This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

This week, we speak with Savita Subramanian , head of US Equity and Quantitative strategy at Bank of America. He helps to oversee DoubleLine’s investment management committee implementing policies & processes, He is a member of DoubleLine’s executive management and fixed income asset allocation committee.

We do discretionary macro trading, which is typically a portfoliomanager — and we have some number of portfoliomanagers, 15 or 18 different portfoliomanagers that independently manage a book of, you know, risk assets. We’ve got central banks all over the world starting to move.

All of their portfoliomanagers not only are substantial investors in each of their funds, but they do a disclosure year that shows each manager by name and how much money they have invested in their own fund. Heather Brilliant : I worked at Bank of America and, and they had a wonderful corporate finance training program.

There are about 13 different portfoliomanagers each focused on a different sub-sector. And when they look at a sector, they want to be long, the very best stocks at the best valuations they can, and short the worst stocks at the worst valuations. And I didn’t have a background that banks wanted.

My mental image was that he worked in the bank of, back of a bank approving mortgage applications. Now I do fundamental side research portfoliomanagement, which I just, 00:08:20 [Speaker Changed] So, so you joined GMO, there’s 60 people, 30 years. Jeremy’s never really been a portfoliomanager.

stocks and fixed income securities will probably languish when the central bank begins to withdraw record stimulus. Federal Reserve policymakers forecast that they will likely start tightening this year for the first time since 2006, bringing an end to record liquidity, even as central banks from Europe to Japan push unprecedented stimulus.

So, first, I found the book to be quite fascinating, very in depth and you managed to take some of the more technical arcana and make it very understandable. You began as a central bankportfoliomanager in Finland. So, that relationship actually already started when I was a portfoliomanager, right?

Michael is the portfoliomanager of Broome Street Capital, a fund that specializes in m&a and event-driven trading. You could make a case that banks best days are behind us. But if they weren't, I certainly wouldn't know whether to choose Bank of America or Wells or, or go with a company like Visa or Mastercard.

In Engines That Move Markets, a 2002 book about the cycles of technology investing, Alasdair Nairn defines “bubbles” as periods when investors appear to suspend rational valuation, much as they had during the dotcom craze shortly before the book was published. Unsurprisingly, as volume has increased, so have valuations. Possible Signs.

Mick Dillon and Bertie Thomson, portfoliomanagers of the strategy, are keenly aware of the events that have disrupted markets over the last five years, yet equally aware of the risk to the portfolio if they let those events distract them from their research and investment decisions. 6th Edition, 2015. We call this the win-win.”

Mick Dillon and Bertie Thomson, portfoliomanagers of the strategy, are keenly aware of the events that have disrupted markets over the last five years, yet equally aware of the risk to the portfolio if they let those events distract them from their research and investment decisions. 6th Edition, 2015.

So, yeah, I had a career in investment banking with Jefferies, and it was a really good professional experience because I do have the opportunity to work in M&A, equity and debt financing. I had the chance to be part of some very interesting transactions in the banking space. billion deal. BERRUGA: Yeah.

Throughout this period, we often saw windows in which we believed that European valuations were more attractive, but we were cautious due to Europe’s high debt levels and struggles to generate economic growth. large-cap managers have been able to beat the market consistently. Further, we see room for the European economy to grow.

Throughout this period, we often saw windows in which we believed that European valuations were more attractive, but we were cautious due to Europe’s high debt levels and struggles to generate economic growth. large-cap managers have been able to beat the market consistently. Further, we see room for the European economy to grow.

Then, in mid-August, the People’s Bank of China relaxed controls on the yuan—which has been pegged to the dollar—and allowed a 3% decline in a matter of days. By Mick Dillon, CFA, PortfolioManager, Global Leaders Strategy; Priyanka Agnihotri, Equity Research Analyst. By Stephen Shutz, CFA, Tax-Exempt PortfolioManager.

And so to your point, I was a public portfoliomanager, started as a tech analyst and made my way to associate portfoliomanager and then began managing public portfolios in 1996. Where, 00:06:25 [Speaker Changed] Where were you managing those for in 96? The more private side of the street?

They could put me running a grain elevator, gosh knows where I interviewed with consulting companies and banking companies. And eventually I got a job offer at Donaldson Lefkin Jenette, which is no longer here, but it was an investment bank of, of some note at the time. I interviewed with some airlines. Why aren’t you?

It wasn’t too long ago when investments would mean going to the bank and following the advice of the bankers or calling in neighborhood uncle to buy term-deposit certificates or insurance. You can also undertake the globally recognized course in risk management from GARP (Global Association of Risk Professionals).

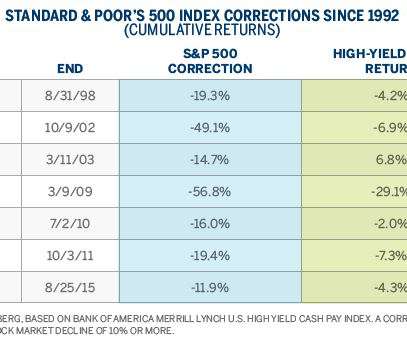

In 2015, though, three trends began to weigh on stock prices: equity valuations rose above their historical average, record central-bank stimulus failed to fuel faster growth, and corporations, having already wrung out significant inefficiencies, made fewer gains in streamlining and improving profit margins, especially in the U.S.

As with many things in life, the truth is somewhere between the extremes: While both simulated and real-world data suggest momentum may not be suitable as a driver of long-term asset allocations, we believe momentum considerations can be integrated in a cost-effective way to help inform daily portfoliomanagement decisions.

I’m joined here today by Ryan Kelley, Lead PortfolioManager and Research Analyst for Bell. But before we go there, maybe a couple of comments about the banking crisis that occurred earlier this year in March. Banking Crisis – Key Points 05:25 Ryan Kelley: Sure. And this was actually true of a number of banks.

Maintaining liquidity allows a portfoliomanager to snap up new opportunities such as General Dynamics, whose shares have risen 14% this year as of September 6. Barclays Indices are trademarks of Barclays Bank PLC. small-cap stocks. Compared with large caps, small-cap companies generally sell at a lower price-to-sales ratio (1.1

Maintaining liquidity allows a portfoliomanager to snap up new opportunities such as General Dynamics, whose shares have risen 14% this year as of September 6. Barclays Indices are trademarks of Barclays Bank PLC. small-cap stocks. Compared with large caps, small-cap companies generally sell at a lower price-to-sales ratio (1.1

Fed Vice Chairman Stanley Fischer said in June that the central bank is carefully monitoring whether investors “take on risks they cannot measure or manage.”. By Mick Dillon, CFA, PortfolioManager, Global Leaders Strategy; Priyanka Agnihotri, Equity Research Analyst. Europe's Slow Climb.

I was actually running the Investment Banking Club at BYU, and you know, thought I was interested in that, interested in going to Wall Street. Tell us a little bit about the corporate culture which is decidedly different than the typical Wall Street bank. I just signed a whole bunch of bank docs through DocuSign on my laptop.

Corporate Investment Management. Hedge fund management. PortfolioManagement. Understand concepts of valuation, fixed income securities, valuation, macroeconomics, and volatility of international markets. Asset Management. Corporate Banking. Credit Risk Management. Securities analysis.

This entire process is known as investment analysis where you use multiple valuations to understand and analyze the market along with those of different firms, industries, and sectors. All of the aforesaid factors need to be considered to find the investment instrument for your needs.

The academic thesis that equity managers as a whole will approximately equal overall market returns is followed by a corollary: Some managers will outperform for periods of time, but it is impossible to predict which manager will deliver favorable results, or when they will do so—in other words, outperformance (alpha) is random.

The academic thesis that equity managers as a whole will approximately equal overall market returns is followed by a corollary: Some managers will outperform for periods of time, but it is impossible to predict which manager will deliver favorable results, or when they will do so—in other words, outperformance (alpha) is random.

With traditional assets like stocks and bonds at high valuations, the implications for future returns of those assets may be underwhelming. It is not representative of an actual portfolio. When investing in alternatives, we seek long-term partnerships with portfoliomanagers and teams that possess specific talent and skill.

With traditional assets like stocks and bonds at high valuations, the implications for future returns of those assets may be underwhelming. It is not representative of an actual portfolio. When investing in alternatives, we seek long-term partnerships with portfoliomanagers and teams that possess specific talent and skill.

For instance, while non-financial indicators in fundamental corporate debt analysis assess management teams, in the case of sovereigns, the analysis involves evaluating central bank independence, quality of institutions, and the domestic and international political landscape. nd.edu/our-work/coun-try-index/) and Brown Advisory.

For instance, while non-financial indicators in fundamental corporate debt analysis assess management teams, in the case of sovereigns, the analysis involves evaluating central bank independence, quality of institutions, and the domestic and international political landscape. nd.edu/our-work/coun-try-index/) and Brown Advisory.

For instance, while non-financial indicators in fundamental corporate debt analysis assess management teams, in the case of sovereigns, the analysis involves evaluating central bank independence, quality of institutions, and the domestic and international political landscape. nd.edu/our-work/coun-try-index/) and Brown Advisory.

Both types of error are due to a combination of either mis-assessing the business quality or its valuation (or both). Our 10/10/3 valuation framework using a 10% weighted average cost of capital is undoubtedly conservative and ends up with us missing some big opportunities as type 2 errors of omission. 13 It’s a win-win.

banking crisis in 1Q23 and this is undoubtedly not an exhaustive list. Sometimes factors are short and sharp as seen with the US banking crisis earlier this year. To be clear, we would love to have more investments in any diversifying business or sector but every investment must first pass all our tests, particularly valuation.

Investment banks were not really a known concept in the area where I grew up. I lined up a bunch of job interviews with a variety of banks. So I got to know banks a little bit. So I interviewed with a bunch of banks, got a number of job offers by the end of the week, and joined Goldman Sachs in October 1998.

But it was a tremendous experience because I had started off in bond trading, worked my way into portfoliomanagement and running the bond indexing team for a number of years, and then I got asked to take this responsibility, which was much broader. DAVIS: Where international equities, because of valuations, probably 7% to 7.5%.

And the, you know, obviously just my personal opinion, but I think at that particular point in time, all of the investment banks were bankrupt or insolvent. Valuations tended to crash and burn very, very cheap valuations tended to do well. It was, we wanted to have the absolute best software for the way we managed money.

I started my career as a bank teller, but fell in love with markets. MIAN: So Stray Reflections is a macro advisory and community that works with portfoliomanagers, CIOs around the world. The fact that you’ve got declining risk appetite, declines are prolonged, deep and valuations mean revert.

I was born in London and when I was three and a half, my father got a job for the World Bank in Washington DC So we all moved to Washington DC Then just before my 10th birthday, my father was posted to Bangladesh for four years. 01:04:39 [Speaker Changed] I think it was the Journal of PortfolioManagement.

And then very soon after, you know, bear Stearns fails, Lehman Brothers fails, the cracks were massive and there were so much for selling from the trading desks at the banks. And we, we feel that a lot of phone calls, I think the most nervous we became was when the banks started failing. That had mismatched assets.

It’s just a fascinating conversation about looking at the world from both bottoms up and top-down, as well as thinking about what valuations are like, how likely are macro events, the impact you’re getting not just the return on capital, but as famously said in fixed income, a return of your capital. Every bank had balance sheet.

Interestingly, for many years prior to the crisis, the portfolio changed very little in value or in the composition of its holdings, which include Treasury securities, mortgage backed securities and other types of loans. A number of thoughts are swirling in the wake of these policy and leadership shifts.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content