This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Over the past decade, a growing number of advisors have expanded into offering comprehensive financialplanning services, reflecting a shift that not only helps them stand out from (increasingly commoditized) portfolio management offerings but also supports clients' broader financial goals.

It's natural for advisors to begin discovery meetings by asking questions about a client's current financial situation – understanding cash flow, debt, investments, risk tolerance, or even the burning tax concern that brought them to the advisor's door in the first place is crucial for financialplanning. Read More.

Some prospects approach an advisor with an immediate 'problem to be solved', such as a fast-approaching retirement date. I help clients in retirement by doing X, Y, and Z."). However, not all prospects have immediate financial concerns. One effective way to facilitate this self-discovery is through self-persuasion questions.

Welcome to the 432nd episode of the Financial Advisor Success Podcast! Seth is the founder of Heartwood FinancialPlanning, an advisory firm affiliated with PlanMember Securities Corporation that is based in Fresno, California, and oversees approximately $100 million in assets under management for 850 client households.

Travis is the founder of Student Loan Planner, an RIA and student loan consulting company based in Chapel Hill, North Carolina that serves nearly 1,400 households with ongoing financialplanning (as well as consulting with over 15,000 clients on student loan debt).

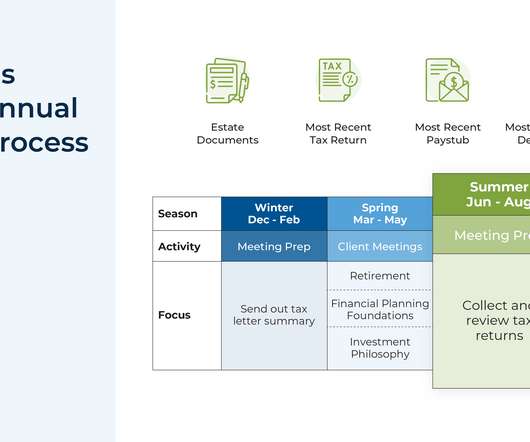

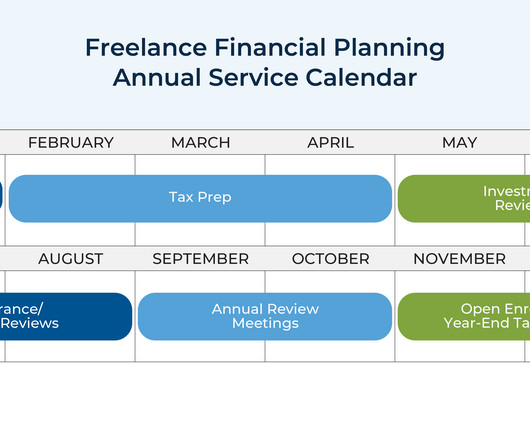

However, by creating a systematic annual process to monitor and update client plans based on seasons, not only can advisors save time and work more efficiently, but they can also communicate the value of ongoing financialplanning services to prospects and clients more effectively.

Financial advisors have a wide range of strategies at their disposal to create financialplans for their clients. This strategy is valuable because it generally allows for higher initial withdrawal rates than more static approaches that don’t accommodate clients willing to adjust their spending in retirement.

In this episode, we talk in-depth about why Daniel decided to outsource tax return preparation (rather than hire someone to do it in-house) to be able to access the expertise of the CPAs his firm uses (particularly for clients with complicated equity compensation plans), how Daniel views these CPA relationships as mutually beneficial from a financial (..)

In the early days of financialplanning, serving clients often meant developing transactional relationships focused on facilitating trades and selling insurance. Over time, advisors shifted toward more analytical approaches, such as investment management and retirementplanning.

Though in practice, while a 1% AUM fee is a common 'starting point' in the industry, the actual fee structure can vary based on the firm's approach; for example, some firms may reduce the fee for high-net-worth clients, or charge an additional fee for separate and additional services (from deeper financialplanning to add-ons like tax preparation).

As owners of financialplanning firms approach retirement, some may decide to sell to an external buyer, while others may plan for an internal succession. Sometimes, this succession plan can include the owner's child, providing an opportunity to keep the business in the family.

What's unique about Brad, though, is how he built a multi-billion-dollar advisory firm not by moving 'upmarket' to gather multi-millionaire clients, but instead leveraged his 401(k) retirementplan advisory firm to begin offering comprehensive financialplanning to the employees of large companies as an added employee benefit, and in the process scaled (..)

Zack is the Director of FinancialPlanning and Participant Engagement of Greenspring Advisors, an RIA based in Towson, Maryland, that manages $2 billion of private wealth assets under management for 1,300 client households and advises on an additional $5 billion in retirementplan assets.

Welcome to the 356th episode of the Financial Advisor Success Podcast ! Sarah-Catherine is the founder of Aptus Financial, a fee-only financialplanning firm based in Little Rock, Arkansas, that is approaching $2M in revenue and works with over 480 client households.

What's unique about Liz, though, is how she and her brother have taken ownership of what was originally their father’s broad commission-based practice with more than 1,500 clients, and have managed the balance of transitioning the business into a fee-based financialplanning practice while still doing right by the smaller or more transactional (..)

Welcome back to the 297th episode of the Financial Advisor Success Podcast ! Andy is the owner of Tenon Financial, a virtual independent RIA that oversees $70 million in assets under management for 43 retired client households. My guest on today's podcast is Andy Panko.

Also in industry news this week: While the FPA is going full steam ahead on its federal and state lobbying efforts to regulate the title “financial planner”, CFP Board is more focused on increasing recognition of the CFP marks. How firms can best leverage their internal data to improve the number of client referrals they receive.

Enjoy the current installment of “Weekend Reading For Financial Planners” - this week’s edition kicks off with the news that Congress appears poised to pass “SECURE Act 2.0”, ”, a series of measures that will have significant impacts on the world of retirementplanning.

What's unique about Chris, though, is how he has built a highly efficient solo practice that allows him to work fewer than 25 hours/ week to have more time for his family and managed to cut his hours down by relentlessly focusing on only the financialplanning tasks that really truly matter most to his clients… and either outsourcing, or just (..)

In this post, Kitces.com Senior FinancialPlanning Nerd Ben Henry-Moreland writes about how he went from being hesitant to offer tax preparation at his solo RIA (given how common it is for tax preparers to work long hours throughout tax season) to embracing it as a core part of the business’ service offering.

What’s unique about Matthew, though, is how he differentiates his firm by offering his high-net-worth clients opportunities to diversify their investment portfolios by syndicating private real estate partnerships that directly purchase individual multi-unit rental properties.

It goes by many different names: semi-retirement, partial or phased retirement, second career, and so on. But typically, it means the same thing: working in some capacity after retiring early. As more workers consider the growing appeal of semi-retirement, some ask — is working part-time in retirement a good idea?

What's unique about Bridget, though, is how, as a solo advisor, she found herself overwhelmed with the pressures of having to manage different aspects of her business while also providing great service to her clients as she quickly grew to $77M of AUM in 7 years, and has decided to not to "scale" her firm by hiring more advisors but instead leverage (..)

We also discuss why Jake and his team not only create long-term financialplans for their clients, but also focus on a 10-year vision to help his younger, travel-loving clientele start achieving more of their immediate goals so they're more likely to retain as clients by feeling like they're making near-term financialplanning progress.

Welcome back to the 317th episode of the Financial Advisor Success Podcast ! Jennifer is the CEO and a Senior Advisor for Milestone FinancialPlanning, an independent RIA based in Bedford, New Hampshire, that oversees $360 million in assets under management for 225 client households.

and why Suzanne has taken an approach of not trying to work and save for retirement as a time to enjoy when she gets there, but instead has structured her busy-season-light-season approach to client meetings to allow for more space to enjoy trips and time with her family now, instead.

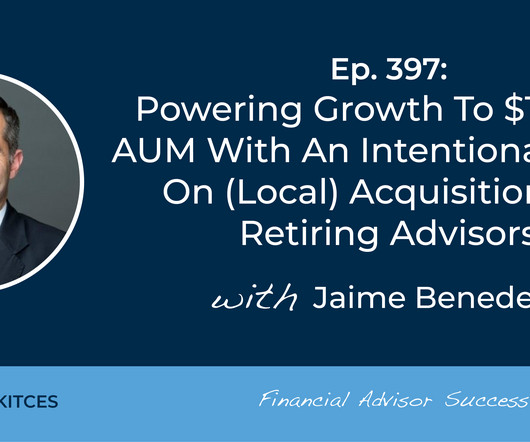

What's unique about Jaime, though, is how his firm has grown to more than $1 billion in AUM over the past 20 years in part by making a series of 6 acquisitions, typically buying mixed fee-and-commission practices from retiring advisors in his local area and converting them into ongoing recurring revenue financialplanning clientele.

a single person, a couple, a business, or a retirementplan) and the date on which the agreement will become effective. To start, the agreement should contain basic information about the adviser-client relationship, including who the client is (e.g.,

a single person, a couple, a business, or a retirementplan) and the date on which the agreement will become effective. To start, the agreement should contain basic information about the adviser-client relationship, including who the client is (e.g.,

What's unique about Gaetano, though, is how after breaking away from an insurance broker-dealer with barely $5M in assets under management, he has been able to quickly build his practice to $75 million in AUM in just 5 years in part by turning what was originally a liability for him in his 20s – being a 'young' advisor who prospective clients (..)

Welcome back to the 307th episode of the Financial Advisor Success Podcast ! Stacey is the President of Envision FinancialPlanning, an independent RIA based in Memphis, Tennessee, that oversees nearly $200 million in assets under management for 206 client households. My guest on today's podcast is Stacey Hyde.

We also talk about how, while she was still working for a broker-dealer, Libby learned to differentiate herself not by learning to better sell her firm’s products but instead by diving deep into contract language of her clients’ insurance and annuity policies to find the gaps where those products didn’t really fit their financial (..)

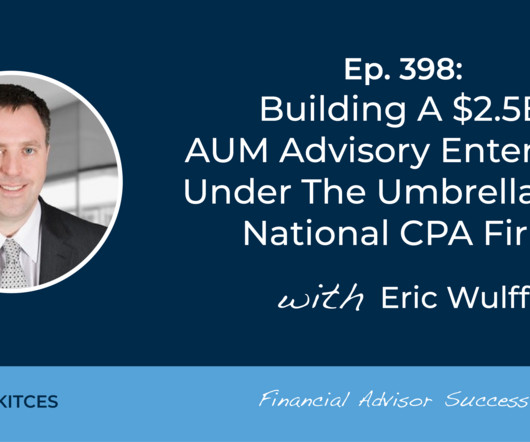

What's unique about Eric, though, is how he has built Marcum Wealth into a multi-billion-dollar firm under the umbrella of a national accounting firm, in large part by cultivating mutually beneficial relationships with the firm's internal CPAs to get them comfortable providing referrals of their accounting clients to his financialplanningbusiness.

Plan for Current Business Needs. First, let’s talk about the importance of a businessplan. How does an idea develop into a fully functioning business? It takes vision, work, and a good plan. For entrepreneurs, we call this map a businessplan. Creating a marketing plan.

In this episode, we talk in-depth about how John and his entire firm serves the Federal employee niche, with a particular focus on the areas that make their clients' situations different from others, such as the Federal government's unique retirement system that includes both defined-benefit pension and defined-contribution plans, how John finds that (..)

It goes by many different names: semi-retirement, partial or phased retirement, second career, and so on. But typically, it means the same thing: working in some capacity after retiring early. As more workers consider the growing appeal of semi-retirement, some ask — is working part-time in retirement a good idea?

So whether you need to pay off debt , build an emergency fund , save for your kids’ college education , or invest for retirement , here are some ways you can make it hap’n, cap’n. Why Long-Term Financial Goals Are Important Long-term financial goals provide direction and motivation for your financial decisions.

Delvin Joyce is a Certified Financial Planner specializing in providing comprehensive financialplanning services. He collaborates with clients and their advisors to create a detailed and robust financialplan tailored to their unique needs and goals.

Founding owners of financial advisory firms often spend much of their time focusing on the short-term aspects of running their business, from providing high-quality client service to pursuing client growth.

In this episode, we talk in-depth about how Lisa realized that by visiting Coca-Cola’s headquarters consistently and engaging employees in-person about their financial issues, she could become known as a familiar and trusted financial expert in the Coca-Cola community, how Lisa leveraged writing white papers about preparing for retirement and (..)

We also talk about Rob's journey from getting an undergrad in Kinesiology and starting med school to moving into accounting and then ultimately becoming a financial planner through the program at UCLA (because financialplanning was the perfect blend of helping people the way he wanted to in medicine, and working with numbers the way he did in accounting), (..)

How to Choose the Right Wealth Management Firm in Kansas City Managing your wealth is a crucial aspect of financial success and security. Long-Term vs. Intermediate and Short-Term Goals Begin by distinguishing between your long-term, intermediate-term and short-term financial goals.

In this episode, we talk in-depth about how Joe has witnessed firsthand as an advisory firm owner, and now a partner at a leading global investment management firm, how the financial services industry is evolving in real time as more banks and brokerage firms are truly adopting financialplanning and implementing advisory services at national scale (..)

How to Choose the Right Wealth Management Firm in Kansas City Managing your wealth is a crucial aspect of financial success and security. Long-Term vs. Intermediate and Short-Term Goals Begin by distinguishing between your long-term, intermediate-term and short-term financial goals.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content