This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Budgeting is one of the most important financial habits to develop. There are so many budgeting methods out there to choose from, but it’s not just creating a budget that will set you up for financial success. How do I plan for variable vs fixed expenses in my budget? What are average expenses for a household?

This information is critical if you want to create a budget and manage your money correctly. I’ll also share some budgeting and side hustle tips so you can get the most out of the money you earn. In your budget, you should plan to set aside money to cover future expenses, such as a vacation, a house downpayment, retirement , etc.

Retirementplanning can be a bit complex. There are multiple factors to weigh in, right from healthcare and inflation to estate planning, business succession planning, tax planning, and more. However, the main drawback to this can be the lack of foresight regarding what and how to plan.

If you don’t feel like you truly have a strong handle on your finances, one possible cause for that is using a budgeting method that doesn’t work. While not everyone needs a to-the-penny balanced budget, some type of budgeting strategy or template is really important if you want to know where your money is going month after month.

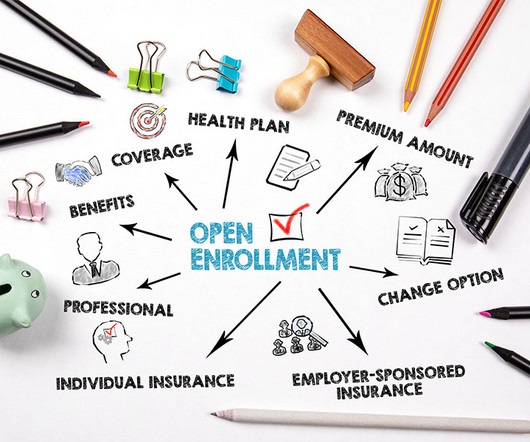

However, choosing the right Medicare plan is crucial to ensure that you have the coverage you need as you move into retirement. Whether you’re enrolling for the first time or considering a change, these tips will help you choose a plan that fits your healthcare needs and budget. Talk to us today!

If you’re really struggling financially and aren’t sure which problem to tackle or how, budget counseling can help. Table of contents What is budget counseling? Does budget counseling affect your credit score? Articles related to counseling and budgeting Consider budget counseling to get your finances in order!

You can start to gauge what you need and what needs to change about your financial plan in order to make the most out of your retirement. This is also the time when considering medical insurance and Medicare options are both important. [1]

You can use this online tool to help you find plans. [2] 2] You can also call 1-800-MEDICARE to find out which plans are in your area. [2] 2] But before choosing a plan, make sure that it aligns with your financial situation and is the best fit for you personally. Unfortunately, exact medical costs are hard to estimate.

Without a proper retirement nest egg, those 10 years could be met with a personal financial crisis. Set a Budget (and Stick to It) While seemingly a basic concept in the financial planning toolbox, a budget can uncover bad spending habits unbeknownst to people. 3 This excludes long-term care.

As a retiree, medical care will likely become more important, so you’ll want to ensure that you have reliable coverage and access to hospitals and specialists. One of the most common misconceptions is that Medicare will cover your medical expenses if you retire abroad.

Create a Post-RetirementBudget Many people underestimate how much they will need to cover living expenses in retirement. Creating a detailed budget that includes housing, food, transportation, travel, medical expenses and fun activities will help you understand what your financial needs will be.

If you want to know how to build up your wealth from scratch, this wealth accumulation plan will help. Create a budget. Try using something like the 50/30/20 budget. There are many other budgeting options, as well, like the 70/20/10 or the 30/30/30/10 budget. Have a will and estate plan.

Taxes & RetirementPlans Tax law seems to get more complicated every year. This can be paired very nicely with charitable giving. · Contribute to your employer sponsored retirementplans and other retirementplans – This would include any catch-up contributions for of-age individuals.

You can start to gauge what you need and what needs to change about your financial plan in order to make the most out of your retirement. This is also the time when considering medical insurance and Medicare options are both important. [1]

This data can serve as a baseline for tailoring your retirementplan, taking into account factors such as inflation, your current age, and your desired retirement age. Calculating potential housing costs accurately is fundamental for developing a realistic retirementbudget. of overall expenses.

If you wish to have a firm grip on your finances and want to learn about different strategies related to investing, tax-saving, or retirementplanning, consult with a professional financial advisor who can advise you on the same. You need help creating a budget. What to expect when meeting with a financial advisor?

The importance of understanding financial literacy basics Financial literacy covers several topics , including budgeting, banking, investing, handling debt, and planning for the future. Good financial planning is the key to success. And budgeting isn’t as tricky as it sounds.

Because retirement finances are much more about prediction than they are about facts and assurances, it can be hard to feel confident that you will have enough to carry you through your entire retirement. According to traditional wisdom, you want to withdraw 4% of your 1 million dollars in your first year of retirement. [3]

Creating a plan for the costs of parenthood can be important to discuss with your clients who plan to raise children. Add to those initial costs the ongoing medical care for a child as they age. 4 However, your clients will only qualify for an HSA if they have a High Deductible Health Plan (HDHP).

In our planning with clients, we like to employ a “pay yourself first” approach, especially as it relates to retirementplanning. You may have been contemplating starting contributions to a retirementplan, or you may have been contributing small amounts and are worried that you are behind in the game.

Healthcare Costs After Retirement — Securing Your Parents’ Future Retirement is a long-awaited phase of life where individuals can enjoy the fruits of their labor and enjoy well-deserved rest. With medical expenses on the rise, planning for healthcare during retirement becomes crucial to ensure a secure future.

Healthcare Costs After Retirement — Securing Your Parents’ Future Retirement is a long-awaited phase of life where individuals can enjoy the fruits of their labor and enjoy well-deserved rest. With medical expenses on the rise, planning for healthcare during retirement becomes crucial to ensure a secure future.

They both have decent-paying jobs, but their retirement savings are nonexistent. They have two kids, one of whom had significant medical problems as a young child. Of course, they can also try figuring out retirement on their own, and many people do. Retirementplanning isn’t a test—it’s life.

Often this means retirees must make significant compromises in their purchases and budgets, which can lead to undesirable outcomes. Retirees should evaluate their budget, identify areas where they can cut expenses and prioritize healthcare-related costs. A reduced COLA can also indirectly impact retirement savings.

Often this means retirees must make significant compromises in their purchases and budgets, which can lead to undesirable outcomes. Retirees should evaluate their budget, identify areas where they can cut expenses and prioritize healthcare-related costs. A reduced COLA can also indirectly impact retirement savings.

But if you don’t take an active role in the finances, start by making a habit of reviewing your accounts, keeping track of bills and talking regularly with your partner about your budget and money goals. Women are also more likely to work part time or lower paying jobs that do not offer 401(k)s or other retirementplans.

De-clutter Your Budget (Aka Spending Plan). The holiday season often marks increased spending, so it’s a good time to haul out your family budget. . Instead, start thinking of your budget as a spending plan. Your spending plan is a guide to help you use your money in ways that mean the most to you.

We talk about padding retirementbudgets for unbudgetable expenses by $1000/mo or some other number relevant to your circumstance and history with unexpected one-offs. Eating well and exercising effectively provides the opportunity to avoid being vulnerable to rising medical costs by not having to pay for prescriptions.

RETIREMENTPLANNING The Four Phases of Retirement Schedule a Complimentary Financial Review CLICK HERE TO SCHEDULE. Retirementplanning has become increasingly difficult as the cost of living continues to rise. This phase occurs while you are still working but nearing retirement age. Early Retirement.

Paul also took care of the family finances—everything from paying bills monthly to managing the couple’s assets and retirementplanning. I would also recommend that Margaret enlist the help of a financial planner, who can help her set a budget and undertake the next step: detection.

You can’t negotiate your bills Many people assume that their bills, such as their cable, cell phone, or even medical bills , are non-negotiable. The sooner you begin retirementplanning, the better off you’ll be later. However, this is not always the case. Look for categories where you can cut back on your spending.

Someone may be trying to use your insurance for medical procedures or medicine. You should ask for any associated medical records and let your medical providers know. And while you're at it, be sure to review other aspects of your financial health , such as your retirementplan and your budget.

No matter your age, you may save for retirement. Make your savings allocations a part of your monthly budget, like any other bill. You may withdraw the money tax-free as needed to pay for qualified medical expenses. As you get nearer to retirement, you may take advantage of the increased limits for retirement contributions.

Housing market trends, such as demand and supply in your area, can also influence your plan. Others, such as retirementplanning or buying a home, require a long-term commitment. No matter how meticulously you plan, your financial safety net must account for every possible worst-case scenario.

For example, you want to travel in your retirement years. You’ll need to budget more retirement savings for travel but might need less for housing costs. You’ll want to make sure to include education savings in your retirementplanning. Ongoing health conditions or concerns will affect retirement needs.

Instead, they start piling up right when you plan to conceive. Regular medical tests, doctor consultations, quality care, a good diet, and more, start to affect your budget even before you deliver the baby. And, once your baby comes to life, your financial budget can suffer if you do not prepare well.

Finding extra money in your budget to invest can seem like an impossible task. For example, contributions to traditional IRAs (but not Roth IRAs) and most employer-sponsored retirementplans are generally tax-deductible. Ad Looking forward to your retirement? Set a Contribution Schedule and Stick With it. Low enough?

Financial security is when you have enough financial resources to cover basic needs and unexpected expenses, such as medical bills. 4 Milestones to financial independence Having financial independence means that you can retire early or pursue your passions without being held back by financial constraints. What about financial security?

Just be a budget whiz, stay on top of those finances, and you’ll find that $30 an hour can go a long way. With a solid budget, you’ll pave the way for a bright financial future by saving for the essentials, like retirement, emergencies, and other endeavors. Retirement/Savings $832.00 Retirement/Savings $832.00

Below are 6 common financial planning mistakes physicians make: Even though financially well-off, physicians tend to make several financial mistakes. Not creating a comprehensive financial plan Financial planning for physicians and healthcare professionals is essential. A budget is like a snapshot of your financial health.

De-clutter Your Budget (Aka Spending Plan). The holiday season often marks increased spending, so it’s a good time to haul out your family budget. . Instead, start thinking of your budget as a spending plan. Your spending plan is a guide to help you use your money in ways that mean the most to you.

To maximize your earnings at this level, focus on financial planning and budgeting, as well as on improving your skills and knowledge. Follow a Budget Creating a budget is an essential step in setting yourself up for success when it comes to achieving your financial goals.

As was the case for 2022 we're saving about $1000/mo because we can get away with catastrophic coverage and by Blue Cross' estimate, another $500/mo on other medical expenses. We might spend $100/mo on supplements but that is in our grocery budget. Vitamin D and zinc are cheap, turmeric and magnesium glycinate are expensive.

Not only will you save thousands of dollars by avoiding medical bills, but your health is also the biggest contributor (or barrier) to accomplishing your goals. A great place to start is to create a budget that helps you to know where all your money is going each month. Prioritize health Health is wealth, baby.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content