This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Fran is the CEO of Toler Financial Group, an RIA based in Silver Spring, Maryland, that oversees nearly $200 million in assets under management for 280 client households.

Travis is the founder of Student Loan Planner, an RIA and student loan consulting company based in Chapel Hill, North Carolina that serves nearly 1,400 households with ongoing financial planning (as well as consulting with over 15,000 clients on student loan debt).

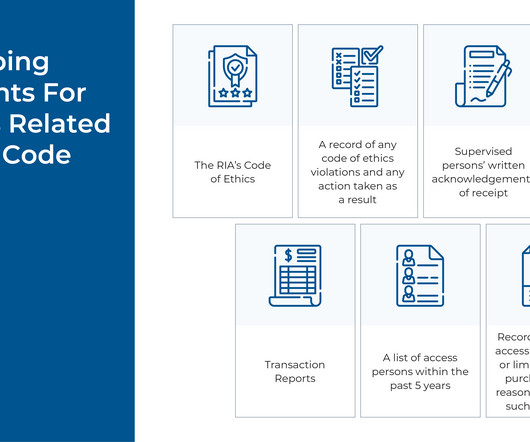

Maintaining adequate books and records is a cornerstone of compliance for all investment advisers. For financial planning services, a similar approach to documentation can be applied to support regulatory compliance from the start of client engagement through all the steps that follow.

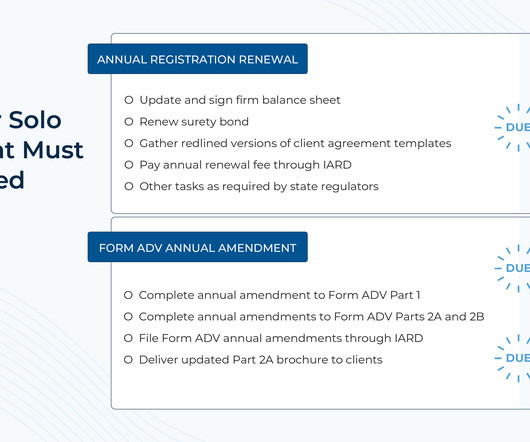

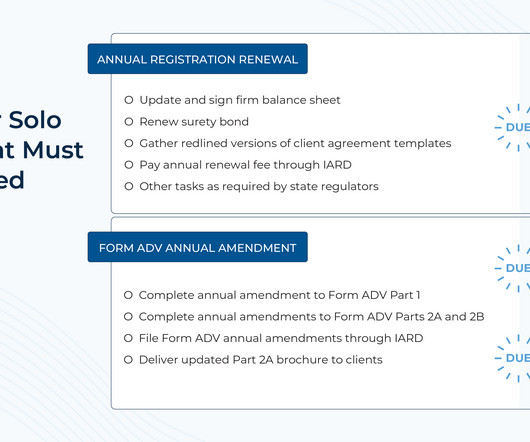

One of the most intimidating aspects of launching a solo advisory firm is the question of how to manage compliance. Creating a compliance calendar for a solo RIA can help to systematize and manage compliance tasks, requirements and deadlines.

One of the most intimidating aspects of launching a solo advisory firm is the question of how to manage compliance. The 1st category of tasks that advisory firms must handle involves renewing their registration with the applicable state(s) in which they do business each year, which typically involves submitting select documents (e.g.,

Fran is the CEO of Toler Financial Group, a DBA firm under the RIA Rossby Financial, in Silver Spring, Maryland, that oversees nearly $200 million in assets under management for 280 client households.

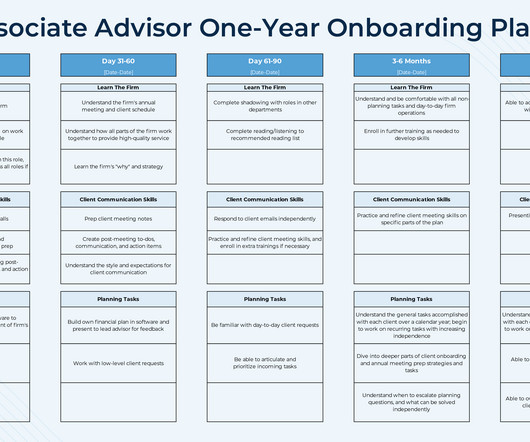

As their practices grow and they start to serve more clients, though, advicers invariably reach a point where they simply don't have the time to do everything on their own and need to decide whether to make their first hire (or not!). From there, the next decision will be whether the new hire should be an employee or independent contractor.

We have provided an onboarding plan template for advisors to download, which breaks up the skills list into two primary categories: 1) client communication skills (e.g., building an initial financial plan). meetings, email communication, and phone calls), and 2) technical skills (e.g.,

After advisors do all of the work of bringing on a new client (Marketing! Compliance!), This can result in fewer referrals and even the loss of the client, who might eventually opt to move their accounts to another (more appealing) advisory firm. Prospecting! Onboarding!

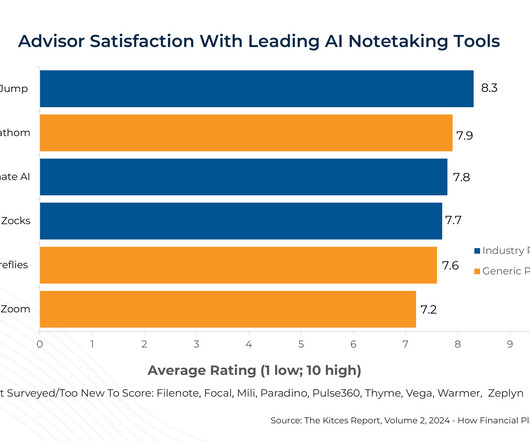

This is largely because, for financial advisors, it's not 'just' about capturing notes from the client meeting itself, but also about managing everything that follows: recording meeting notes in the CRM for compliance purposes, assigning post-meeting tasks to the team, and sending the client a post-meeting recap email.

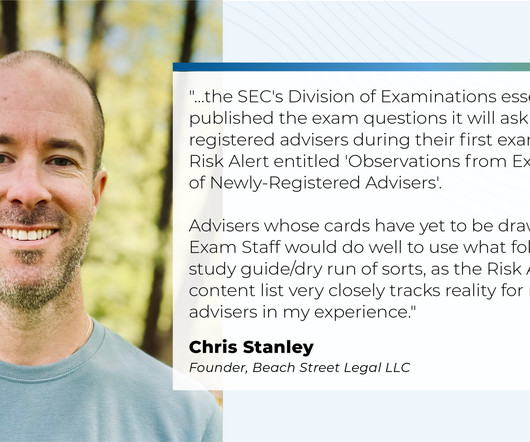

Even firms with robust compliance programs that do a good job following their required policies and procedures can struggle with examinations if they don't have the information that examiners will ask for readily available.

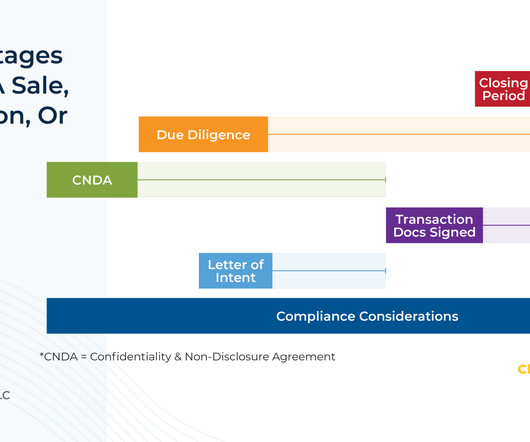

This moves the deal into the closing period, where the transaction can be publicly announced and any closing conditions must be met (such as obtaining consent from the seller’s clients to transition to the new owner). Only then can the new owner begin the work of integrating processes and systems and serving their new clients.

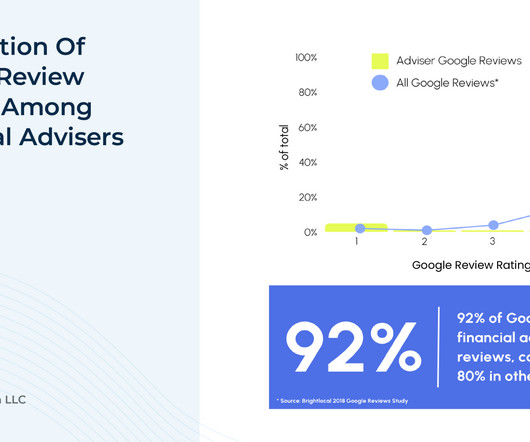

Nonetheless, fewer than 10% of SEC-registered investment advisers report using them, even though the SEC’s updated investment adviser marketing rule allows financial advisors to proactively encourage testimonials (from clients), use endorsements (from non-clients), and highlight their own ratings on various third-party review sites.

Financial advisors who pay third parties to solicit or refer prospective clients to generate new business have historically been subject to the SEC’s Cash Solicitation Rule. These requirements include ensuring that promoters are eligible to receive compensation for testimonials or endorsements (i.e.,

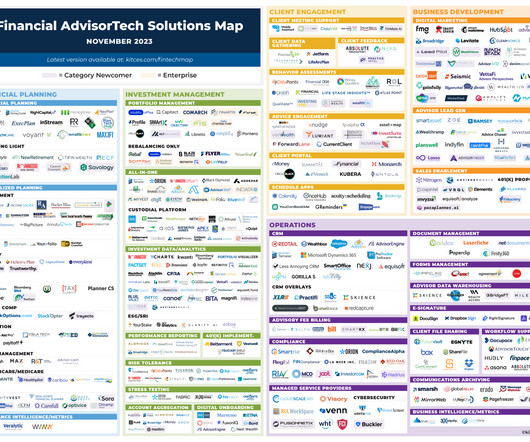

This month's edition kicks off with the news that Practice Intel has launched a new "growth platform" centered around quantifying the quality of an advisor's client relationships with an all-in "Relationship Quality Index" (RQI) – which while potentially valuable in helping advisors understand and improve their client experience (and subsequently (..)

Even firms with robust compliance programs that do a good job following their required policies and procedures can struggle with examinations if they don't have the information that examiners will ask for readily available.

A little over 20 years ago, when the Internet was still just a few years into gaining widespread use, the SEC understood its potential to transform how financial advisory firms conducted business with the ability to deliver advice digitally, lowering the barriers to serve clients across the country.

Notably, different affiliate platforms have different payout rates; those that pay out the most (and thus have the lowest fees) tend to cover relatively few functions such as compliance and technology, while those that pay out the least (and therefore have the highest fees) cover a significant amount of the advisor's overhead costs.

Which at best will still be a substantial uphill battle, given the hassle of switching from one financial planning platform to another (and the fact that most advisors are generally satisfied with their current financial planning software in the first place!).

While some are looking to gain a first-mover advantage by leveraging client testimonials and third-party endorsements (and adjusting their compliance programs before doing so), others are taking a wait-and-see approach. How a regular firm newsletter can keep clients engaged and improve retention.

All investment advisers are fiduciaries that owe a duty of care and loyalty to their clients, and, in an ideal world, advisory firms and their staff would abide by these requirements without the need for a prescriptive code of ethics. Read More.

Kamila is the CEO and Founder of Collective Wealth Partners, an independent RIA based in Atlanta, Georgia, that oversees nearly $25 million in assets under management for almost 175 client households.

Tim is the founder of Goodwin Investment Advisory, an RIA based in Woodstock, Georgia, that oversees $275M in assets under management for 370 client households. return in new onboarded client revenue for every $1 spent in marketing. return in new onboarded client revenue for every $1 spent in marketing.

This month's edition kicks off with the news that 'startup' custodian Altruist has completed a $169 million fundraising round as it continues to rebuild the RIA custodial tech stack layer-by-layer while positioning itself as the biggest RIA custodian built from scratch and solely for advisors – which, while making it the clear #3 custodian behind (..)

Which makes it all the more important for IARs to ensure Form U4 is up to date and that the way they are presenting themselves to current and potential clients in public – including content on their website, advertisements, and social media post – aligns with their (also publicly available) regulatory disclosures! Read More.

Adam is a principal with RubinGoldman and Associates, and the Founder and CEO of Asset-Map, a financial planning tool that helps financial advisors create a visual representation of their clients’ financial situation, reaching over 1.25 million users.

Jake is the Founder of Experience Your Wealth, an independent RIA based in Bristol, Rhode Island, that advises 78 client households with a 3-person team supporting more than $550,000 of ongoing revenue. Welcome back to the 331st episode of the Financial Advisor Success Podcast ! My guest on today's podcast is Jake Northrup.

This month's edition kicks off with the news that held-away asset management platform Pontera has raised $60 million in venture capital funding as advisors increasingly seek to directly manage clients' 401(k) and other outside assets – although an ongoing investigation by Washington state regulators over whether advisors' use of Pontera violates (..)

Bridget is the President of WealthChoice, a virtual independent RIA that oversees nearly $80 million in assets under management for 68 client families, and Co-Founder of Equita Financial Network, an advisor platform that helps advisors plug in and share resources. My guest on today's podcast is Bridget Venus Grimes.

Hearsay Systems rolls out a new small-to-mid-sized RIA platform for social media compliance and website design. Riskalyze signals an intent to rebrand itself away from ‘just’ risk tolerance assessments to a broader focus on helping advisors grow clients and assets.

This month's edition kicks off with the news that estate planning platform Wealth.com has launched Ester, an AI-driven 'legal assistant' that uses machine learning to help advisors quickly review and extract the key information from clients' estate planning documents, as it joins FP Alpha in the competition to become 'Holistiplan for estate planning (..)

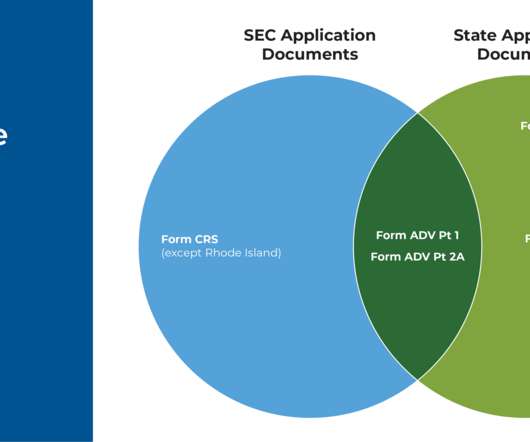

But by being aware of the varying requirements and filing documents in an accurate and timely manner, new firms can navigate their way through the registration process and (finally) begin offering planning services to clients! Notably, along with certain standardized forms (e.g., Read More.

This month's edition kicks off with the news that Riskalyze has completed its previously-announced rebranding, and will now be known as “Nitrogen”, a ”growth platform” for advisory firms – which represents less of a shift in the platform’s core function (given that Riskalyze’s risk tolerance tool was always (..)

Financial advisors, as professionals whose clients rely on their advice to make financial decisions, are legally and financially responsible for the advice that they give. Because ultimately, it's better to be surrounded by others who take care in advising their clients than to be the only one doing so! Read More.

But in the financial advisory business, firms are typically less concerned about employees taking intellectual property (e.g., financial planning processes and other 'trade secrets') with them to a competitor and are more concerned about clients (and the revenue they bring in) following their (departing) advisor to their new firm.

Mindy is the owner of Creative Money, an independent RIA based in Seattle, Washington, that offers a unique 12-month financial planning engagement – or as Mindy puts it on her homepage, “financial planning that doesn’t suck” – which has allowed her firm to work with nearly 400 client households just this year.

Firms seeking acquisitions may talk up their values prior to the sale, but the reality is that at a firm that is rapidly acquiring other businesses – particularly when funded by private equity ownership – the focus is often on the growth of assets and profitability, no matter what the core values are purported to be.

Registered Investment Advisers (RIAs) are generally required to enter into an advisory agreement with their clients prior to being hired for advisory services. million under the management of the adviser, or with a total net worth of at least $2.2 million under the management of the adviser, or with a total net worth of at least $2.2

Advisory agreements for Registered Investment Advisers (RIAs) contain many sections that are important both for the purposes of complying with SEC and state securities regulations, and for constituting a valid agreement between the RIA and the client. The agreement should also lay out some acknowledgments for the client to review.

Advisory agreements for Registered Investment Advisers (RIAs) contain many sections that are important both for the purposes of complying with SEC and state securities regulations, and for constituting a valid agreement between the RIA and the client. The agreement should also lay out some acknowledgments for the client to review.

Registered Investment Advisers (RIAs) are generally required to enter into an advisory agreement with their clients prior to being hired for advisory services. million under the management of the adviser, or with a total net worth of at least $2.2 million under the management of the adviser, or with a total net worth of at least $2.2

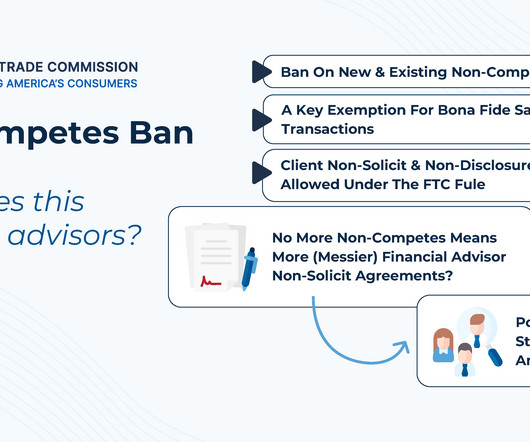

Which could make it more advantageous for firms and advisors alike to consider a more equitable, cooperative approach than strict on-competes or non-solicits to deciding which clients an advisor can solicit if they do eventually leave the firm.

Thus, Advice, Business, Compensation, and Securities (ABCS) are the key elements in this definition. But once a financial coach addresses specific questions from clients around actual securities (e.g., Read More.

billion in assets under management for approximately 4,700 client households. Jenny is a Principal and Wealth Manager at Modera Wealth Management, an RIA based in Westwood, New Jersey, that oversees $12.5

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content