This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

These services may range from 'standard' offerings like retirementplanning to less traditional areas like credit card consulting. In a firm's early years, there tends to be more room for experimentation, with advisors adding new services to provide value and attract clients.

It's natural for advisors to begin discovery meetings by asking questions about a client's current financial situation – understanding cash flow, debt, investments, risk tolerance, or even the burning tax concern that brought them to the advisor's door in the first place is crucial for financial planning.

Travis is the founder of Student Loan Planner, an RIA and student loan consulting company based in Chapel Hill, North Carolina that serves nearly 1,400 households with ongoing financial planning (as well as consulting with over 15,000 clients on student loan debt).

Over the past decade, a growing number of advisors have expanded into offering comprehensive financial planning services, reflecting a shift that not only helps them stand out from (increasingly commoditized) portfolio management offerings but also supports clients' broader financial goals.

Some prospects approach an advisor with an immediate 'problem to be solved', such as a fast-approaching retirement date. I help clients in retirement by doing X, Y, and Z."). These situations often narrow the focus of the prospecting conversation, giving the advisor a clear opportunity to affirm their value (e.g., "I

Seth is the founder of Heartwood Financial Planning, an advisory firm affiliated with PlanMember Securities Corporation that is based in Fresno, California, and oversees approximately $100 million in assets under management for 850 client households.

Jennifer is the CEO of The Mather Group, an RIA based in Chicago, Illinois, that oversees $15 billion in combined assets under management and advisement for approximately 4,400 client households. Read More.

In the early days of financial planning, serving clients often meant developing transactional relationships focused on facilitating trades and selling insurance. Over time, advisors shifted toward more analytical approaches, such as investment management and retirementplanning.

Daniel is the CEO of WMGNA, a hybrid advisory firm based in Farmington, Connecticut, that oversees approximately $270 million in assets under management for 200 client households.

Financial advisors have a wide range of strategies at their disposal to create financial plans for their clients. This strategy is valuable because it generally allows for higher initial withdrawal rates than more static approaches that don’t accommodate clients willing to adjust their spending in retirement.

However, when these aspirations are delayed or blocked by senior advisory firm partners who choose to delay their retirementplans, it can leave younger advisors frustrated and in a place of uncertainty about their futures with their firm.

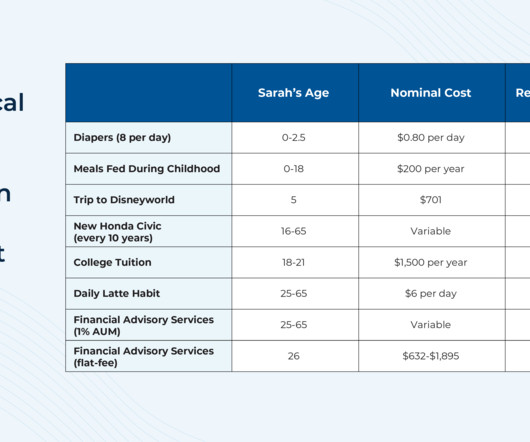

Though in practice, while a 1% AUM fee is a common 'starting point' in the industry, the actual fee structure can vary based on the firm's approach; for example, some firms may reduce the fee for high-net-worth clients, or charge an additional fee for separate and additional services (from deeper financial planning to add-ons like tax preparation).

On April 25, 2024, the Department of Labor (DoL) issued the final version of its Retirement Security Rule (the "Final Rule"), which imposes an ERISA fiduciary standard "that applies uniformly to all investments that retirement investors may make with respect to their retirement accounts ".

However, because many next-generation clients such as those who are Millennials and Gen Zers are still building their assets up, paying $10,000 or more in advisory fees each year may not be feasible for them… at least not yet. robo-managed portfolios) at a lower fee.

This month's edition kicks off with the news that digital estate planning platform Wealth.com has raised a whopping $30 million in Series A funding, following on the heels of Vanilla's follow-on $20M capital round just a few months ago – which on the one hand reflects the anticipated enthusiasm for solutions that can help advisors efficiently (..)

Chris is the founder of Sparrow Wealth Management, an RIA based in Orlando, Florida, that oversees approximately $110 million in assets under management for 68 client households.

Matthew is the Founder and CIO of Lansing Street Advisors, an independent RIA based in Ambler, Pennsylvania that oversees $160 million in assets under management for 60 client households.

Suzanne is a Senior Financial Advisor at Meridian Wealth Management, an RIA based in Lexington, Kentucky, where she oversees approximately $110 million in assets under management for nearly 150 client households.

What's unique about Ramit, though, is how he literally wrote the book (and subsequently launched an online educational platform and brand) on how consumers can not just learn more about their finances but change their financial behaviors, without focusing on a budget or setting retirement savings goals, and instead helping them focus their money more (..)

As owners of financial planning firms approach retirement, some may decide to sell to an external buyer, while others may plan for an internal succession. Sometimes, this succession plan can include the owner's child, providing an opportunity to keep the business in the family. Read More.

In this episode, we talk in-depth about the best practices David recommends to firms to start preparing in advance for an internal succession (including creating defined career tracks and compensation structures as well as getting the firm’s business metrics in order and receiving a third-party valuation), how David advocates for breaking up (..)

From there, we have several articles on practice management: Why it is important for advisors charging on a fee-for-service basis to regularly reassess their pricing, and best practices for letting current clients know about a fee increase. How firms can best leverage their internal data to improve the number of client referrals they receive.

Why private placement life insurance policies could become an increasingly popular option for ultra-high-net-worth clients. The upcoming debut of a new tontine product could add another option for advisors looking to mitigate their clients’ longevity risk.

While some are looking to gain a first-mover advantage by leveraging client testimonials and third-party endorsements (and adjusting their compliance programs before doing so), others are taking a wait-and-see approach. How a regular firm newsletter can keep clients engaged and improve retention.

Troy is the Founder and CEO of Oak Harvest Financial Group, an RIA based in Houston, Texas, that oversees approximately $750 million in assets under management for about 1,000 client households.

Hans is the founder of Intelligent Investing, an RIA based in Greenville, South Carolina, that oversees $50M in assets under management for 40 client households.

Mark is the Chief Investment Officer of Noble Wealth Management, an RIA based in Greenwood Village, Colorado, that oversees $320 million in assets under management for 160 client households.

Liz is the co-owner of Pleasant Wealth, a hybrid advisory firm based in Canton, Ohio that oversees $146 million in assets under management for 522 client households.

This month's edition kicks off with the news that held-away asset management platform Pontera has raised $60 million in venture capital funding as advisors increasingly seek to directly manage clients' 401(k) and other outside assets – although an ongoing investigation by Washington state regulators over whether advisors' use of Pontera violates (..)

” has brought a wide range of changes to the world of retirementplanning. Also in industry news this week: Why many clients of robo-advisors are seeking out human advisors in the current market climate. How advisors are increasingly purchasing individual bonds rather than bond funds in client accounts.

This month's edition kicks off with the news that robo-advisor Betterment entered into a $9M settlement with the SEC for misrepresenting its tax-loss harvesting practices in its client agreements and marketing materials compared with its actual practices (e.g.,

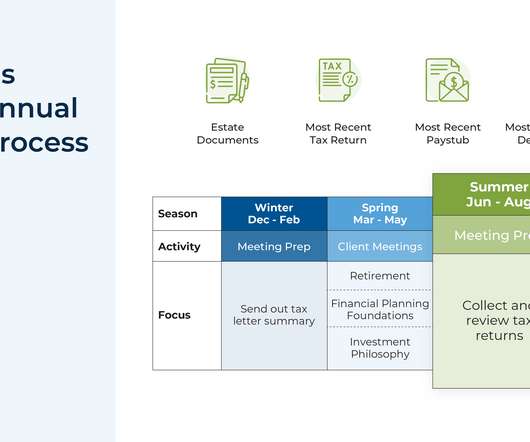

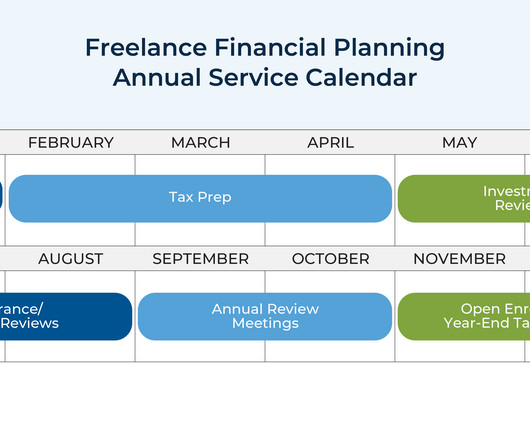

A common service model for many financial advisory firms is to schedule annual client meetings throughout the year where the advisor meets with each client in the month they started working with the firm, and conducts a comprehensive review of all planning topics for the client.

It goes by many different names: semi-retirement, partial or phased retirement, second career, and so on. But typically, it means the same thing: working in some capacity after retiring early. As more workers consider the growing appeal of semi-retirement, some ask — is working part-time in retirement a good idea?

Also in industry news this week: A recent survey indicates that retirementplan sponsors currently using financial advisors to support their plan are overwhelmingly satisfied with the service they receive, which also leads to improved retirement savings for their employees.

This month's edition kicks off with the news that Riskalyze has completed its previously-announced rebranding, and will now be known as “Nitrogen”, a ”growth platform” for advisory firms – which represents less of a shift in the platform’s core function (given that Riskalyze’s risk tolerance tool was always (..)

From there, we have several articles on tax planning: How advisors can add value for their clients by managing their exposure to mutual fund capital gains distributions. How advisors can help their clients turn their HSAs into wealth-building machines.

Gaetano is a partner and senior financial advisor at Fountainhead Advisors, an RIA based in Warren, New Jersey, that oversees approximately $900 million in assets under management for 1,000 client households.

”, a series of measures that will have significant impacts on the world of retirementplanning. A review of financial planning actions, from tax-loss harvesting to charitable giving, that have a December 31 deadline.

CPA, EA, or JD) to prepare tax returns and represent clients before the IRS, there has also been the impression that there is simply not enough time for one person to do both. Furthermore, similarly structuring the client service calendar for the remainder of the year to focus on specific topics at set times (e.g., Read More.

Advisory agreements for Registered Investment Advisers (RIAs) contain many sections that are important both for the purposes of complying with SEC and state securities regulations, and for constituting a valid agreement between the RIA and the client. The agreement should also lay out some acknowledgments for the client to review.

Stacey is the President of Envision Financial Planning, an independent RIA based in Memphis, Tennessee, that oversees nearly $200 million in assets under management for 206 client households.

Advisory agreements for Registered Investment Advisers (RIAs) contain many sections that are important both for the purposes of complying with SEC and state securities regulations, and for constituting a valid agreement between the RIA and the client. The agreement should also lay out some acknowledgments for the client to review.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content