplanning and wealth management go hand-in-hand. downtownjoshbrown.com) How tax deferment can backfire. wealthmanagement.com) Asset location isn't job number one, but it is a job. thinkadvisor.com)

morningstar.com) Early in retirement is the time to do some taxplanning. nextavenue.org) Estate planning Mistakes to avoid in your estate planning. theretirementmanifesto.com) If you have a valuable collection you need a plan for its eventual disposition. whitecoatinvestor.com) On the challenges of solo aging.

As a result, there's a common line of thinking that people saving for retirement should avoid pre-tax retirement accounts entirely and contribute (or convert existing pre-taxassets) to Roth instead – regardless of which tax bracket they're in today.

Enjoy the current installment of “Weekend Reading For Financial Planners” – this week’s edition kicks off with the news that the SEC’s proposed “Safeguarding Rule” would significantly increase the number of investment advisers deemed to have custody of client assets and increase paperwork requirements for advisers (..)

Andy is the owner of Tenon Financial, a virtual independent RIA that oversees $70 million in assets under management for 43 retired client households. Welcome back to the 297th episode of the Financial Advisor Success Podcast ! My guest on today's podcast is Andy Panko. Read More.

This month's edition kicks off with the news that digital estate planning platform Wealth.com has raised a whopping $30 million in Series A funding, following on the heels of Vanilla's follow-on $20M capital round just a few months ago – which on the one hand reflects the anticipated enthusiasm for solutions that can help advisors efficiently (..)

Also in industry news this week: A probe by the Government Accountability Office found that the conflict-of-interest disclosures offered by many firms offering financial advice are often inadequate or confusing, making it hard for consumers to understand whether and when a financial professional is operating in their best interest A recent study has (..)

million in assets to both retire and pass on a legacy interest (though many have yet to establish an estate plan), according to a recent survey. Enjoy the current installment of "Weekend Reading For Financial Planners" – this week's edition kicks off with the news that affluent Americans believe they need an average of $5.5

Enjoy the current installment of "Weekend Reading For Financial Planners" – this week's edition kicks off with the news that the North American Securities Administrators Association (NASAA) released the latest edition its annual survey outlining the state of state-registered RIAs, showing that the number of state-registered firms and their assets (..)

Kamila is the CEO and Founder of Collective Wealth Partners, an independent RIA based in Atlanta, Georgia, that oversees nearly $25 million in assets under management for almost 175 client households. My guest on today's podcast is Kamila Elliott.

This shift has led financial advisors to explore new strategies for mitigating the resulting tax-planning challenges. Under the new law, non-spouse beneficiaries (with few exceptions) must now withdraw the entirety of an inherited IRA within 10 years of the account owner's passing rather than over their own lifetimes.

However, because many next-generation clients such as those who are Millennials and Gen Zers are still building their assets up, paying $10,000 or more in advisory fees each year may not be feasible for them… at least not yet.

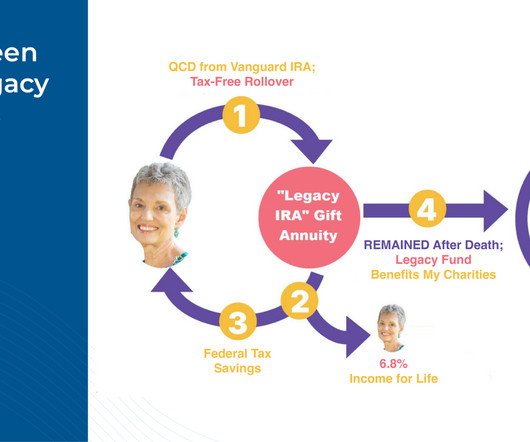

However, the caveat with current CGAs has been that they could only be funded with after-tax dollars before the donor’s death, meaning that if an individual only had tax-deferred funds (e.g., But the SECURE 2.0

Like individuals, businesses holding investments and other capital assets should consider other income, gains, and losses when determining when to sell capital assets. Defer income Clients may consider putting off asset sales or delaying receipt of other income until next year to reduce 2023 taxable income.

House of Representatives and is now being considered in the Senate would increase the number of firms classified as “small entities” and would require the SEC to assess the impact of proposed regulation on this newly enlarged class of investment advisers (which tend to have fewer compliance staff and resources available compared to larger (..)

Other reasons involve changes in investment strategy, portfolio rebalancing, or a simple desire to exit a specific asset class. Capital gains can result from the sale or exchange of capital assets, such as fund interests or portfolio company stock. What tax strategies optimize secondary investments? FIRPTA planning using a U.S.

As we begin our countdown to 2024, it is a great time to ensure your year-end taxplan is in place. Taxplanning is a vital component of meeting your overall financial goals. Our team of professionals is here to assist with your financial and taxplanning needs. You can access the webinar recording here.

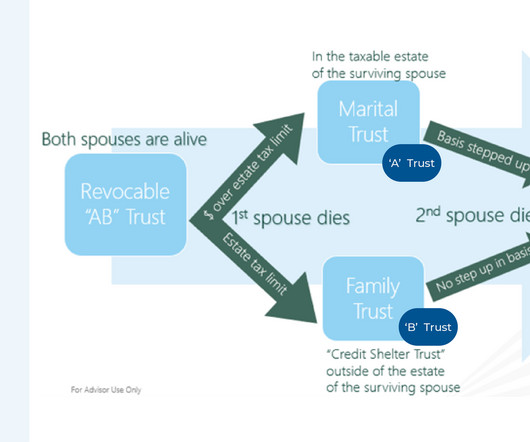

Given how frequently the tax code changes, advisors can add value for clients by ensuring their estate plans are aligned with current law to meet the clients’ objectives, and not with past rules that may no longer apply to them. However, the passage of TCJA resulted in the estate gift tax exemption nearly doubling (from $5.6M

Choosing whether to fund a trust with your assets is an important decision in the estate planning process. Here are three main reasons you may want to consider putting your assets in a trust. Funding a trust means retitling assets in the name of your trust. There are no changes to the tax treatment of these assets.

If you've heard of a DAF and are curious about incorporating it into your giving and taxplanning strategy, this article is for you. Key Takeaways: Contributions to a donor-advised fund reduce your tax bill in the year your contribution is made. What is a Donor Advised Fund?

By rolling the account into their own, spouses can consolidate assets, although they need to be wary of the 10% penalty on early withdrawals if under 59. This flexibility allows EDBs to extend the tax-deferred growth of the inherited funds over a longer period, which is a huge advantage in strategic taxplanning.

While most taxpayers dont need to worry about estate and gift taxes, having significant assets can make them a challenge. Also, like most UHNW individuals, you may have income from several sources like investments, real estate, and business interests that may require special taxplanning. And, if the U.S.

As a whole, these regulations introduce significantly more complexity to the process of taxplanning around retirement accounts, particularly after the death of the account's original owner. Act passed in late 2022.

Cost-saving taxplanning can be much more difficult to implement after your company is well-established and has reached the stage where an IPO, merger, or acquisition becomes a likely event. ISOs can only be issued to employees, and the company issuing the ISO cannot take a tax deduction.

Apex Fintech Solutions noted that the average advisor rings in at a cool 97% retention rate for acquired clients, suggesting that net new assets may provide a clearer lens for growth than the more traditional AUM metric. In the same vein, they also highlighted that hybrid firms (i.e.,

Podcasts Christine Benz and Jeff Ptak talk with Tim Steffen, director of taxplanning for Baird. linkedin.com) Fintech Most people don't need asset management, they need paycheck management. morningstar.com) Michael Kitces and Carl Richards talk about repurposing lessons from clients for content. Budge looks to solve this.

One important aspect of this approach is to ensure that your overall asset mix remains approximately the same after you implement this strategy. You will need to identify investment options for reinvestment of the proceeds that are similar to those you liquidate for tax purposes.

Tax loss harvesting involves selling losing investments to offset capital gains, thus limiting the taxes you owe. While it doesn’t always make sense to take a loss on investments, evaluate your portfolio and consider whether selling some poorly performing assets may make sense in your situation. Charitable giving.

Traditional IPO: Valuation, Lockup Period, and Employee Equity Founders have more options for reducing the tax consequences of an acquisition Founders are generally in the best position to engage in taxplanning and limit the taxable consequences associated with an acquisition.

The Bible doesnt lay out a detailed blueprint for modern estate planning, and thats okay. These guidelines include: Stewardship: Recognize that all assets belong to God and plan accordingly. Charitable Giving Plan: Develop a strategy for supporting Christian ministries and charities.

What are appropriate checklists for year-end taxplanning? Tax planners often develop checklists to guide taxpayers toward year-end strategies that might help reduce taxes. Certain tax benefits may be available if you can claim an individual as a dependent. Family taxplanning. Financial investments.

As you move toward retirement, you can’t be content just to accumulate assets. You need to develop a retirement income plan that can help guide you when it comes time to turn savings into sustainable retirement income. A professional financial advisor can help you create a retirement plan that works for your needs.

Advisors are being asked to provide their clients with a full suite of solutions, ranging from estate and taxplanning to portfolio management, and everything in between. Clients are increasingly eager to gain access to fully customizable solutions that meet their individual needs.

When you have the resources to make an impact, this type of planning helps you pinpoint what you want to accomplish for your family, community, and society. Steps to Setting Up a Philanthropy Fund Taking the proper steps in the beginning can give your charitable giving plan a solid foundation.

TaxPlanning: Things to work on before year-end. Though it may seem that we’ve just put last tax season to rest, now is the time to work on adjustments to optimize your 2022 taxes! Though it may seem that we’ve just put last tax season to rest, now is the time to work on adjustments to optimize your 2022 taxes!

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content